To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil slips as ceasefire optimism eases market tensions. Oil prices declined, with Brent falling toward USD98/b and WTI near USD93/b, as President Trump struck an optimistic tone on prospects for a lasting US-Iran ceasefire, easing immediate supply concerns. Despite his claims that Iran may agree to concessions such as reopening the Strait of Hormuz, uncertainty remains as Iran has not confirmed any deal and negotiations are expected to take months. The conflict, now nearing 50 days, has severely disrupted global oil flows, with dual blockades by the US and Iran keeping the critical waterway largely closed and contributing to earlier price volatility. While market swings have recently moderated and a temporary ceasefire between Israel and Lebanon has slightly eased regional tensions, risks remain elevated given ongoing geopolitical uncertainty and mixed signals from policymakers.

Gold set for weekly gain on ceasefire optimism. Gold prices hovered near USD4,795/oz, heading for a fourth consecutive weekly gain as optimism over a potential US-Iran ceasefire supported sentiment despite lingering geopolitical risks. President Trump signalled that Iran may agree to key terms, including reopening the Strait of Hormuz, though a final deal could take months and tensions remain elevated with ongoing blockades and shipping restrictions. Softer oil prices have eased inflation concerns, providing some support to gold, even as expectations of prolonged higher interest rates continue to weigh on non-yielding assets. While gold has recovered part of its earlier losses, it remains about 9% lower since the conflict began, with persistent risks from disputed energy supplies and damaged infrastructure likely to keep inflation uncertainty elevated.

MIDDLE EAST - CREDIT TRADING

End of day comment – 16 April 2026. Nervy close. It was overall a quiet day. The morning was still somewhat constructive, but whilst bids remained strong no one was chasing bonds. During the day we got a few risk off Iran headlines leading to an oil price spike and weakness in G3 bonds. That weighed not only on prices but also turned flows around as we see RM and ETFs selling into the close. To be sure it’s not panicky either and spreads are still finishing broadly unch/+1bp. One credit away from GCC widening a bit more substantial today was MOROC/ OCPMR. Whilst the new hybrids in OCPMR held both about 0.25/0.375pt above reoffer there was selling pressure in both senior curves. It feels a bit that accounts might have been overallocated in hybrids and decided to sell seniors against it. Into the close we get the Trump announcement on an Israel/ Lebanon ceasefire but so far it doesn't seem to impact risk markets. Things remain fluid indeed and ahead of the weekend we would expect a muted session tomorrow. The market feels weaker than spread moves suggest.

MIDDLE EAST - MACRO / MARKETS

Abu Dhabi fund backs major Jordan rail project. A newly established wealth fund has signed a USD2.3bn agreement to develop a major railway project in Jordan, highlighting its expanding role in advancing Abu Dhabi’s strategic investments and regional partnerships. L’imad Holding Co. will collaborate with Jordanian entities to build and operate a 360-kilometer rail line linking phosphate and potash mines to the port of Aqaba, with construction expected to begin in 2027 and take five years to complete. The project, one of the largest infrastructure investments in Jordan in decades, is expected to boost employment, lower transport costs, and enhance the country’s competitiveness in key export sectors. It also reflects Abu Dhabi’s continued willingness to deploy capital despite ongoing regional tensions, using sovereign investment as a tool to strengthen geopolitical ties, support economic development in allied nations, and reinforce Jordan’s role as a stabilising force in a volatile region.

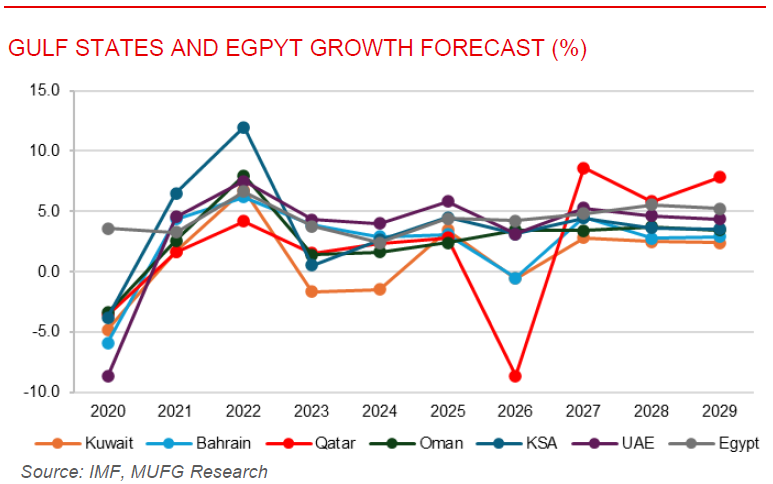

Middle East shows resilience despite war-driven economic shock. The IMF highlights that while the Middle East economy has been significantly disrupted by the ongoing conflict, the region also demonstrates notable resilience supported by strong pre-war fundamentals and financial buffers. Prior to the war, many economies were experiencing solid growth, easing inflation, and robust non-oil activity, providing a cushion against the current shock. Although the near closure of the Strait of Hormuz and damage to energy infrastructure have sharply reduced production, disrupted trade, and pushed regional growth down to 1.4% in 2026, some oil exporters continue to benefit from elevated energy prices, supporting fiscal and external balances where production remains intact. In addition, strong sovereign wealth and policy reforms enhance the region’s ability to absorb shocks and maintain stability. However, these positives are offset by rising inflation, weaker tourism, and mounting fiscal and external pressures, particularly for more exposed economies. While a recovery is expected if disruption eases by mid-2026, the outlook remains uncertain, with resilience likely to determine how effectively countries navigate prolonged geopolitical risks.