To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil extends rally as Iran talks stall and Hormuz disruption persist. Oil prices rose for a fifth straight session, with Brent climbing above USD106/b and WTI nearing USD97/b, as stalled US-Iran negotiations and escalating military tensions continued to threaten energy flows from the Persian Gulf. President Trump intensified pressure on Teheran by maintaining a naval blockade, ordering action against vessels in the Strait of Hormuz, and overseeing the seizure of Iranian-linked oil shipments, further complicating diplomatic efforts. The near-closure of Hormuz has sharply reduced exports from major Gulf producers, adding a significant geopolitical premium to prices and keeping shipping activity largely frozen. With negotiations deadlocked over Iran’s nuclear program and broader regional conflicts, markets are increasingly pricing in prolonged supply disruptions, while investors estimate Gulf oil production could take months to normalise even if shipping routes fully reopen.

Gold heads for weekly loss as Hormuz standoff fuels inflation fears. Gold declined to around USD4,670/oz as escalating US-Iran tensions undermined hopes for a diplomatic breakthrough. President Trump intensified the maritime standoff by ordering the US navy to target vessels laying mines in the Strait of Hormuz, while both US and Iran continued blockades that have severely disrupted global energy supplies. The US also intercepted oil tankers, and Iran reportedly attacked multiple vessels, further escalating risks around a key global shipping route. Rising oil prices and prolonged supply disruptions have reinforced inflation concerns, increasing expectations that central banks may keep interest rates elevated for longer, a major headwind for non-yielding gold. With peace talks showing little progress and geopolitical risks remaining high, gold has now fallen roughly 11% since the conflict began.

MIDDLE EAST - CREDIT TRADING

End of day comment – 23 April 2026. Very weak day in spread terms. The macro markets were risk off on the open with credit indices wider and stock futures lower. That led to an initial 1-2bp widening in my names. Macro recovered in the afternoon, but outflows from RM, especially in UAE index names kept cash prices pressured here and spreads kept on widening with the UST recovery. At EOD, we closed our space anywhere from 3/10bp wider. ADGB was broadly +5bp with long end 0.5pt lower and the belly 0.125/0.25pt lower. The curve was active with mainly 34s and 47s trading. QATAR continues to outperform but was wider as well, I close it +3bp. Long end bonds recovered throughout the day closing -0.125pt/+2bp with the main activity in 49s. The belly though was +4bp with continuous selling in 35s (-0.25pt/+4bp). OMAN was weak to start but recovered with macro as it is not affected by the index linked outflows. We close that curve broadly +2bp with cash unch/-0.25pt. Quasi sovgn names broadly mirrored the respective sovgn moves, in the UAE space index names like ADQABU, ADNOCM, ADNOUH, MUBAUH or DPWDU saw RM selling and underperformed.

MIDDLE EAST - MACRO / MARKETS

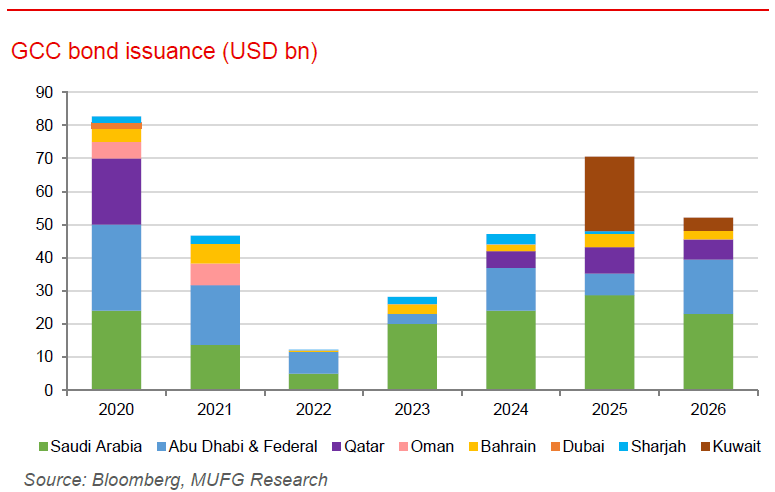

Saudi Arabia bond to join JPMorgan EM index 2027. JPMorgan plans to include Saudi Arabia’s local-currency bonds in its widely followed Government Bond Index-Emerging Markets in early 2027, marking a significant step in the kingdom’s efforts to attract more foreign capital and deepen its integration into global financial markets. The inclusion will begin gradually from January 2027 and eventually give Saudi bonds a 2.52% weighting, which is expected to improve market liquidity and attract passive investment flows from global funds that track the benchmark. The move comes at a critical time as Saudi Arabia ramps up spending on Vision 2030, which requires substantial financing for large-scale infrastructure, tourism, and economic diversification projects. It could also help the kingdom manage the financial fallout from regional geopolitical tensions, including disruptions linked to the Iran war, by broadening its investor base and supporting long-term capital inflows.

PIMCO emerges as key Gulf debt buyer amid war uncertainty. PIMCO has emerged as a major source of funding for Gulf governments as they build financial buffers against the economic fallout from the Iran war, lending more than USD10bn through private bond placements since late February. The asset manager has been a key buyer of privately issued debt from Abu Dhabi, Qatar, Kuwait, and Qatar National Bank, accounting for the majority of the region’s more than USD13bn in private debt issuance since the conflict began. Gulf states have increasingly turned to private placements as public bond markets remain largely shut amid heightened geopolitical risks, the near-closure of the Strait of Hormuz, and disruptions to energy exports that have pressured government revenues. While private debt tends to be more expensive, it offers faster and more flexible access to capital, helping governments navigate rising fiscal uncertainty as regional tensions persist. The trend also highlights growing financial caution in the Gulf, with some states even exploring contingency tools such as US currency swap lines to safeguard liquidity if the conflict worsens.