To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil rises as Iran talks stall and Hormuz remains shut. Oil prices climbed again, with Brent briefly nearing USD108/b and WTI approaching USD97/b, as stalled US-Iran peace efforts and the continued closure of the Strait of Hormuz prolonged one of the biggest energy supply disruptions in recent history. While prices eased slightly after reports that Iran offered a new proposal to reopen the strait, negotiations remain fragile after President Trump cancelled planned talks in Pakistan and Iran rejected negotiations under military pressure. Despite a ceasefire largely holding since early April, dual US and Iranian blockades have reduced shipping through Hormuz to near zero, severely disrupting global supplies of crude, fuel, natural gas, and fertilizers. The conflict has triggered shortages in major importing countries, increased inflation concerns, and forced demand adjustments as supply losses mount. With US sanctions tightening and military interceptions continuing, markets remain highly sensitive to any signs of diplomatic progress or further escalation.

Gold slides as Iran talks stall and Hormuz disruptions persist. Gold prices fell to around USD4,670/oz as stalled US-Iran peace efforts and continued disruptions in the Strait of Hormuz kept inflation concerns elevated. President Trump cancelled planned talks in Pakistan while Iran refused negotiations under military pressure, though prices recovered slightly after reports that Tehran offered a new proposal to reopen Hormuz. The continued blockage of a key route for roughly one-fifth of global oil flows has sustained the energy shock, reinforcing expectations that central banks may keep interest rates higher for longer, a major headwind for non-yielding bullion. Gold has now fallen roughly 11% since the conflict began, while investors are also closely watching potential leadership changes at the Fed for clues on future monetary policy.

MIDDLE EAST - CREDIT TRADING

End of day comment – 24 April 2026. Another weak session. Whilst global markets had a bit of a rollercoaster on 'will they meet or not' GCC bonds were wider from the start and remained wider going out at the lows/wides. The Friday effect where no one wants to warehouse more risk than need over the weekend was in full swing. Add to that that most trades were initiated by sellers again. Both RM and ETFs remained sellers throughout the day, also in risk recovery phases. All said volumes remained low. Long end bonds generally -0.50/-0.625pt/+2bp. OMAN was also +2/3bp with steady outflows from ETFs. Quasi sovgn bonds were 3/5bp wider. Especially the UAE index names were again for sale and the market had little appetite to pick them up. ADQABU was most stable +3bp (35s -0.375pt) vs MUBAUH +5bp (35s -0.5pt). Qatari names held a touch better, with some activity in QPETRO, closing 41s -0.375pt/+2bp. Corps and fins continued to drift wider without finding many clearing levels. ALDAR hybrids were another -0.5pt/+10bp.

MIDDLE EAST - MACRO / MARKETS

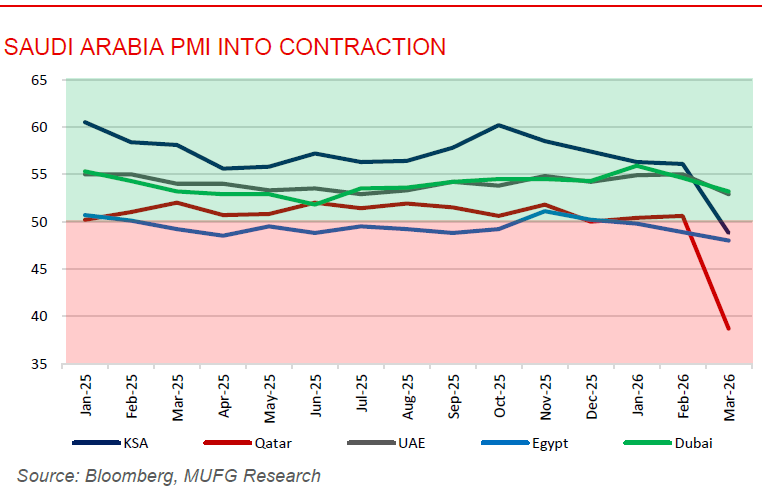

Saudi economy remains resilient despite oil disruptions. Saudi Arabia’s economy has shown notable resilience despite significant disruption from regional conflict, with higher oil prices helping offset a sharp decline in production and broader economic pressures. Saudi crude output fell 23% m/m in March to 7.76mb/d due to geopolitical disruptions, but a more than 60% surge in Brent prices helped cushion revenue losses. While uncertainty linked to the US-Iran conflict weighed on business activity, pushing the PMI into contraction at 48.8, and real estate transactions fell sharply, broader economic fundamentals remain relatively strong. Real GDP expanded 5% in Q4 2025, inflation remained contained at 1.8%, consumer spending rose 8.4%, and Saudi unemployment declined to 7.2%. Non-oil diversification also continued to gain traction, with non-oil exports rising 15.1% y/y to USD8.3bn, supported by stronger re-exports and trade links with key partners such as the UAE, India, and China. Despite emerging fiscal pressures from weaker oil volumes and higher spending, the outlook remains relatively constructive, with the IMF projecting 3.1% growth in 2026 as the kingdom continues advancing its Vision 2030 agenda.

Saudi Arabia’s Vision 2030 enters third phase with 93% of target met. Saudi Arabia released its Vision 2030 Annual Report for 2025, revealing that non-oil activities now account for 55% of real GDP, the private sector contributes 51%, and real GDP grew 4.5% in 2025, the highest annual expansion in three years, with 309 out of 390 performance indicators achieving their interim goals, a 93% completion threshold. GDP reached SAR4.9 trillion (USD1.3trillion) by end-2025, exceeding the interim target, with more than 700 international companies having established regional headquarters in the Kingdom, FDI stock up 119% since 2017, and SME financing climbing to 11.3% of total bank loans. Non-oil government revenues surged more than 170% from SAR185.7bn in 2016 to SAR 505bn in 2025, while Saudi unemployment fell to 7.2% from 12.3% at the programme’s launch. The Finance Ministry projects GDP growth of 4.6% in 2026 as the Kingdom enters Vision 2030’s third and final phase.