Key Points

-

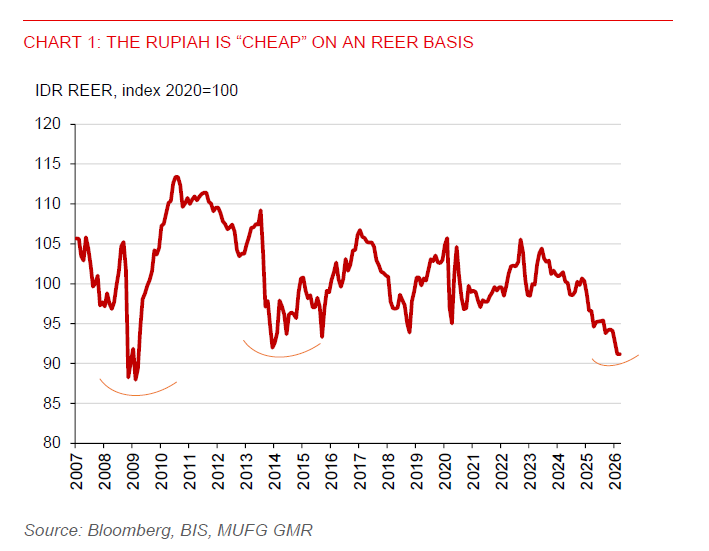

Geopolitical risks remain elevated, but valuations are turning more compelling, with REER pointing to meaningful rupiah undervaluation versus the US dollar. USDIDR has also moved into overbought territory, reducing the risk-reward of chasing USD upside at current levels.

-

Our base case is for near‑term rupiah stabilisation rather than a disorderly depreciation. We maintain our end‑Q2 USDIDR forecast at 17,000 and expect a gradual improvement in rupiah performance in subsequent quarters as stabilisation forces build. Active policy intervention has helped suppress FX volatility and slow the pace of USDIDR gains, while Indonesia’s sovereign CDS spreads have narrowed. Bank Indonesia continues to prioritise rupiah stability, keeping policy rates unchanged. We expect BI to hold rates in Q2 and only revisit easing once the rupiah has clearly stabilised.

-

We also think one of the most underappreciated story for the rupiah is the positive spillover from higher energy prices into non-energy commodity prices. This is currently not priced in by FX markets, in our view, but could be critical for a sustained turnaround in rupiah sentiment. From a flow perspective, we are seeing early signs of renewed foreign bond inflows, following sharp outflows in March.

-

Given unresolved Middle East risks and oil price uncertainty, we are not advocating aggressive USDIDR shorts at spot. Higher oil prices are still a drag on Indonesia’s trade and fiscal balance. That said, elevated USDIDR levels provide an attractive opportunity to layer into USDIDR hedges 12 months out. USDIDR downside remains a medium-term theme in our view. Unlike 2022–23, the Fed now appears constrained, reducing the likelihood of another sharp US rate shock. Given our anticipation for US rates and USD dynamics to turn lower over the next year or so, the rupiah should gradually benefit.