Ahead Today

G3: US initial jobless claims, regional Fed activity indices, PMI data; eurozone PMI

Asia: BSP policy rate decision, Singapore CPI, Taiwan industrial production, India PMI

Market Highlights

US equities have continued to gain, led by tech companies. US 10-year yield holds at 4.3%, but the 2-year yield shows a renewed pickup to an elevated 3.8%. The dollar strengthened slightly to 98.6, on the back of higher carry. Meanwhile, Brent prices closed above $100/bbl for the first time in the past 7 trading days, following a geopolitical standoff between US-Iran in the Middle East. While President Trump has unilaterally extended the ceasefire indefinitely, the continued blockade of Iranian ports and Iran’s rejection of peace talks point to a prolonged disruption to energy flows through the Strait of Hormuz. With no quick resolution in sight, risks of more persistent, oil‑driven inflation have risen. That said, the ceasefire extension suggests limited appetite for further escalation for now, offering some marginal support to broader risk sentiment. Against this backdrop, markets have maintained their net long positioning on the dollar, while the yen could face further weakness in the near term as the energy shock persists and markets push back expectations of BOJ rate hike to June at the earliest. That said, deeper yen depreciation may increasingly run up against BOJ intervention risks, particularly as yen weakness would exacerbate oil‑driven inflation pass‑through.

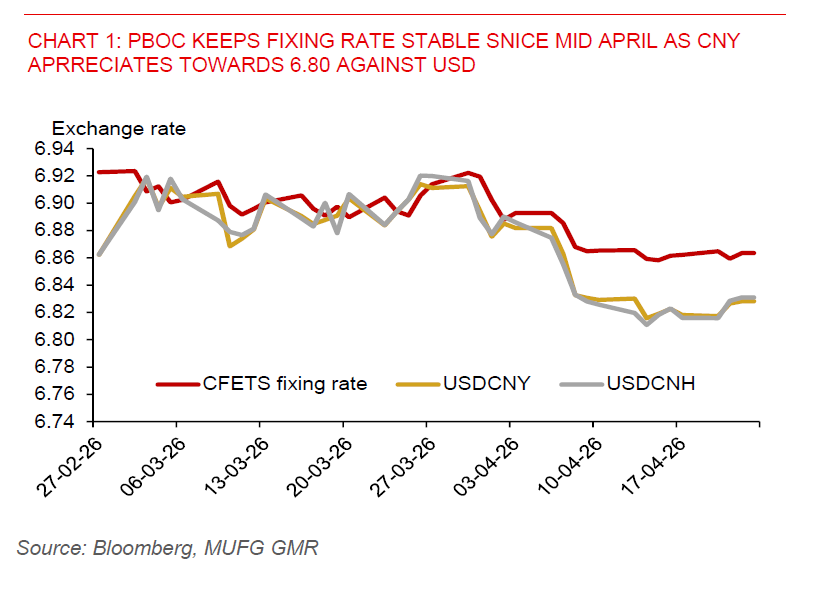

In Asia, CNY stayed resilient against the US dollar, while other regional currencies traded modestly weaker. The PBOC has injected more cash into the banking system, keeping funding costs low and policy accommodative, likely underpinning further yield declines and slowing the pace of CNY appreciation. The PBOC has kept its daily USDCNY fixing broadly stable since mid-April, with CNY appreciating close to the 6.8000 level against the US dollar.

Bank Indonesia held rates unchanged at 4.75%, as widely expected and in line with our outlook. Rupiah stability remains a key priority. BI Governor has pledged to do more to stabilize the rupiah and keep inflation within target range. As part of its FX measures, BI will allow some eligible primary dealers to sell FX against the rupiah in offshore NDF markets, while expanding its FX monetary operations in CNH and local currency transactions. BI also reiterated that the rupiah is undervalued relative to the country’s macro fundamentals – a view that we share (see IndonesiaPulse: The case for rupiah stability as valuations turn supportive). BI left its GDP growth outlook for this year unchanged at 4.9-5.7%, but forecast a larger current account deficit.

A key regional highlight today is the BSP policy rate decision, where we expect a rate hike to guard against broadening inflation risks. Even so, this may not be enough to stem peso weakness in our view, given the Philippines’ huge reliance on Middle Eastern oil and potential negative impact of the Iran conflict on remittances coming from the Middle East. Indeed, PHP has been the worst performing Asian currency since the onset of US-Iran war.

In Singapore, March CPI data will be closely watched. With Brent prices already sharply higher, imported inflation pressures are likely to build. Expectations of further MAS tightening in July should therefore keep the bias skewed toward a lower USDSGD.