US dollar stable as US-Iran stalemate continues ahead of key data

USD: No deal reached ahead of busy month of central bank meetings

The US dollar is broadly stable as we start a new month with no sign of the key breakthrough needed in order to have a formal ceasefire extension agreement reached. Nothing much has been said on the US side over the weekend apart from a few Truth Social posts by President Trump stating the focus of any deal would be not allowing Iran to have a nuclear weapon and that everything “would work out well in the end”. The semi-official Tasnim news agency in Iran quoted officials stating that exchanges are ongoing so that will be good enough for now for the financial markets to remain stable. Brent crude oil is over 2% higher today on the fact that a deal has not been reached given the 18% drop that took place over the previous two weeks on the building optimism that a deal could be done.

This month will be a busy month for central bank meetings and whether these meetings take place against a backdrop of the reopening of the Strait of Hormuz or not will be important for the tone and communication at these meetings. Nine G10 central banks will meet this month with only the RBNZ not meeting and we will likely see some of those central banks act despite the ongoing uncertainty related to the conflict in the Middle East. The OIS market indicates that there are two central banks that are most likely to act – the ECB and the BoJ. Executive Board member at the ECB, Isabel Schnabel, stated in South Korea today that the ECB can “no longer look through this shock” and that the “risk of de-anchoring inflation expectations is rising”. Her comments echoed comments from President Lagarde last week, also in Asia, who spoke of the importance of “credibility” and that credibility is “earned through action”. There is very little doubt now that the ECB will act at the meeting on 11th June. The inflation data last week points to a pick-up in the euro-zone annual CPI data to be released tomorrow, from 3.0% to 3.2% - also the MUFG estimate (here). The decision is close to priced so the key for the euro will be forward guidance on the potential for a further hike.

The BoJ pricing for its meeting on 16th June is a little less than for the ECB – the implied probability is around 80% for a 25bp hike. But action remains likely, and even though inflation has eased, the risk of being behind the curve is rising. Weaker inflation in Tokyo in part reflected government measures while the continued weakness of the yen is telling after the MoF confirmed a record one-month JPY 11.7trn worth of yen buying between 28th April and 27th May. Action would help to curtail yen selling although developments in the Middle East, crude oil prices and global yields will be key as well.

