To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil heads for sharpest quarterly decline since 2020. Oil prices remained under pressure, with Brent trading above USD73/b and WTI near USD70/b, as improving flows through the Strait of Hormuz continued to ease supply concerns following progress in US-Iran peace negotiations. Brent is on track for its largest quarterly decline since the pandemic, reflecting the unwinding of the geopolitical risk premium as tanker traffic through the strait return toward normal levels. However, uncertainty remains over the next phase of negotiations, with the US expecting direct talks while Iran has indicated it will only send a technical delegation. Meanwhile, Iran reiterated its intention to oversee traffic through the Strait of Hormuz, highlighting that differences over the waterway’s future governance remain unresolved. Going forward, oil prices are likely to remain under downward pressure as Gulf supply recovers and the risk premium continues to fade, although uncertainty could keep volatility elevated.

Gold falls below USD4,000 as higher for longer rate expectations persist. Gold prices extended their decline, with gold falling to around USD3,943/oz, as conflicting signals from the US and Iran ahead of renewed peace talks failed to improve market sentiment. The metal has lost around 25% since the conflict began, pressured by expectations that central banks will keep interest rates higher for longer amid lingering inflation concerns, while a stronger US dollar has added further downside pressure. Disagreements over the future governance of the Strait of Hormuz also underscore that geopolitical risks remain unresolved despite ongoing diplomatic efforts. Gold is likely to remain under pressure in the near term as easing energy prices, a resilient US dollar, and higher for longer interest rate expectations continue to reduce demand for non-yielding safe haven assets.

MIDDLE EAST - CREDIT TRADING

End of day comment – 29 June 2026. Firmer markets. Crucially after last week’s outflow and daily widening, the flows changed a bit today. Most would have expected to see more outflows into month end. But dedicated EM RM was rather sidelined and not a sizeable seller. On the other hand, the local bid started to show up today in bonds which had widened more than the overall market. ADGB was a curve which had underperformed last week but traded well today, seen buyers of short end and belly bonds where 2.5 29s closed +0.1pt/-5bp and long end bonds where 70s closed +0.375pt/-3bp. Quasi sovgn are more technical, MUBAUH curve still has sellers and dealers are long, hence the curve closed broadly unch. But other names like ADQABU where the positioning is cleaner traded strong, 54s closed +0.375pt/-2bp. On the primary market side RAKBNK mandated a 5y and Mashreqbank a PNC 5.5 AT1 continuing the trickle of financial names. Month end flows tomorrow will be watched closely, but the market feels much more constructive than at the end of last week. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

Egypt advances IMF reform agenda. Egypt reached a staff-level agreement with the IMF on the seventh review of its reform program, paving the way for over USD1.6bn in additional financing, including USD1.5bn under the Extended Fund Facility (EFF) and USD136 million under the Resilience and Sustainability Facility (RSF), pending Executive Board approval. The agreement reflects continued progress on key structural reforms, including state asset sales, measures to strengthen public finances through tax reforms, and efforts to reduce the state’s role in the economy while encouraging greater private sector participation. The IMF also acknowledged Egypt’s commitment to a more flexible exchange rate regime, demonstrated by the Egyptian pound’s two-way movements during the recent regional conflict. Once approved, total IMF disbursements under the program will reach around USD7.2bn, reinforcing investor confidence, supporting external financing needs, and underpinning Egypt’s ongoing macroeconomic stabilization and economic reform agenda.

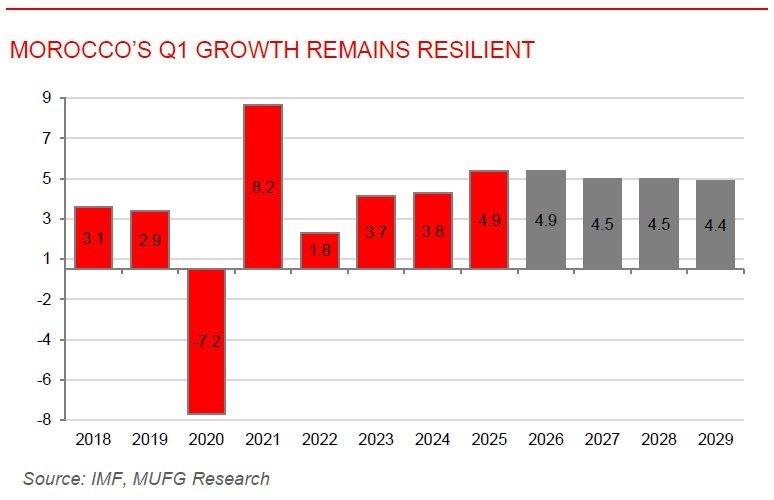

Morocco’s Q1 growth remains resilient. Morocco’s economy grew by 4.6% y/y in Q1 2026, supported by a strong rebound in agriculture and resilient domestic demand, despite weaker industrial activity. Agricultural output surged 18.4% following improved rainfall, offsetting slower 2.6% growth in the non-agricultural sector and a contraction in industrial activity. The data also showed solid macroeconomic fundamentals, with national savings reaching 31.4% of GDP, investment at 32.9% of GDP, and a modest financing gap of 1.5% of GDP. Morocco continues to stand out as one of the region’s more resilient economies, benefiting from diversified trade routes outside the Strait of Hormuz, contained inflation, and supportive monetary policy. Going forward, the sustainability of the agricultural recovery, a rebound in industrial production, and external demand, particularly from Europe, will be key factors determining whether Morocco can maintain its growth momentum through the rest of 2026.