To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil extends rally as Hormuz standoff persists. Oil prices rose for a fourth straight session, with Brent nearing USD104/b and WTI around USD95/b, as tensions between the US and Iran intensified following failed peace talks and an ongoing battle over the Strait of Hormuz. President Trump said the ceasefire would remain in place indefinitely while awaiting a new Iranian proposal, but Iran signalled no immediate plans to return to negotiations. Meanwhile, the US continues its naval blockade of Iranian-linked vessels, while Iran has kept Hormuz largely closed to international traffic and reportedly fired on commercial ships, deepening supply disruptions. The conflict has sharply reduced energy flows from the Gulf, driving a strong rally in oil prices, while falling US inventories and record exports highlight growing reliance on American supplies to offset shortages. With little progress on diplomacy and major geopolitical issues still unresolved, markets are increasingly pricing in prolonged supply disruptions rather than temporary headline-driven volatility.

Gold falls as Hormuz crisis sustains inflation pressures. Gold prices declined, falling as much as 1% to below USD4,700/oz, as President Trump extended the US-Iran ceasefire but failed to ease broader concerns over energy security. While the truce reduces the immediate risk of renewed military strikes, tensions remain high around the Strait of Hormuz, where the US continues its naval blockade and Iranian forces have targeted commercial vessels, keeping global energy flows disrupted. Rising oil prices and a stronger US dollar added pressure on gold, while persistent inflation risks from the prolonged energy shock have reinforced expectations that central banks may keep interest rates elevated for longer. As a result, gold continues to face headwinds despite ongoing geopolitical uncertainty.

MIDDLE EAST - CREDIT TRADING

End of day comment – 22 April 2026. We are on the record saying the market has moved on from the conflict and we continued to see evidence of that in the market today after this flubbed deadline (definitely not a deadline) back and forth last night. This week we have taken all my GCC benchmarks inside the z spread levels we had pre-war so this isn't exactly a bold statement, but we were surprised to see BHRAIN underperform a bit today on the back of the extended close of the Strait. Honestly, we would have thought that the potential for this to drag out for another month would have had more of an impact on BHRAIN, Kuwait, and Qatar. As mentioned, Bahrain curve ticked wider through the day with selling focused more on mid curve bonds in 35s and 36s, but generally 8-10bps wider across on lower TRAX volumes than average.

MIDDLE EAST - MACRO / MARKETS

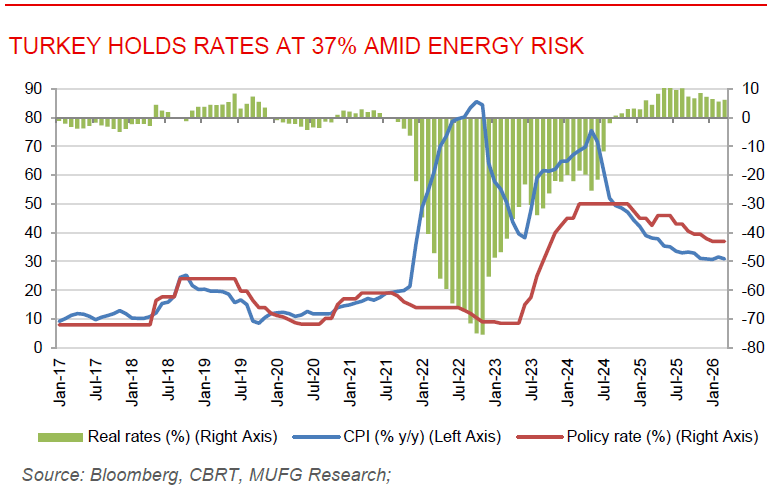

Turkey holds rates at 37% amid inflation and energy risks. The Central Bank of Turkey (CBRT) kept its key policy rate unchanged at 37%, while maintaining a tightening bias as it remains highly alert to inflation risks stemming from volatile energy prices and broader geopolitical disruptions. The CBRT noted that underlying inflation eased in March but could rise slightly in April, warning that any significant and persistent deterioration in the inflation outlook may require further tightening. While slowing domestic economic activity offers some relief, policymakers remain concerned about second-round inflation effects from higher oil prices and potential spillovers into food and core goods prices. Despite the external shock, Turkey’s economic framework has remained relatively resilient, with dollarisation stable at around 40%, limited pressure on foreign exchange markets, and reserves helping absorb temporary capital outflows. The CBRT’s slightly faster currency depreciation path is seen as a measured response to external pressures rather than a policy shift. Overall, the base case remains for rate cuts to resume in mid-2026 if geopolitical tensions ease and energy prices decline, with the policy rate expected to end the year at 31%, though risks remain tilted toward tighter policy if inflation pressures persist.

UAE property market maintains strong growth in Q1 2026. The United Arab Emirates real estate sector posted a strong start to 2026, with transaction volumes and values rising across major emirates, underscoring sustained investor demand and continued momentum in the property market. Dubai led activity, with transaction values surging 31% y/y to approximately USD68.6bn, alongside growth in total investments and new investors. Abu Dhabi recorded its strongest quarter on record, with transaction values jumping to roughly USD18bn, up from about USD6.9 billion a year earlier, while deal volumes nearly doubled. Sharjah also posted robust growth, with trading volumes reaching around USD5bn, up more than 40%, supported by broader international participation from investors across 113 nationalities. Meanwhile, Ajman maintained steady expansion, with total real estate transactions reaching approximately USD1.7bn. Overall, the broad-based growth across all major emirates reflects strong domestic and foreign investor confidence, continued capital inflows, and resilient demand across the UAE’s property sector.