Ahead Today

G3: US NFIB Small Business Index, US Existing Home Sales

Asia: China Trade, Taiwan Exports

Market Highlights

The continued uncertainty around the Iran conflict continued, but with Iran and Israel agreeing to ease strikes against each other after a flare-up in violence threatened to derail peace negotiations with President Trump appealing for de-escalation. While there has been an easing of tensions, fundamental disagreements around fighting in Lebanon continues to be a crucial sticking point. Together with other major factors such as Iran’s enriched uranium stockpile, the status of the Strait of Hormuz, Iran’s assets, the road towards an eventual deal remains narrow for the time being even as appetite for significant re-escalation seems to be low for both US and Iran.

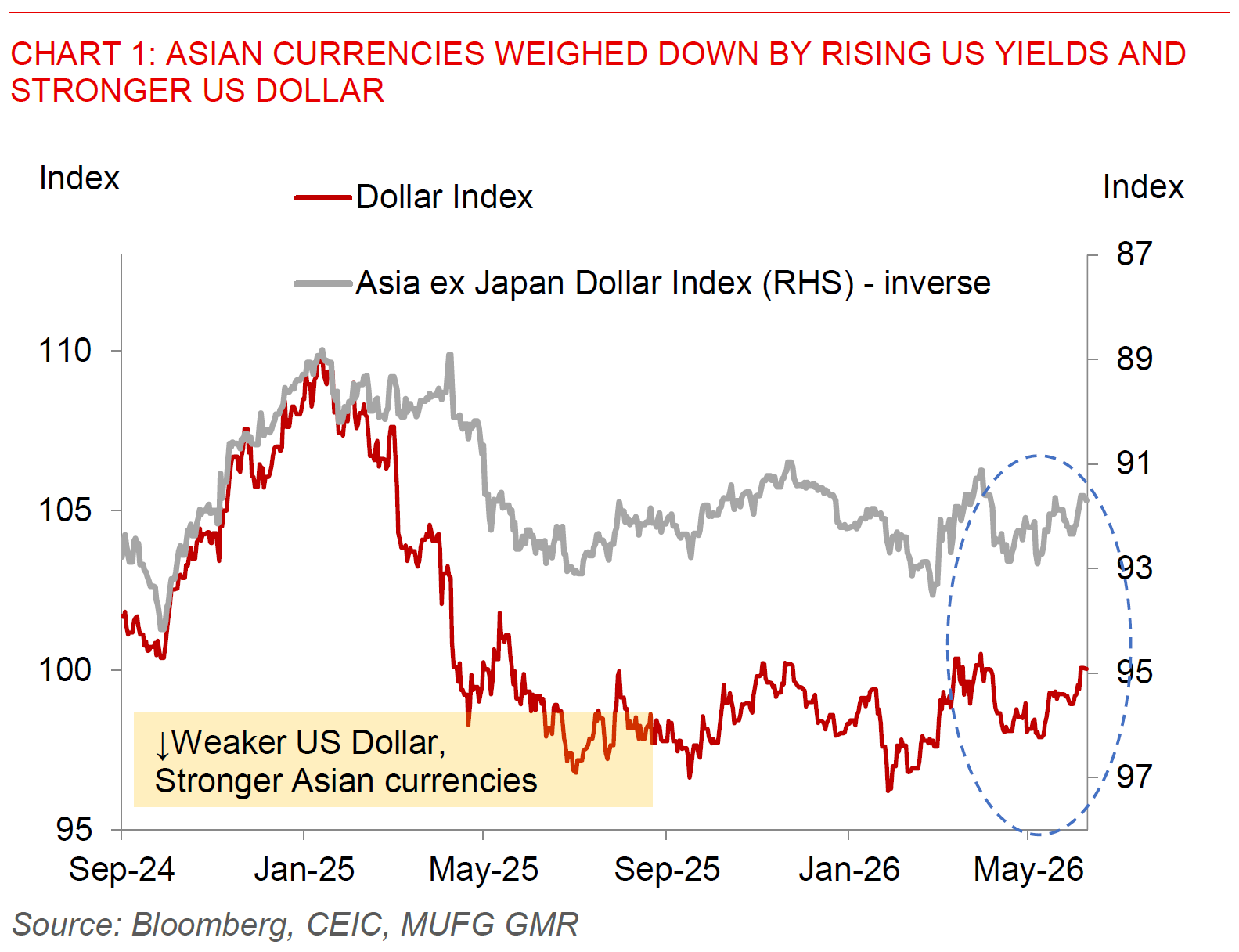

What’s more important for markets however has been the steady rise in US yields, and this has weighed on all markets, including AI tech stocks with massive volatility in the likes of KOSPI, a stronger Dollar and generally weaker Asian currencies as well. Some of this has been driven by the stronger string of US labour market data so far, and the upcoming CPI inflation numbers later this week will be important to see to what extent the Fed has the space to look through the impact of oil and energy prices. Fed Chair Kevin Warsh is also a key factor not just around his views on the appropriate measure of inflation to look at, but also around his proclivity to reduce the Fed’s balance sheet.

In that broader macro backdrop, it’s fair to say that many Asian central banks are increasingly pushing back against currency weakness, and in many instances also targeting the non-deliverable forward market. We have seen that in the likes of India earlier in late March to April when RBI drove a wedge between the onshore and offshore market, while more recently yesterday South Korea announced a plan to step up oversight of offshore currency derivatives, boost inspections into suspected market misconduct and probes of potential illegal foreign exchange transactions. Of course, beyond that South Korea actually put words into action by also activating the National Pension Service’s FX hedging requirements, and this in combination resulted in a sharp fall in USD/KRW by more than 1%. India’s latest salvo of measures to help shore up the Indian Rupee is also potentially quite meaningfully, by our estimate bringing in around US$40bn of inflows, and is one key reason why we see some near-term stability in INR notwithstanding global risks from both sticky US yields and the US-Iran conflict uncertainty (see India: Shoring up the Indian Rupee). We prefer more relative value FX plays for INR right now rather than USD/INR outright and see long CNH/INR on dips and buying INR against the likes of IDR as decent risk reward.