To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil extends decline on Hormuz reopening expectations. Oil prices fell with Brent dropping below USD79/b and WTI nearing USD76/b, as markets increasingly priced in a US-Iran agreement that could restore oil flows through the Strait of Hormuz. The proposed deal would allow Iran to resume oil exports and facilitate the reopening of the key shipping route, raising expectations of a significant increase in global crude supply. Reflecting the easing supply concerns, physical market tightness has moderated sharply, with Brent’s prompt spread narrowing from nearly USD10/b in early April to just USD0.2/b. While uncertainty remains over the implementation and durability of the agreement, the prospect of additional Iranian exports and improved Gulf shipping access has weighed heavily on prices. Nevertheless, global inventories remain relatively tight, with US crude stockpiles continuing to decline. We expect Brent to remain in the USD80-90/b range in the near term as improving supply prospects offset still-tight inventories and lingering geopolitical risks.

Gold holds gain ahead of US-Iran peace deal. Gold remained near USD4,335/oz, as markets awaited the signing of a US-Iran interim peace agreement that could help ease the energy and inflation shock caused by the conflict. The proposed deal would allow Iran to resume oil exports and eventually regain access to frozen assets, while a reopening of the Strait of Hormuz could improve global energy supplies and reduce inflationary pressures. Although lower energy prices and easing inflation expectations would typically weigh on non-yielding assets such as gold, the precious metal continued to find support from lingering geopolitical uncertainty and cautious investor sentiment. At today’s Fed meeting, rates are expected to remain unchanged, with markets looking for guidance on the future inflation and interest rate outlook.

MIDDLE EAST - CREDIT TRADING

End of day comment – 16 June 2026. Activity was lower than yday and dealer trades had a higher ratio to total volumes suggesting the position squaring ahead of the FED tomorrow has started. All UAE index phase out bonds felt heavy today. Long end ADGB was -0.375pt/+6bp with most UAE names +2/+5bp. MUBAUH has continuous selling in long end and belly bonds where 33s closed -0.25pt/+6bp. The outperformer was ADQABU which got bid up in 31s/34s and 35s (+0.25pt/+0bp), so technicals are playing out a bit. But away from UAE we also saw weakness in the QATAR complex, ever squeezed QPETRO 31s had sellers closing -0.275pt/+9bp. The sovgn curve was anywhere from +1bp to +5bp. Higher betas like OMAN and SHJGOV were also +3/6bp. SHJGOV long end 50s and 51s found sellers after yday squeeze and closed -0.25pt/+6bp. The market will turn its attention to the FED now and the implications on rates market, meanwhile the flattening in UST continues. Today the market has pushed back against the spread tightening of Friday and yday, which arguably looked a bit excessive. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

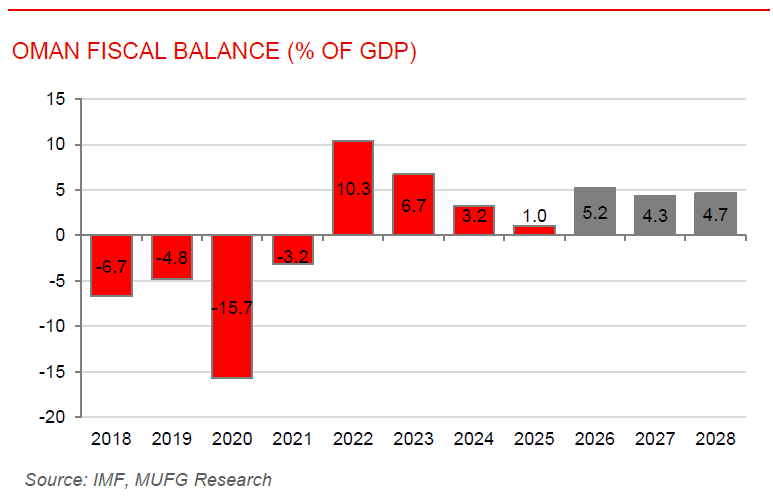

Oman shows resilience as higher oil revenue strengthens outlook. The IMF noted that Oman’s economy has remained resilient despite the regional conflict, supported by the strategic location of its major ports outside the Strait of Hormuz and continued prudent economic management. Real GDP growth is projected to accelerate to 3.7% in 2026 from 2.4% in 2025, driven by higher oil production and exports, while non-hydrocarbon growth is expected to moderate temporarily due to weaker tourism and construction activity before recovering in 2027. Rising oil prices and fiscal discipline are expected to strengthen public finances, with the fiscal surplus widening to 4.5% of GDP in 2026 and government debt continuing its downward trend. The external position is also forecast to improve, with the current account returning to a surplus of ~3% of GDP. Inflation has risen to 2.8% amid higher food and transport costs but remains relatively contained, while the banking sector continues to benefit from strong capital, liquidity, and asset quality. The IMF emphasised that maintaining fiscal and structural reform momentum under Oman Vision 2040 will be critical to supporting long-term growth, diversification, and fiscal sustainability, although risks remain tilted to the downside due to regional geopolitical uncertainty.

Israel’s economic contraction deepens in Q1 2026. Israel’s economy contracted by 3.8% annualised in Q1 2026, a deeper decline than the initial 3.3% contraction, highlighting the deeper than expected impact of the regional conflict on economic activity. The revised data sowed weaker private consumption, softer business activity, and a significant downgrade to export growth, suggesting that even Israel’s traditionally resilient technology and services sectors faced greater disruption than previously anticipated. In contrast, fixed investment remained strong, supported by continued technology and energy sector spending. Although GDP was still 1.5% higher y/y, the data suggest a slower recovery trajectory, with growth prospects dependent on improving domestic demand, export performance, and geopolitical stability.