To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds near highs as Hormuz blockade extends supply crisis. Oil prices remained elevated, with Brent trading above USD111/b and WTI near USD100/b, as markets focused on stalled US-Iran peace talks and the continued near-closure of the Strait of Hormuz. President Trump said Iran has asked for the US naval blockade to be lifted during negotiations, but reports suggest the US is preparing for a prolonged blockade to further pressure Iran’s economy and oil exports. While a ceasefire has largely held since early April, shipping disruptions have severely curtailed flows of crude, natural gas, and refined products, fuelling inflation concerns and what the IEA has called the biggest supply shock in history. Iran is also facing growing storage constraints that could force deeper production cuts, while the US continues tightening sanctions on Chinese refiners linked to Iranian oil. The crisis has already triggered broader regional shifts, including the UAE’s decision to leave OPEC next month to gain greater flexibility in responding to market disruptions.

Gold steadies as Iran talks continue amid Hormuz inflation risks. Gold prices stabilised near USD4,590/oz, as investors balanced renewed US-Iran diplomatic efforts against persistent inflation risks tied to the prolonged closure of the Strait of Hormuz. President Trump said Iran has requested the US lift its naval blockade while negotiations continue, with mediators in Pakistan expecting a revised proposal from Iran in the coming days. However, the ongoing disruption to global energy supplies continues to drive inflation concerns, increasing expectations that major central banks, including the Fed, may keep interest rates elevated for longer. Higher bond yields and tighter monetary expectations have weighed heavily on non-yielding gold, which has now fallen around 13% since the conflict began while oil prices continue to surge.

MIDDLE EAST - CREDIT TRADING

End of day comment – 28 April 2026. Mixed day. Flows picked up compared to yesterday but overall remain well below an average trading day. Credit curves steepened, partly on the UST flattening but also on the continuous selling of long end bonds. Whilst spreads are anywhere from -2bp/+5bp depending on the part of the curve and the credit, cash prices are lower across the board. UAE announced they will leave OPEC and OPEC+, but the impact of this is yet to be seen and there was no market reaction to it today. ADGB and QATAR long end were +2/3bp with most activity in ADGB 54s (-0.50pt/+3bp) and QATAR 50s (-0.50pt/+3bp). Against this the 10y area saw more support with bids in ADGB 34s (-0.10pt/-2bp) and QATAR 35s sukuk -0.15pt/+0bp. Oman was quiet but saw some 47s clearing in the afternoon closing -0.25pt/+1bp. Quasis getting technical, QPETRO 31s remains well bid (unch/-3bp) whereas UAE index names saw again some selling , closing the MUBAUH curve up to 0.375pt lower and on average +2bp. In primary markets EBIUH priced its PNC6 AT1 at 6.25%. On the back of it saw some small selling in the outstanding 6.25 perp callable in 2030 which is still holding around 102 (YTC 5.71).

MIDDLE EAST - MACRO / MARKETS

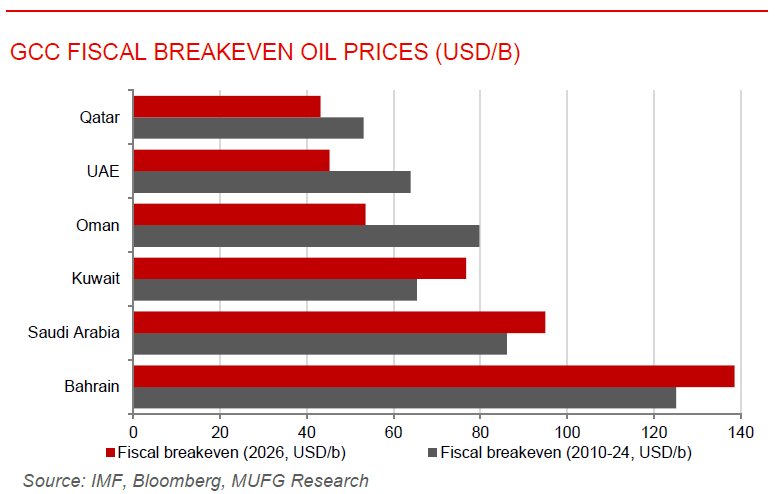

UAE decides to exit OPEC after six decades. The UAE announced that it will withdraw from OPEC and OPEC+ effective May 1, ending nearly six decades of membership and removing the cartel’s third-largest producer. The UAE described the decision as a policy-driven move aligned with its long-term energy strategy and national interest, citing the need for greater flexibility in managing production. The country’s capacity currently stands at around 4.85mb/d against actual output of roughly 3.2mb/d, with ADNOC targeting 5mb/d by 2027 under a USD150bn capex program. The exit comes amid the ongoing Iran war and the closure of the Strait of Hormuz, which has constrained Gulf production broadly. The decision follows earlier departures by Qatar and observers note it raises questions about OPEC’s long-term cohesion and pricing influence, particularly if other members reassess their commitments. Near-term market impact is expected to be limited given existing supply disruptions, though the longer-term implications for global oil governance remain a subject of active discussion. The move reflects a rational response to structural divergence, the UAE’s lower fiscal breakeven and diversified economy make volume-led monetisation a more efficient strategy than coordinated price defence, and the exit is likely to accelerate a broader shift from cartel-managed pricing toward market-driven dynamics.

Qatar inflation hits three-year high in March 2026. Qatar’s inflation accelerated sharply to 4.2% y/y in March, up from 2.5% y/y in February, marking the fastest pace of price growth in the country since February 2023. The jump represents one of the steepest single-month accelerations in Qatar’s recent inflation history, driven largely by the supply chain disruption and logistics cost surge that followed the Ras Laffan infrastructure attacks in March, which effectively halted LNG production and severely restricted import flows through the Strait of Hormuz. With the economy already under pressure from the production shutdown, Q2 2026 data will be the real test for Qatar.