To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil falls below pre-war levels as Hormuz flows normalise. Brent crude fell below its pre-war level of around USD72.5/b, easing all gains made during the conflict as outflows through the Strait of Hormuz continued to recover following progress in US-Iran peace negotiations. Increased exports from the Middle East, alongside additional supplies from Africa and temporary easing of restrictions on Iranian oil sales, have significantly improved market availability, pushing both physical crude prices and prompt spreads into a more bearish structure. Although negotiations remain ongoing and uncertainties persist over issues such as Iran’s nuclear program, shipping fees through Hormuz, and sanctions implementation, the market is increasingly pricing in a sustained normalisation of supply. The rapid recovery in Gulf exports and fading geopolitical risk premium are likely to keep Brent trading around the low-USD70s in the near term, although low global inventories should prevent a sharper decline.

Gold extends decline on strong dollar and hawkish Fed outlook. Gold extended its losses, falling below USD4,000/oz for the first time since November, as a stronger US dollar and expectations of higher interest rates continued to weigh on investor sentiment. The decline reflects growing confidence that the Fed will maintain a tighter monetary policy stance, reducing the appeal of non-yielding assets such as gold. The recent selloff has also pushed gold into bear market territory, ending a multi-year rally that had been supported by strong central bank buying and safe-haven demand. While easing geopolitical tensions and lower energy prices have reduced inflation fears, the stronger dollar and improving relative attractiveness of US assets have further pressured precious metals.

MIDDLE EAST - CREDIT TRADING

End of day comment – 24 June 2026. Ugly day in terms of spread moves. Cash prices were in essence irresponsive to the UST rally. Flows remained skewed to selling and on balance the street is long. Dealers are awaiting the month end outflows in UAE names and are not in a hurry to step up bids. The small trickle in new issuance does the rest. ADGB closed +6/7bp with the curve up to 0.125pt higher in long end, seen sellers in the 10y area esp 34s (unch/+7bp). QATAR did a touch better with some buyers in 50s (+0.375pt/+4bp). QPETRO curve came a bit to life today. Seen sellers of the recent 29s PP (unch/+5bp) and 31s (unch/+5bp) but 51s had better bid (+0.5pt/+2bp). In UAE quasis MUBAUH (+6/7bp) remains weakest with continuous outflows from RM/ETF in belly bonds. In fins seen a bit more activity in new FABUH 36s T2 wich closed 100.125/375. On the back of it though outstanding AT1 in UAE remained for sale. DUKHAN will price its new AT1 at 6%. Technicals still look weak overall but with the widening in the last two days some value in spreads is opening up. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

Iran seeks new Asian buyers as temporary sanctions relief boosts oil exports. Iran is moving quickly to expand its oil exports following a 60-day US sanctions waiver, actively marketing crude to refiners across India, Japan, South Korea, and other Asian markets in an effort to diversify beyond its traditional reliance on China. Iran is also seeking to clear an estimated 68mb of crude and condensate currently held in floating storage while negotiating longer-term supply agreements. However, buyer interest remains cautious as Asian refiners are already well supplied, uncertainty persists over the durability of US sanctions relief, and financing, insurance, and shipping restrictions remain significant obstacles. Combined with signs of short-term oversupply in Middle Eastern crude markets, Iran may need to offer meaningful discounts to attract new customers. The sanctions waiver will support a gradual recovery in Iranian exports, but a rapid return to pre-sanction market share is unlikely given weak regional demand, abundant supply, and continuing geopolitical and regulatory uncertainties.

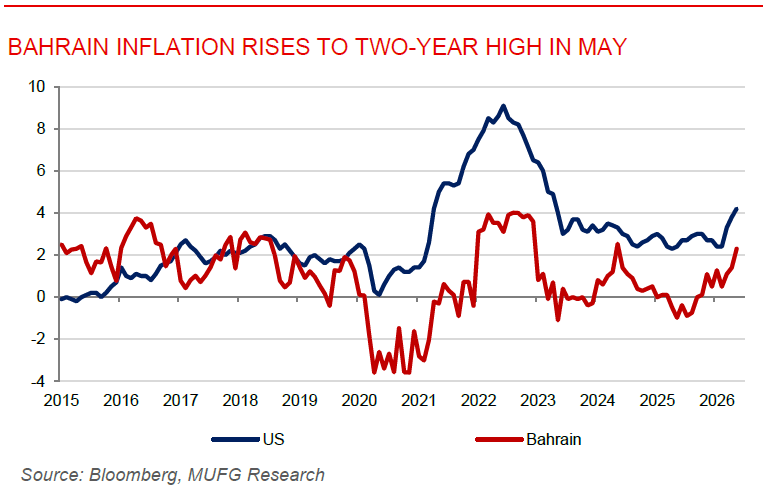

Bahrain inflation rises to two-year high in May. Bahrain’s inflation rate accelerated to 2.3% y/y in May, up from 1.4% y/y in April, marking its highest level since May 2024. The increase was mainly driven by stronger price pressures in food and non-alcoholic beverages, where inflation rose to 5.7%, alongside elevated growth in transport prices at 10.4% and education costs at 2.8%. On a monthly basis, consumer prices increased by 0.4%, after remaining flat in April. While Bahrain’s inflation remains relatively contained compared with many emerging markets, the latest increase suggests renewed household cost pressures and may keep monetary conditions tighter for longer, particularly given the country’s exchange rate peg and close alignment with US Fed policy. Going forward, Bahrain’s economy is likely to remain supported by steady non-oil activity, infrastructure investment and financial-sector resilience, but higher living costs and elevated borrowing rates could weigh on household consumption and private sector credit demand if inflationary pressures persist.