To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil stabilises as Trump signals progress toward Iran deal. Oil edged higher after a sharp selloff, as President Trump said the US was in the “final stages” of negotiations with Iran, raising hopes for a potential reopening of the Strait of Hormuz and a gradual recovery in energy flows. Brent traded above USD105/b while WTI hovered near USD99/b, though prices remain more than 40% higher since the conflict began in late February. Markets continue to swing on conflicting headlines around ceasefire negotiations, with traders balancing the possibility of a near-term de-escalation against ongoing geopolitical risks. Despite tentative signs of increased tanker activity through Hormuz, energy executives warned that full normalisation of Middle East oil supply may not occur until 2027 due to the scale of disruptions caused by the conflict. Meanwhile, declining US crude inventories and continued uncertainty over Iran’s response to the latest US proposal are keeping oil markets volatile.

Gold steady as Iran deal hopes ease rate-hike expectations. Gold traded little changed near USD4,540/oz as optimism around a potential US-Iran agreement eased concerns over prolonged inflation and aggressive interest-rate hikes. President Trump said negotiations with Iran were in the “final stages”, supporting hopes for a reopening of the Strait of Hormuz and lower energy prices. Softer Treasury yields and a weaker dollar also provided support for gold. However, uncertainty around the conflict and Fed policy continues to limit stronger gains, with Fed meeting minutes showing officials remain concerned about persistent inflation. Gold has traded within a relatively narrow range in recent weeks and remains down around 14% since the war began in late February.

MIDDLE EAST - CREDIT TRADING

End of day comment – 20 May 2026. Another day where our pricing was entirely subordinate to the rates market, though we are lagging this move lower in rates a bit after we lagged the move higher in rates earlier in the week, so it makes sense in a way. The notable difference between today and earlier in the week is that the ETF arbs were super active in the morning. {IEMB LN Equity <GO>} went out quite negative last night and that led to a fair amount of dumping of index bonds in the morning, which turned entirely around in the afternoon when headlines hit about some sort of deal in the works. The new supply in the pipeline is loosening up the market a bit. Sukuks have rallied hard enough that I saw a fair amount of secondary supply today albeit at levels ridiculously tight to KSA. If this deal comes to fruition and we see an eye watering rates rally on the back of it your guess is as good as mine to where spreads will end up. I would really like to stop talking about a deal though.

MIDDLE EAST - MACRO / MARKETS

Morocco returns to Eurobond markets after regaining investment-grade status. Morocco successfully raised EUR2.25bn through a dual-tranche Eurobond issuance in May 2026, attracting more than EUR5bn in investor demand and achieving tighter pricing than initially guided, highlighting strong confidence in the country’s macroeconomic outlook and sovereign credit profile. The transaction, split between 8-year and 12-year maturities, marks Morocco’s second consecutive euro-denominated issuance and reflects the government’s growing preference for euro funding as it finances large-scale infrastructure projects tied to the 2030 FIFA World Cup, post-earthquake reconstruction, and broader capital-market reforms. The deal was completed without a formal international roadshow, yet demand remained robust due to Morocco’s relatively stable fiscal position, manageable external debt levels, and solid foreign exchange reserves. With economic growth projected to remain among the strongest in North Africa and sovereign spreads tightening relative to regional peers, Morocco is increasingly positioning itself as one of the more resilient EM credit stories in the MENAT region, with further external issuance likely through 2026.

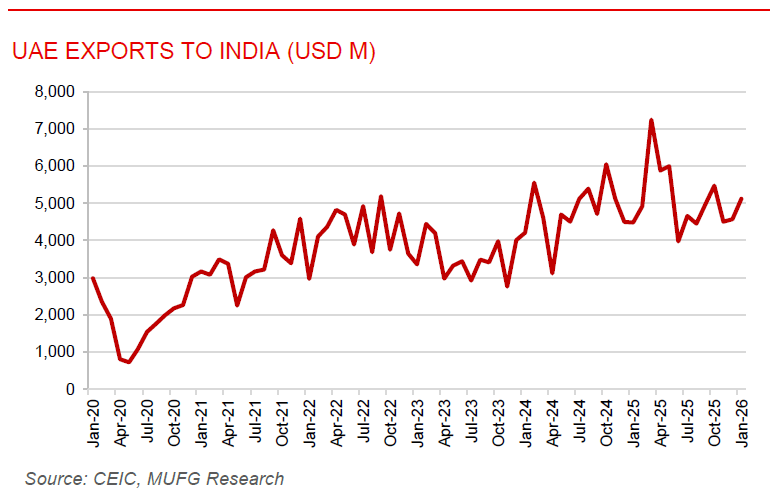

UAE-India CEPA deepens strategic trade partnership beyond USD100bn. The UAE–India Comprehensive Economic Partnership Agreement (CEPA) marked its fourth anniversary with bilateral trade reaching over USD101bn in FY2025–26, surpassing the USD100bn mark for the second consecutive year and reinforcing the agreement’s role as a central pillar of the bilateral economic relationship. Since entering into force in May 2022, CEPA has driven a notable expansion in non-oil trade, which now accounts for roughly two-thirds of total flows, supported by tariff liberalisation and deeper investment cooperation. Recent high-level engagements between UAE and Indian leaders have further strengthened ties, resulting in agreements across energy, defence, infrastructure and technology, alongside approximately USD5bn in new UAE investment commitments into India. Overall, the continued growth in UAE–India trade underscores the deepening strategic and economic partnership between the two countries.