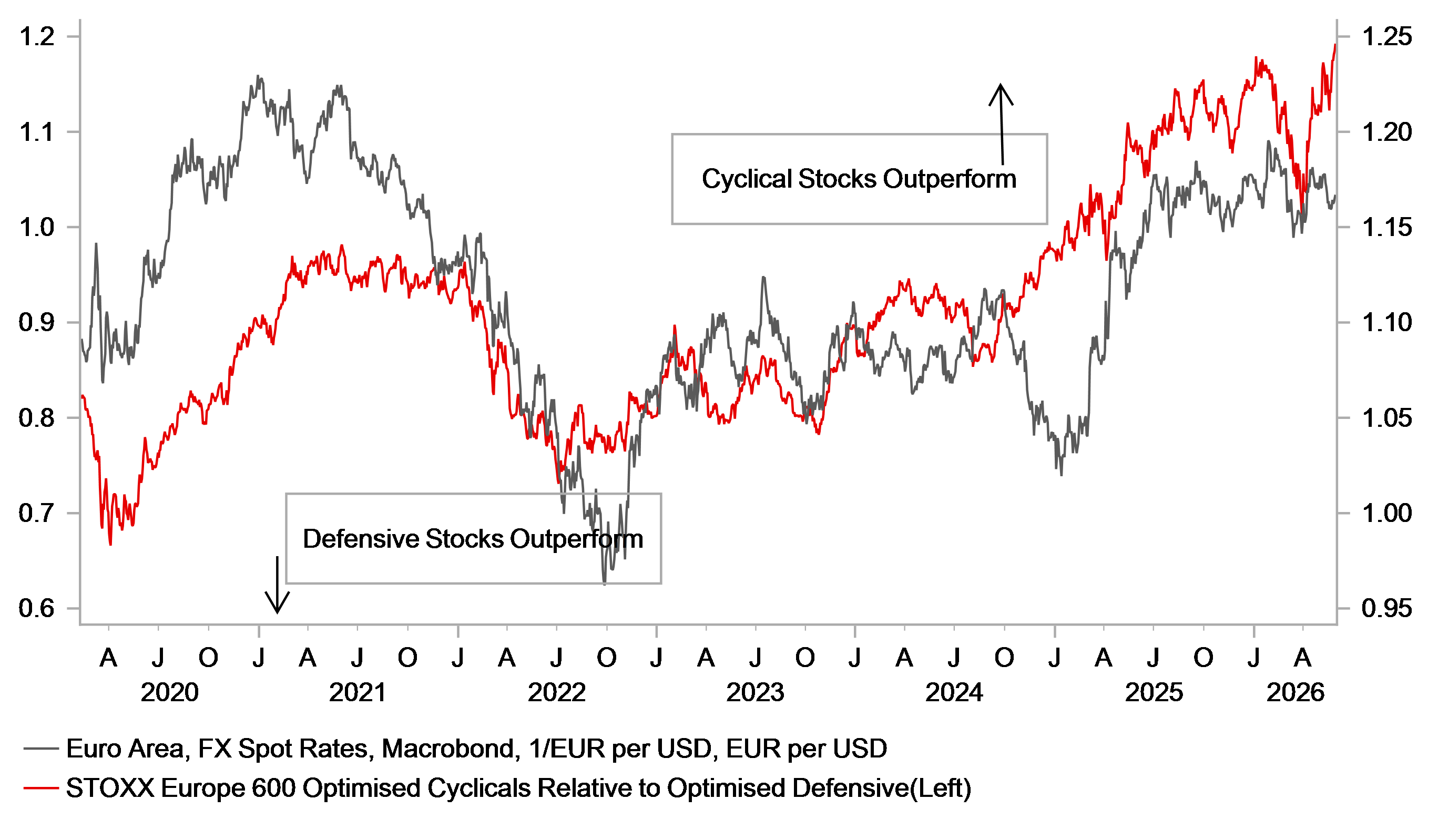

EURO CYCLICAL STOCK OUTPERFORMANCE HELPS SUPPORT EUR

Source: Bloomberg, Macrobond & MUFG Research

USD: Data heavy week to provide colour on inflation risks

The 2-year yield in the US jumped by 13bps in May and that reflected less confidence amongst investors over the “looking through the energy shock” view that had been the consensus view that had seen yields lag moves in Europe. The rise in the 2-year yield in the US was in contrast to moves in May in Europe. The 2-year yield in Germany fell 11bps in May and in the UK the drop was even larger, 24bps. The UK move was mainly driven by the weak jobs and CPI prints and the more balanced communications on policy guidance, certainly compared to the ECB’s more direct approach signalling a rate hike in June.

But as usual, the start of a new month brings with it a lot of the key economic data prints in the US. If a deal is announced and confirmed by President Trump there may well be a greater willingness amongst Fed officials to look through the energy price shock. Still, the extent in which the crude oil price declines further will be important as will the data. The worse the inflation data, the more difficult to look through it. The ISM manufacturing and services reports will be released this week along with the JOLTS report and the ADP employment report and followed by the NFP report on Friday.

The consensus is for another reasonable NFP print with the consensus for a gain of 85k after a gain of 115k in April. The unemployment rate is expected to remain at 4.3% with YoY average hourly earnings growth slowing to 3.4%. That would lift the 3mth average run rate from 48k to 128k. The 6mth average run is perhaps the more reflective of the underlying run rate and that would increase from 55k to 62k. The 12mth average run rate would increase from 21k to 27k. Whatever way you look at it there are signs of a gradual improvement in the pace of payrolls growth that if confirmed in the data this week would certainly suggest continued caution over pushing for renewed rate cuts any time soon. The unemployment rate will also paint a similar picture measured by relative change over the last twelve months – the consensus unemployment rate for May is 4.3%, which would mean an unchanged level from 12mths ago. Over the previous 12mth period the unemployment rate increased 0.4ppt to 4.3%.

