To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil set for weekly loss despite renewed Hormuz security concerns. Oil remained on track for a weekly decline as increasing flows through the Strait of Hormuz continued to ease supply concerns, although a reported attack on a commercial cargo vessel near Oman highlighted that security risks remain elevated. Brent traded near USD74/b and WTI around USD71/b, with prices recovering modestly after the incident but still heading for a third consecutive weekly loss. Gulf producers, including the UAE, Kuwait, Qatar, and Iraq, are ramping up production and exports as diplomatic negotiations between the US and Iran continue, helping to restore regional supply. However, shipping disruptions, limited tanker availability, and uncertainty over safe navigation through Hormuz continue to slow the pace of normalisation. Oil prices are likely to remain range bound in the low-to-mid USD70/b as improving supply fundamentals offset geopolitical risks, although any renewed security incidents in Hormuz could temporarily restore part of the geopolitical risk premium.

Gold stabilises as softer US inflation eases rate hike expectations. Gold stabilised near USD4,000/oz after softer-than-expected US inflation data reduced expectations for further Fed rate hikes, providing some relief following a sharp multi-week selloff. The US personal consumption expenditures (PCE) index rose less than anticipated, leading Treasury yields and the US dollar to ease, although gold remains on track for a fourth consecutive weekly decline. Gold has come under sustained pressure from the Fed’s hawkish stance and higher for longer interest rate expectations, which have reduced the appeal of non-yielding assets. Softer inflation data may help stabilise gold prices in the near term, but a sustained recovery is likely to deepen on clearer signs of Fed policy easing or a renewed increase in geopolitical uncertainty.

MIDDLE EAST - CREDIT TRADING

End of day comment – 25 June 2026. The spread widening continues, albeit the market was a bit more constructive today. Sellers retreated a bit today in the morning as risk markets were on the front foot. All said, there was no buying either. In the afternoon with risk turning mixed, we started seeing again mainly ETF selling the same bonds as recently. The steepening of the UST curve post US numbers leads to a flattening in credit curves. Shorter end and belly bonds close on average +2/3bp whilst long end bonds close broadly unchanged in spreads. Cash prices remain sticky, but with the better risk tone in the morning sovgn bonds were up to 0.25pt higher. The market will be a bit concerned that there hasn't been any meaningful take out of bonds, dealers are still long, and month end flows are about to hit the screens. It will take more than risk on in macro markets to see spreads moving tighter, what GCC bonds need is a change in flows. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

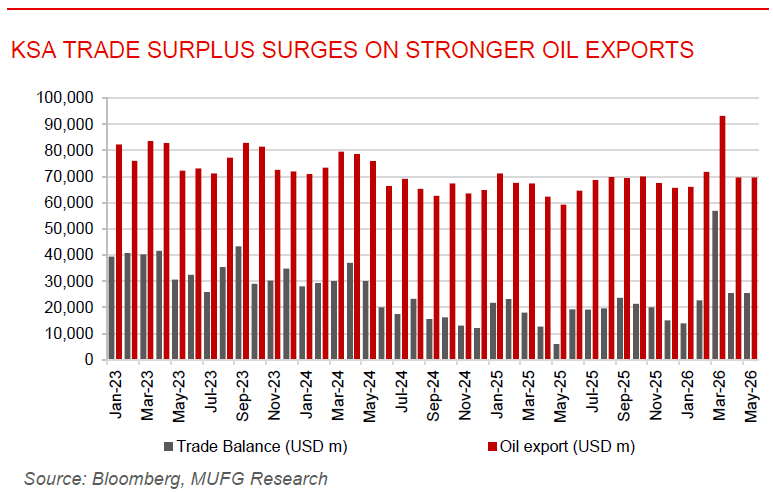

Saudi Arabia trade surplus surges on stronger oil exports and lower imports. Saudi Arabia’s merchandise trade surplus more than doubled to SAR25.4bn (USD6.8bn) in April 2026, supported by stronger oil exports and lower imports, reinforcing the Kingdom’s external position. Total exports increased 9.3% y/y, driven by an 11.7% rise in oil exports, while imports declined 5.2%, boosting the overall trade balance. The data also pointed to continued progress in economic diversification, with the ratio of non-oil exports to imports rising to 41.6% from 37.8% a year earlier. Re-exports remained particularly strong, increasing 20.4%, while machinery and electrical equipment recorded robust growth, highlighting expanding industrial and logistics activity. China remained Saudi Arabia’s largest trading partner for both exports and imports, followed by the UAE and South Korea on the export side. The stronger trade surplus reflects Saudi Arabia’s resilient export infrastructure during the regional conflict and continued progress under Vision 2030, although lower oil prices and recent Aramco official selling price (OSP) cuts could moderate external balance improvements in the second half of 2026.

Kuwait expands debt issuance to fund wider fiscal deficit. Kuwait issued KWD550 million (USD1.8bn) in Treasury bonds and Islamic tawarruq across four maturities, bringing total domestic debt issuance to KWD1.25bn in FY2026/27 as the government steps up financing to address a widening fiscal deficit. The increased borrowing reflects the impact of the US-Iran conflict on Kuwait’s public finances, with the country remaining one of the GCC’s most exposed economies to disruptions in the Strait of Hormuz due to its heavy reliance on oil export revenues and limited alternative export infrastructure. The issuance follows the reactivation of Kuwait’s debt law in 2025, while strong demand from local banks underscores ample domestic liquidity and continued investor confidence in sovereign debt. Going forward, the pace of fiscal borrowing will largely depend on the recovery of oil export revenues as Hormuz traffic normalises, although Kuwait’s strong domestic funding base should continue to provide stable market access despite ongoing geopolitical uncertainties.