To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil hits wartime high as escalation risks intensify. Oil prices surged to wartime highs, with Brent climbing above USDS122/b and WTI nearing USD109/b, as fears of renewed US military action against Iran and a prolonged disruption in the Strait of Hormuz drove market anxiety. President Trump is reviewing new military options while maintaining a strict naval blockade on Iranian ports, signalling a hardline stance amid stalled negotiations. The near-total shutdown of Hormuz, one of the world’s most critical energy chokepoints, has sharply reduced global oil and gas flows, fuelling what is the largest supply shock in modern energy markets. Iran has warned of retaliation if pressure continues, raising the risk of broader regional escalation, while the US is also intensifying economic measures, including tanker seizures and expanded sanctions. With supply tightening and geopolitical tensions rising, oil markets remain highly volatile and vulnerable to further upside shocks.

Gold rebounds slightly as Fed divisions and inflation risks weigh. Gold prices edged higher, rising about 0.7% to above USD4,580/oz, as dip-buying emerged after a three-day decline, even as a divided Fed kept interest rates unchanged. The central bank’s 8–4 split, the widest dissent in decades, highlighted growing uncertainty over policy, with some officials signalling concern about persistent inflation that could require higher rates, a negative for non-yielding gold. Rising Treasury yields further pressured gold, while the ongoing Middle East conflict, now in its ninth week, continues to fuel inflation risks through elevated energy prices and the near-total shutdown of the Strait of Hormuz. Despite the modest rebound, gold remains under pressure, down around 13% since the war began, although continued central bank buying has helped cushion the decline.

MIDDLE EAST - CREDIT TRADING

End of day comment – 29 April 2026. Another mixed day ahead of the Fed. Oil prices continue to go up and that in turn pressures UST. But with some price stickiness the higher yields still translate into tighter spreads overall as flows remain balanced. Like yesterday front end and belly are 2/3bp tighter on the flattening UST curve. Long end bond prices though reacted again more to the underlying yield move and closed unch/+1bp in spread terms. QATAR 50s was active and last down at 85.50 (-0.25pt/unch). In the ADGB curve 70s underperformed a touch closing -0.375pt/+2bp. OMAN had a strong day in the belly of the curve with buying interest in 28s-31s where cash even closed a touch higher in price and about -5/-6bp. Fins saw new EBIUH 6.25 perp trading very strong closing 100.625/100.875 from 100 reoffer. Early morning it traded up at 100.375, but most trades where around 100.75. A break of 5% in 30y bonds will probably be met by some outflows/selling first.

MIDDLE EAST - MACRO / MARKETS

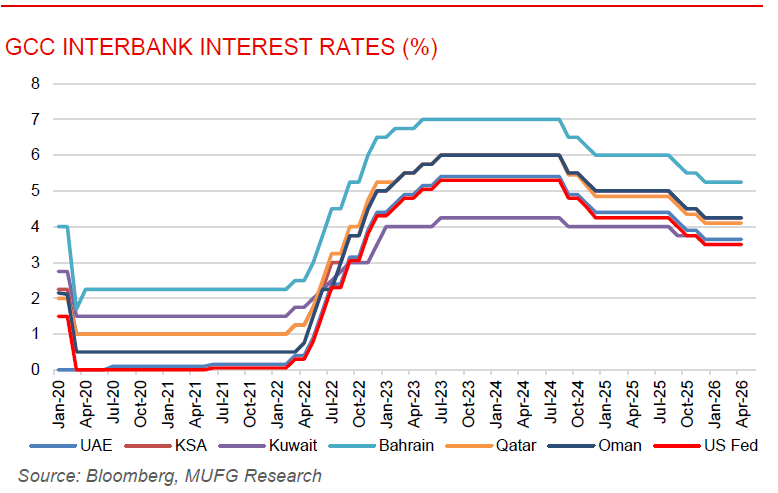

Gulf central banks maintain policy rate in line with Fed decision. Gulf central banks kept their key interest rates unchanged after the US Fed opted to hold policy rates steady, underscoring their commitment to monetary stability under dollar-pegged exchange rate frameworks. Qatar Central Bank kept its Deposit Rate at 3.85%, Lending Rate at 4.35%, and Repo Rate at 4.10%. The Central Bank of Bahrain held its overnight deposit interest rate at 4.25%, citing the need to maintain monetary and financial stability in light of global financial market developments. Similarly, the Central Bank of the UAE maintained its base rate on the overnight deposit facility at 3.65%, with short-term borrowing rates kept at 50bps above the base rate, a move explicitly noted as following the US Fed’s decision on reserve balances. The synchronized approach reflects the longstanding monetary policy alignment between Gulf states and the US, driven largely by their currencies’ pegs to the US dollar.

World Bank sees Middle East war to drive sharpest commodity price surge since 2022. The outbreak of war in the Middle East in early 2026 has caused unprecedented disruptions to global commodity markets, most critically through the near-total closure of the Strait of Hormuz, a chokepoint carrying roughly 35% of global seaborne crude oil trade. They project that the Middle East conflict will drive average commodity prices up 16% in 2026, the first annual increase since 2022, representing a 25% upward revision from January projections. Global energy prices are forecast to surge 24% this year, with Brent crude oil projected to average USD86/b, a steep rise from USD69/b in 2025, before reverting to USD70/b in 2027. Natural gas prices are expected to climb sharply on both sides of the Atlantic, with European prices projected to rise 25% and Japanese LNG prices forecast to surge nearly 33% this year. Fertilizer prices, particularly urea, are projected to soar 31% in 2026 due to export disruptions and surging natural gas input costs, pushing fertilizer affordability to its worst levels since 2022. The World Bank warns that risks are firmly tilted upward, if disruptions prove more protracted, Brent could average USD95/b to USD115/b, potentially pushing an additional 45 million people into acute food insecurity.