To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil extends decline as Hormuz traffic recovers and peace talks advance. Oil prices continued to fall as shipping activity through the Strait of Hormuz showed further signs of normalisation and US-Iran negotiations made incremental progress. Brent dropped below USD77/b while WTI traded near USD73/b, with tankers increasingly transiting the waterway openly and international authorities reporting improved maritime safety conditions. Additional supply is returning to the markets as the UAE has restored most of its pre-war production levels, while Kuwait and Iraq are also ramping up exports. The temporary easing of restrictions on Iranian oil exports has further reinforced expectations of a significant increase in regional supply. Although negotiations remain complex and questions persist over the future governance of Hormuz, the market is increasingly pricing in a gradual normalisation of Middle East energy flows. Going forward, the continued recovery in Gulf exports and fading geopolitical risk premium should keep downward pressure on oil prices.

Gold falls as stronger dollar and market selloff weigh on demand. Gold declined for a second consecutive session, falling below USD4,070/oz, as a stronger US dollar and a broad market selloff reduced investor demand for precious metals. The decline was driven by risk-off sentiment in global markets, with investors liquidating gold positions to cover losses elsewhere, particularly following weakness in technology stocks. At the same time, expectations of higher-for-longer interest rates continue to pressure gold, as persistent inflation concerns and the Fed’s hawkish stance have reinforced the likelihood of tighter monetary policy. While geopolitical risks have eased following progress in US-Iran negotiations, inflation remains elevated and continues to support a strong dollar environment.

MIDDLE EAST - CREDIT TRADING

End of day comment – 23 June 2026. Today weak technicals around the UAE index exclusion was flanked by weakness in broader risk markets. Flows remained sellers:buyers 2:1 with the picture again being RM and ETFs selling. At end of day cash prices are lower and UST higher, a classic risk off spread widening. Front end and belly bonds were +3/5bp, long end bonds closed +1/3bp. UAE names saw again most of the selling. In the sovgn space ADGB 49s was the weakest closing -0.375pt/+4bp. In quasi sovereigns MUBAUH underperformed closing up to 0.375pt lower and 3/5bp wider. New FABUH T2 has a reasonable start being priced +5/10bp to outstanding T2s, most morning trades were around 100.25 but it fell back into the close to 100. DUKHAN announced a mandate of 500mm PNC 5.5 AT1 sukuks. Whilst month end is still a few days ahead, the market expects to see more index related outflows. The absorption levels of this flow will depend on the broader macro picture as volatility in global markets increases. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

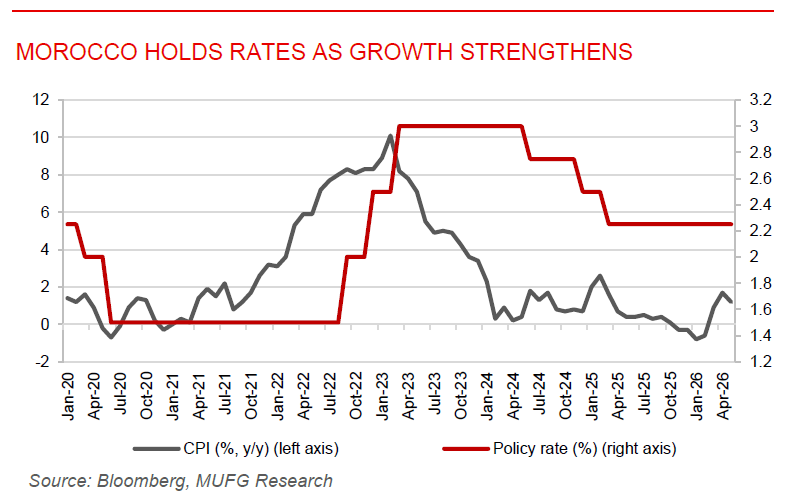

Morocco holds rates as growth strengthens as inflation moderates. Morocco’s central bank kept its benchmark interest rate unchanged at 2.25%, balancing support for strong economic growth and World Cup-related infrastructure investment against lingering inflation and external risks. Economic activity continues to strengthen, supported by improved agricultural output and large-scale spending ahead of the 2030 FIFA World Cup, while inflation eased to 1.2% y/y in May from 1.7% y/y in April due to lower food prices and better domestic supply conditions. Despite the moderation in inflation, policymakers remain cautious given uncertainty surrounding global economic conditions and the impact of recent Middle East tensions on energy prices. The central bank also raised its current account deficit forecasts for 2026-27, reflecting higher import costs and external pressures. In our view, Morocco remains one of the more resilient economies in North Africa, with strong investment momentum and contained inflation likely allowing the central bank to maintain an accommodative policy stance while monitoring external risk.

UAE oil exports recovers as supply routes prove resilient. UAE oil exports recovered to approximately 4.3mb/d in early June, or around 85% of pre-war levels, highlighting the country’s ability to maintain energy flows despite disruptions in the Strait of Hormuz. The recovery was supported by the Habshan-Fujairah pipeline, strategic storage facilities near Fujairah, and alternative shipping arrangements that allowed crude to continue reaching international markets. ADNOC also utilised its own tanker fleet and flexible logistics networks to sustain exports throughout the conflict. These measures helped mitigate the global supply shock and prevented oil prices from reaching the extreme levels initially feared by the market. With the US-Iran interim agreement now in place and maritime traffic gradually normalising, UAE export volumes are expected to continue recovering. The UAE’s strong infrastructure, storage capacity, and export flexibility have reinforced its position as one of the region’s most resilient energy exporters, while supporting its longer-term strategy.