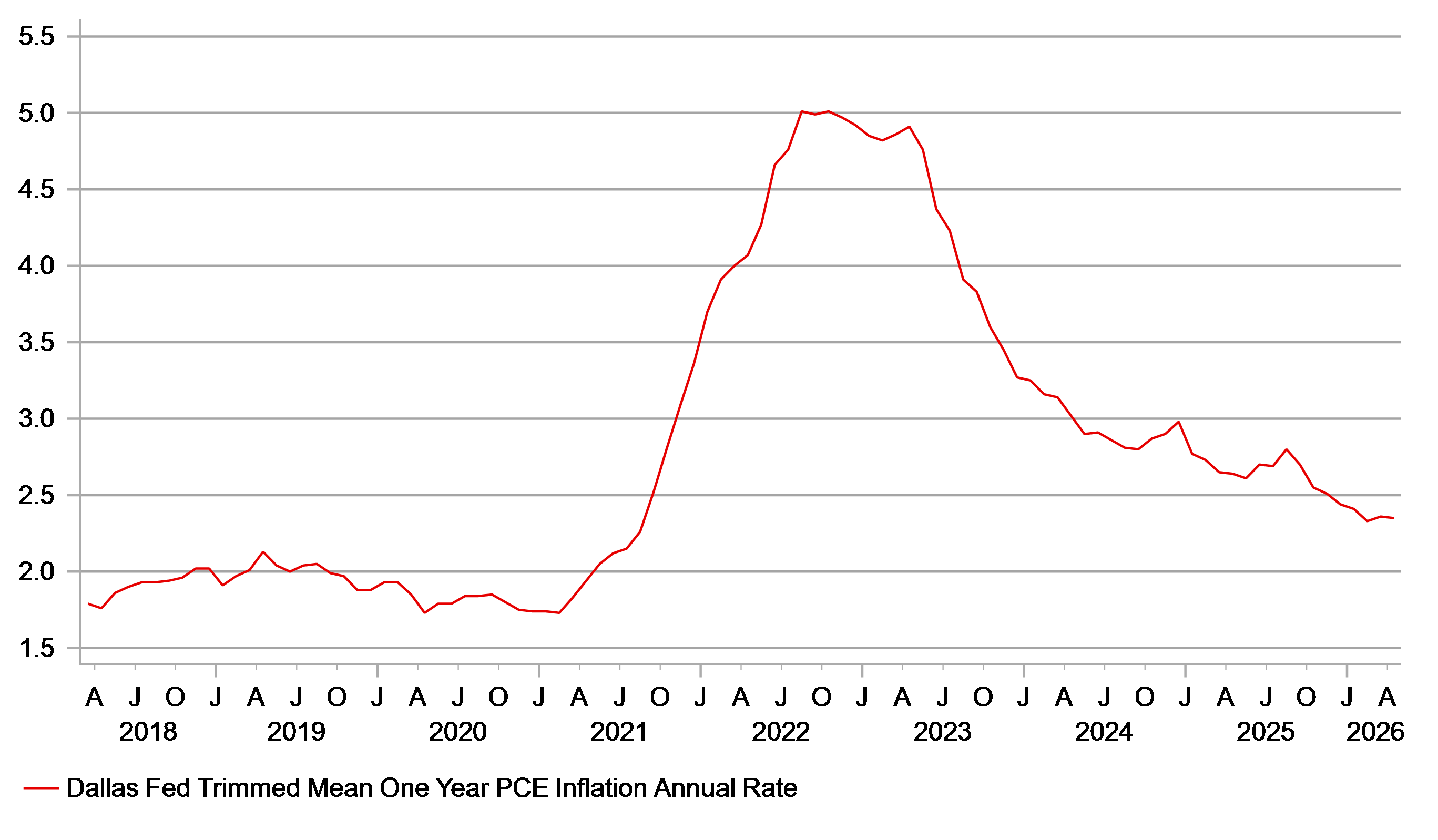

The conclusion to a consensus NFP print on Friday would be that monetary policy is in the right place and wouldn’t argue for a change either way. We still have to remember though that we are entering a new Federal Reserve period under new leadership, and we could well have a Chair who pushes a dovish interpretation. The PCE data last week showed the headline rate rising from 3.5% to 3.8% and the core from 3.2% to 3.3%. But Fed Chair Warsh in his nomination hearing cited trimmed mean measures as a good gauge of underlying inflation. The Dallas trimmed mean YoY rate was stable at 2.3% for the third consecutive month. Good ammunition for Fed Chair Warsh if he wants to push a dovish message and counter the hawkish arguments within the FOMC. We await Warsh’s first communications, but he could well push for greater focus on underlying inflation that would help keep rates in check and weaken the dollar.

WARSH HAS CITED TRIMMED MEAN AS A FAVOURED MEASURE OF UNDERLYING INFLATION – THIS DALLAS MEASURE REMAINS STABLE

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

CH | 08:30 | procure.ch PMI | (May) | 54.0 | 54.5 | !! |

FR | 08:50 | French Manufacturing PMI | (May) | 48.9 | 52.8 | !! |

DE | 08:55 | German Manufacturing PMI | (May) | 49.9 | 51.4 | !! |

EU | 09:00 | Manufacturing PMI | (May) | 51.4 | 52.2 | !!! |

EU | 09:00 | M3 Money Supply (YoY) | (Apr) | 3.3% | 3.2% | ! |

EU | 09:00 | Loans to Non Financial Corporations | (Apr) | 3.1% | 3.2% | ! |

EU | 09:00 | Private Sector Loans (YoY) | - | 3.0% | 3.0% | ! |

UK | 09:30 | Manufacturing PMI | (May) | 53.7 | 53.7 | !!! |

EU | 10:00 | Unemployment Rate | (Apr) | 6.2% | 6.2% | !! |

US | 13:30 | Fed Waller Speaks | - | - | - | !! |

CA | 14:30 | Manufacturing PMI | (May) | - | 53.3 | ! |

US | 14:45 | Manufacturing PMI | (May) | 55.3 | 54.5 | !!! |

US | 15:00 | ISM Manufacturing PMI | (May) | 53.3 | 52.7 | !!!! |

US | 15:00 | Construction Spending (MoM) | (Apr) | 0.3% | 0.6% | !! |

US | 15:00 | ISM Manufacturing Prices | (May) | 85.3 | 84.6 | !!! |

Source: Bloomberg & Investing.com