To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Hormuz reopening drives oil lower as supply return. Oil prices are on track for a sharp weekly decline as the US-Iran interim peace agreement accelerates the reopening of the Strait of Hormuz. Brent fell around 9% during the week to near USD79/b, while WTI traded around USD75/b, as stranded cargoes began leaving the Gulf and major producers, including Kuwait, prepared to restore output. Tanker traffic through Hormuz has started to recover, supported by the removal of US restrictions on Iranian port access and coordinated efforts to improve maritime safety. Although oil has surrendered most of the war-related risk premium, a full normalisation of flows is likely to take time as producers restart fields, repair infrastructure, clear mines, and rebuild shipping confidence. Nevertheless, the market is increasingly pricing in a gradual return of Middle Eastern supply, reinforcing expectations of a more balanced oil market in the second half of 2026.

Gold pressured by hawkish Fed despite US-Iran peace deal. Gold fell below USD4,200/oz, as expectations of tighter US monetary policy outweighed support from the US-Iran interim peace agreement. The Fed’s hawkish tone reinforced market expectations for a rate hike later this year, reducing the appeal of non-yielding assets such as gold. While the reopening of the Strait of Hormuz and the return of commercial shipping have eased concerns over a prolonged energy supply shock, inflation risks have not fully disappeared as it may take time for oil and LNG flows to normalise. In our view, gold is likely to remain under pressure in the near term as geopolitical risk premiums continue to fade and higher for longer interest rate expectations strengthen. However, lingering uncertainty around the pace of Hormuz normalisation and the durability of the US-Iran agreement should help limit downside risks.

MIDDLE EAST - CREDIT TRADING

End of day comment – 18 June 2026. Not much bounce back from the widening yesterday but the tone was definitely better. Volumes ticked up nicely with the rates move triggering a fair amount of short-dated bond trading along with a fair amount of long end ARAMCO and PIFKSA and KSA project finance bonds going through. Spreads were generally tighter across those shorter dated bonds given the largely local holder base that tends to be more focused on yield rather than spreads. Bonds were 3-4bps tighter out to about 2032s, flat out to the 2051s and 3-4bps tighter longer than 2051. This didn't translate into ARAMCO or PIFKSA long end where it feels pretty heavy and that the street is gnawing on itself a bit trying to square positions. We did see some legit supply in mid curve KSA sovs for the first time in a while as 35 sukuks and conventional come out in a number of BWICs. The new JAZCOR 6.5% Perp traded about as expected with locals slowly driving it higher into 100.20-100.25 territory but limited flipping from retail accounts allowed it. (Source: Matthew Dunker, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

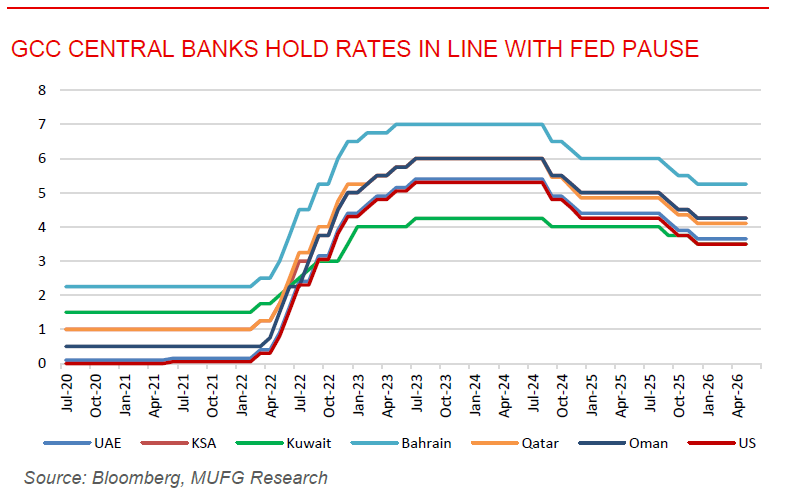

GCC central banks hold rates in line with Fed pause. Following the US Federal Reserve’s decision to keep rates unchanged at 3.50%–3.75% on 17 June 2026, GCC central banks largely followed by maintaining their benchmark rates, reflecting the region’s close monetary-policy linkage to the US dollar. The UAE kept its Base Rate unchanged at 3.65%, while Saudi Arabia maintained its repo and reverse repo rates at 4.25% and 3.75%, respectively. Qatar, Bahrain, Oman and Kuwait also kept policy rates steady, consistent with their dollar-peg or dollar-linked exchange-rate frameworks. The decision was broadly expected, as GCC central banks typically move in line with the Fed to preserve currency stability and limit capital-flow pressures. However, the rate hold also means borrowing costs will remain elevated for longer across the region, delaying relief for households and corporates while continuing to support bank margins in the near term.

IMF unlocks additional funding as Jordan demonstrates economic resilience. The IMF approved the fifth review of Jordan’s Extended Fund Facility (EFF) and the second review of its Resilience and Sustainability Facility (RSF), unlocking USD188 million in additional financing. The Fund praised Jordan’s ability to maintain macroeconomic stability despite ongoing regional tensions, supported by prudent fiscal and monetary policies, strong reform implementation, and targeted measures to protect vulnerable households and key sectors such as tourism and industry. Jordan’s economy grew by 2.8% in 2025, up from 2.6% in 2024, while inflation remained moderate at 1.8%. The IMF expects growth to remain resilient at 2.7% in 2026 and accelerate to 3.1% in 2027. Fiscal performance continued to outperform programme targets, foreign reserves remained robust at around USD$27bn, and confidence in the dinar peg was reinforced by strong financial inflows. The latest approval highlights continued confidence in Jordan’s reform agenda, with progress in improving the business environment, labour market flexibility, and competitiveness expected to support stronger private sector-led growth and job creation over the medium term.