To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds near highs as Trump revives threat of strikes on Iran. Oil prices steadied as markets assessed renewed threats from President Donald Trump to resume military action against Iran if Tehran refuses US peace terms. Brent crude traded around USD111/b while WTI hovered near USD104/b, with traders remaining cautious after Trump again warned of potential strikes despite previously delaying planned attacks. The ongoing conflict, now in its 12th week, continues to disrupt flows through the Strait of Hormuz, keeping global energy markets tight and inflation concerns elevated. Additional pressure came from reports that the US seized another Iran-linked tanker and that NATO is discussing possible naval escorts for commercial shipping if the strait remains closed into July. Meanwhile, falling US, crude inventories and ongoing geopolitical uncertainty continue to support prices, although rising global bond yields and concerns over weaker economic growth are limiting further upside momentum.

Gold extends losses as inflation fears, and rate-hike expectation rise. Gold remained under pressure as ongoing disruptions in the Strait of Hormuz continued to fuel inflation concerns and strengthen expectations that global central banks may keep interest rates higher for longer. Gold traded near USD4,480/oz while surging energy prices linked to the Iran war triggered a broad selloff in global bond markets and pushed US 30-year Treasury yields to levels last seen during the 2007 financial crisis period. President Trump renewed threats of military action against Iran despite earlier postponing planned strikes, adding to geopolitical uncertainty. Elevated inflation risks from higher oil prices are increasingly reducing expectations for near-term monetary easing, which is negative for non-yielding gold. Gold has now fallen around 15% since the conflict began, while silver also faced heavy losses amid rising inflation concerns.

MIDDLE EAST - CREDIT TRADING

End of day comment – 19 May 2026. Another day driven by the rates move. The morning was strong, seen first yield buyers in some quasis (ADNOUH 47s), fins (EBIUH) and even in long bonds (ADGB 54s) as the recent yield uptick brought some buyers out. It helped that G3 rates were relatively stable. That changed in the afternoon though where the market faced another headline driven rates sell off on fading hopes of any timely Hormuz opening. All said Spreads closed anywhere from unch to -3bp as most lose bonds cleared in the morning. In IG QATAR continues to outperform ADGB. The latter seems to have done another private placement in 10y (1bn). Talking of new supply, MOROC is tapping the market with a 2 tranche EUR deal, 1.25bn 8y at MS+170bp and 1bn 12y at MS+200bp which offers roughly 10bp concession against outstanding 35s preannouncement. With some higher beta deals like DARALA, ALINMA AT1 or OMAB AT1 waiting to be priced the primary market remains active. All eyes though remain on the rates side and UST/JGB moves overnight.

MIDDLE EAST - MACRO / MARKETS

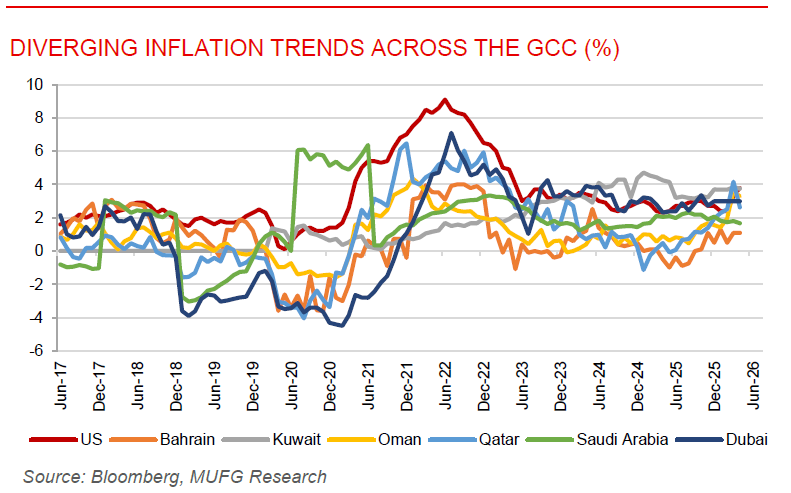

Diverging inflation trends across the GCC highlight uneven impact of the war. April 2026 inflation data from Qatar and Kuwait both came in at 2.6% y/y, but the underlying trends reflected very different economic dynamics across the Gulf. Qatar’s inflation slowed sharply from 4.2% in March, likely supported by easing housing and food pressures alongside softer services inflation, reinforcing the resilience provided by the Qatar Central Bank’s strong reserve position and ample external buffers. In contrast, Kuwait’s inflation accelerated from 2.1%, signalling that war-related supply and import costs are increasingly feeding into consumer prices, particularly given Kuwait’s greater exposure to disruptions in the Strait of Hormuz and lack of alternative export infrastructure. The pickup in inflation alongside weaker PMI readings also points to emerging mild stagflationary pressures in Kuwait. More broadly, GCC inflation remains relatively contained compared to regional peers such as Turkey and Egypt, supported by dollar pegs, strong reserves, and relatively stable domestic demand conditions. Looking ahead, upcoming inflation prints will be closely watched to assess whether Qatar’s disinflation trend continues and whether Kuwait’s price pressures deepen further as regional tensions persist.

Oman’s Q1 revenues rise on strong oil and gas income. Oman’s public revenues increased 13% y/y in Q1 2026 to USD7.8bn, mainly supported by stronger oil and gas revenues. Net oil income rose 5% to OMR1.54bn, while gas revenues surged 36% to OMR593 million, with Oman’s crude averaging around USD64/b and production reaching roughly 1.025mb/d. Current revenues also climbed 13% to OMR817 million. On the expenditure side, public spending rose 9% to OMR3.01bn, driven by higher current and development spending, with ministries and government units utilizing around 26% of the year’s development budget allocation. Subsidies for social protection, electricity, and fuel products remained significant, while the government also transferred OMR75 million toward debt repayment provisions. Despite higher spending, Oman’s debt profile remained stable, with public debt standing at OMR14.5bn at the end of Q1, reflecting continued fiscal discipline and manageable financing conditions.