To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil stabilises as US-Iran talks progress and Iranian supply returns. Oil prices steadied after a sharp decline driven by early progress in US-Iran peace negotiations and a US waiver allowing limited Iranian oil exports. Brent traded near USD78/b while WTI held above USD74/b, as markets weighed the prospect of additional Iranian supply against ongoing uncertainties surrounding the broader peace process. The temporary waiver provides Iran with an important economic boost and could accelerate the return of Iranian crude to global markets. At the same time, Gulf producers including Kuwait, the UAE, and Qatar are gradually increasing exports and shipping activity as conditions in the Strait of Hormuz improve. While key issues, including Iran’s nuclear program, the Lebanon ceasefire, and the full reopening of Hormuz, remain unresolved, the market is increasingly pricing in a normalisation of regional energy flows. In our view, oil prices are likely to remain under pressure as supply recovers and risk premiums continue to unwind.

Gold falls as inflation concerns and hawkish Fed weigh on sentiment. Gold declined below USD4,140/oz as persistent inflation concerns and expectations of tighter monetary policy outweighed optimism surrounding ongoing US-Iran peace negotiations. Rising energy costs linked to the Middle East conflict have strengthened the case for higher interest rates, with Fed officials continuing to emphasise inflation risks and a commitment to price stability. The stronger US dollar and hawkish policy outlook have further reduced the appeal of non-yielding assets such as gold. While diplomatic progress between the US and Iran, including discussions on maritime security and limited Iranian oil exports, has helped reduce geopolitical tensions, these developments have provided only modest support for gold.

MIDDLE EAST - CREDIT TRADING

End of day comment – 22 June 2026. Cash adjusted to the left this morning on the back of the rates move, but spreads were still -2/-3bp in the morning. During the day though outflows from RM and ETFs pushed spreads to unch. Sellers outnumbered buyers in a ratio of 2:1. It was again mainly the index names which got sold in the sovgn and quasi sovgn space. We also saw selling in AT1 and fins generally on the back new FABUH T2 10NC5.5 which will price at T+140bp for 750mm USD. Mind FABUH just priced a PP 5y USD and 750mm EUR bond, so there is a bit of a realisation that new supply might hit the market bigger than thought, the 3.5bn QPETRO 29s PP last week is another proof of this. IG sovgn close up to -0.5pt and unch/-1bp. SHJGOV/SHARSK again outperformed on lack of selling from RM side closing up to -0.25pt and -2/-3bp. In fins FABUH 34s/35s T2 closed -0.25pt/+4bp on the back of the new issuance. The corps space firmed up in ALDAR hybrids (+0.125pt/-5bp) and DPWDU (unch/-3bp) as news around US/Iran negotiations pointed to progress. (Source: Matthew Dunker, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

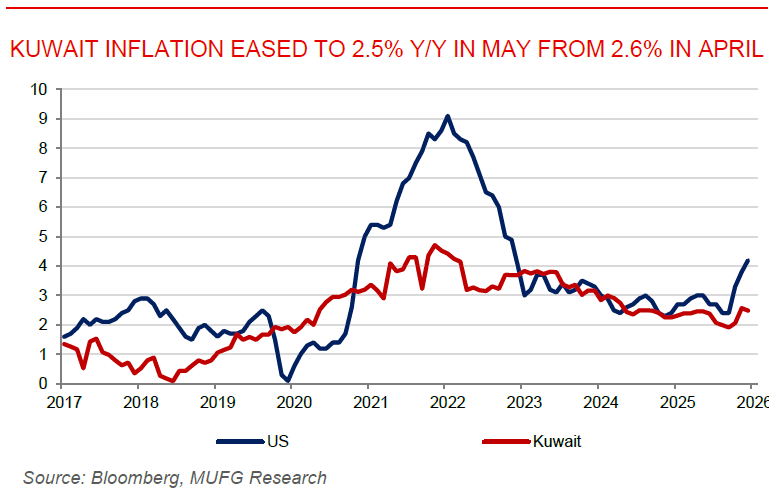

Kuwait inflation remains contained as energy exports resume. Kuwait’s inflation eased to 2.5% y/y in May from 2.6% y/y in April, with monthly inflation remaining subdued at just 0.07%, reinforcing its position as one of the GCC’s lowest inflation economies. While prices continued to rise across food, healthcare, education, and clothing, overall inflation remains well contained compared with regional peers. On the energy front, Kuwait is taking steps to normalise exports following the US-Iran peace framework, with Kuwait Petroleum Corp. offering naphtha cargoes for direct pickup from ports inside the Persian Gulf, requiring transit through the Strait of Hormuz. The move, alongside the lifting of force majeure notices and plans to increase oil production, signals growing confidence in the gradual recovery of regional energy flows. However, shipping activity through Hormuz remains subject to security risks, suggesting that a full normalisation of trade and export volumes may still take time.

UAE accelerates post-Hormuz diversification strategy. The UAE is advancing a long-term strategy to reduce its dependence on the Strait of Hormuz by expanding eastern ports, pipelines, and transport infrastructure, building on the existing Habshan–Fujairah pipeline that already bypasses the chokepoint. The initiative reflects lessons learned from the recent regional conflict and aligns with broader efforts to strengthen supply-chain resilience and economic diversification. In addition, the UAE is reinforcing its capital markets through measures such as retail sukuk market expansion, bank funding activity, and strategic overseas investments. The strategy also supports the country’s ambition to raise oil production capacity to around 5mb/d by 2027, while enhancing its role as a regional logistics and investment hub through projects such as the UAE-Oman rail link and the Aqaba rail corridor. We expect the UAE is emerging as one of the key beneficiaries of the post-war regional landscape, leveraging infrastructure investment, energy capacity expansion, and capital-market development to strengthen both economic resilience and long-term growth prospects.