To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

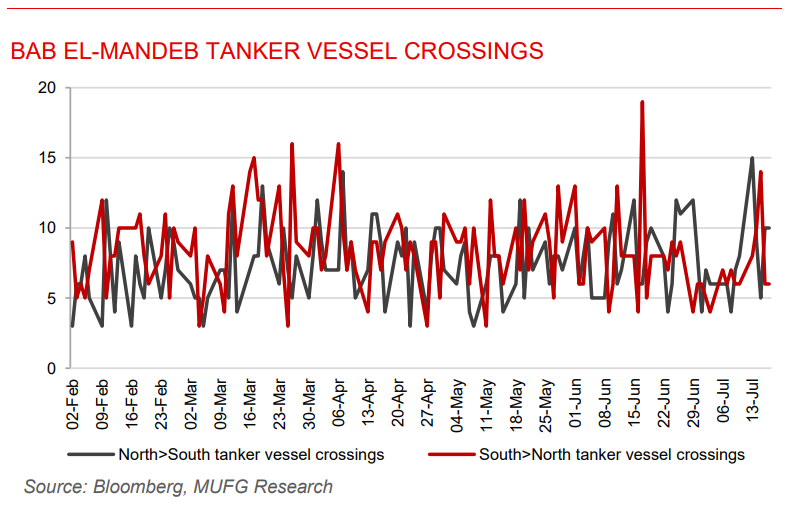

Oil posts strongest weekly gain since April on escalating US-Iran conflict. Oil prices were on track for their strongest weekly gain since April, with Brent rising above USD85/b and WTI nearing USD80/b, as escalating military exchanges between the US and Iran intensified concerns over Middle East energy supplies. Fresh US strikes on Iranian military targets, alongside attacks on vessels near Iran’s main export terminal and missile threats extending to Qatar and the Bab el-Mandeb shipping route, heightened fears of broader regional disruption. Although some tanker traffic through the Strait of Hormuz continues, shipments remain constrained, while tighter fuel markets in the US and Europe have pushed refining margins to record highs. The conflict is increasingly affecting both crude and refined fuel markets, suggesting that the persistence and geographic spread of supply disruptions will be the key drive of oil prices in the near term.

Gold slides on higher rate expectation. Gold prices were on track for their largest weekly decline since early June, despite edging higher toward USD3,980/oz today, as escalating US-Iran hostilities reinforced concerns that rising energy prices could keep inflation elevated and prompt the Fed to tighten monetary policy further. The latest US strikes on Iran added to geopolitical tensions, but the resulting surge in oil prices also lifted US Treasury yields and the US dollar, reducing the appeal of non-yielding gold. Gold has remained close to the USD4,000/oz level in recent weeks after suffering its steepest quarterly decline sine 2013. The recent price action suggests that markets are placing greater weight on the prospect of higher for longer US interest rates than on gold’s traditional safe-haven demand, leaving gold vulnerable unless geopolitical risks translate into a broader deterioration in financial market sentiment.

MIDDLE EAST - CREDIT TRADING

End of day comment – 15 July 2026. We were more tied to rates today than the days rates have rallied this week. Spreads in IG product are generally flat and cash prices have moved more or less in line with the weakness in the rates market. Client activity was, once again, fairly muted and focused more of rebalancing and retail sized prints. We had marginal demand from local accounts across some T2 bonds. KSA Sovereign spreads are unchanged and there is no bond with a TRAX volume >10mm. The new SRCSUK 36s seem to have found a floor around z+138 or so with some loose bonds getting cleaned up in the street at that level. Bank bonds were stuck on cash price as we were lifted out of BSFR 35s and RJHIAB 6.15 36s. PIFKSA 56s and ARAMCO long end were offered through CBBT mid most of the day as there appears to be an overhang of duration in those names, while the sukuks and the shorter end is in good demand. (Source: Matthew Dunker, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

Iraq advances oil expansion and export diversification. Iraq is stepping up efforts to expand oil production and reduce its reliance on the Strait of Hormuz, with Chevron expected to sign preliminary agreements to advance negotiations on developing the West Qurna-2 and Nasiriyah oil fields while participating in a consortium studying alternative export pipelines to the Mediterranean. The move follows the US-Iran conflict, which forced Iraq, previously OPEC’s second-largest oil producer, to cut production by more than 60% as exports through Hormuz were severely disrupted, exposing the country’s dependence on the strategic waterway and straining public finances. At the same time, Iraq is seeking to attract greater foreign investment to unlock its production potential and has recently argued that its OPEC+ production quota is too restrictive, with officials even raising the possibility of exiting the group if higher output is not allowed. While the agreements remain non-binding and commercial negotiations are still at an early stage, they reflect Iraq’s broader strategy to rebuild production capacity, diversify export routes and enhance long-term energy security against future geopolitical disruptions.

UAE accelerates strategic investment to support non-oil growth. The UAE government significantly increased capital spending in Q1 2026, with investment in non-financial assets rising to AED18.6bn (USD5.1bn) from AED 2.0bn (USD0.5bn) a year earlier, driven by infrastructure, digital transformation, renewable energy and advanced industrial projects. The sharp increase in fixed asset investment shifted the federal government’s fiscal position from a net lending surplus of AED13.1bn in Q1 2025 to net borrowing of AED10.4bn, which the Ministry of Finance said reflected a deliberate acceleration of strategic capital deployment rather than weaker revenues. At the same time, net acquisitions of financial assets declined as the government redirected liquidity toward domestic productive investment. The expansionary fiscal stance highlights the UAE’s continued commitment to diversifying its economy and strengthening long-term non-oil growth, with higher public investment expected to support activity across construction, logistics, manufacturing and digital infrastructure.