To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil eases on renewed Iran US talks despite ongoing disruption. Oil prices declined, with Brent falling about 1% to around USD94/b, as signs that Iran will participate in renewed negotiations with the US in Islamabad raised hopes for a diplomatic breakthrough before the ceasefire expires. Donald Trump indicated talks could resume soon, while Iran’s willingness to attend marked a shift from earlier hesitation, supporting market sentiment. However, uncertainty remains high as tensions persist around the Strait of Hormuz, where shipping flows are still largely halted following recent military incidents and mutual restrictions. The conflict continues to drive volatility in energy markets, with unresolved issues including Iran’s nuclear program and regional conflicts, while global leaders urge de-escalation. Despite the recent dip, risks remain skewed to the upside, with forecasts suggesting oil could surge significantly if disruptions persist and volatility potentially lasting for years.

Gold steady as markets assesses peace talks ad rate outlook. Gold held near USD4,830/oz as investors weighed prospects for renewed US-Iran negotiations against persistent inflation risks driven by the ongoing conflict. Plans for fresh talks in Pakistan, featuring delegations from both sides offered some optimism ahead of a looming ceasefire deadline flagged by President Trump. However, the war continues to disrupt global energy supplies, reinforcing inflationary pressures and expectations that central banks will keep interest rates elevated, a negative for non-yielding gold. With bullion down about 8% since the conflict began, investor focus is also turning to US monetary policy, particularly the outlook from Federal Reserve leadership, as signals on future rate cuts or tightening could drive the next move in gold prices.

MIDDLE EAST - CREDIT TRADING

End of day comment – 20 April 2026. You would think GCC bonds would sort of also give half the Friday gains back, but they stayed on Friday’s level and in many cases closed even higher. That is even more impressive given the weaker macro risk in general. IG names were broadly unchanged, QATAR saw activity in 10y bucket with 34s starting strong and on the back of it 35s conv and sukuk started to trade, but into the close we are broadly settling unchanged in cash price in all 3 bonds/-2bp. ADGB long end against this has still bonds to work through, 54s were most active closing -0.125pt/+0bp. In higher beta credits SHARSK saw a very strong bid, and there was not much offer side liquidity causing bids to step up, especially in 36s closing +0.25pt/-5bp. Long end bonds though remain firmly bid showing the +ve risk appetite for OMAN, 47s closed +0.375pt/-3bp. Away from sovgn, most quasis and corps were unmoved in cash price and with the UST move closed -2/3bp in spread terms.

MIDDLE EAST - MACRO / MARKETS

Kuwait declares force majeure as war disrupts oil output. Kuwait Petroleum Corp. has declared an additional force majeure on crude and refined product shipments, indicating it will be unable to fully meet contractual obligations even after the Strait of Hormuz reopens. The decision reflects significant war-related damage to oil infrastructure, which has pushed Kuwait’s production down to levels last seen in the early 1990s following the Iraqi invasion. The ongoing conflict has effectively halted traffic through Hormuz, leading to rising storage constraints and forcing producers across the region to cut output, contributing to a major global supply shock. While Kuwaiti officials expect production to gradually return to pre-war levels within a few months after hostilities ease, the latest move highlights that recovery will be slow and operational challenges will persist. The situation underscores the broader vulnerability of Gulf energy exporters to geopolitical disruptions, as prolonged outages and logistical bottlenecks continue to weigh on supply, revenues, and market stability.

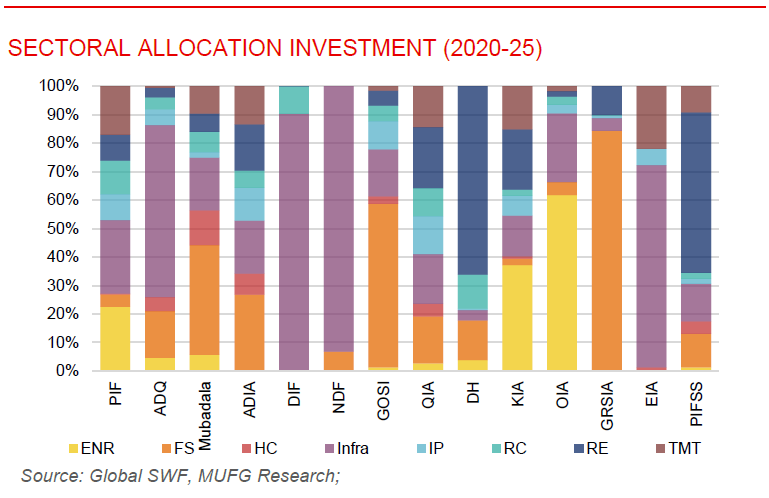

PIF sets 2030 strategy to deepen Saudi economic transformation. Public Investment Fund has unveiled its 2026–2030 strategy, marking a transition from rapid expansion to a more mature phase focused on sustainable value creation, improved investment efficiency, and stronger private sector participation to support Saudi Arabia’s long-term economic transformation. Chaired by Mohammed bin Salman, the strategy structures investments into three portfolios. The Vision Portfolio, which will drive the development of six key domestic ecosystems, including tourism, urban development, advanced manufacturing, logistics, clean energy, and NEOM, while fostering deeper integration across sectors and attracting private and international partners; the Strategic Portfolio, aimed at scaling national champions and maximizing financial and economic impact; and the Financial Portfolio, focused on global diversification and sustainable returns. The plan builds on PIF’s rapid growth, with assets exceeding USD900bn and significant contributions to non-oil GDP and private sector development and reinforces its role as a central engine of diversification, innovation, and long-term wealth creation for the Saudi economy.