To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

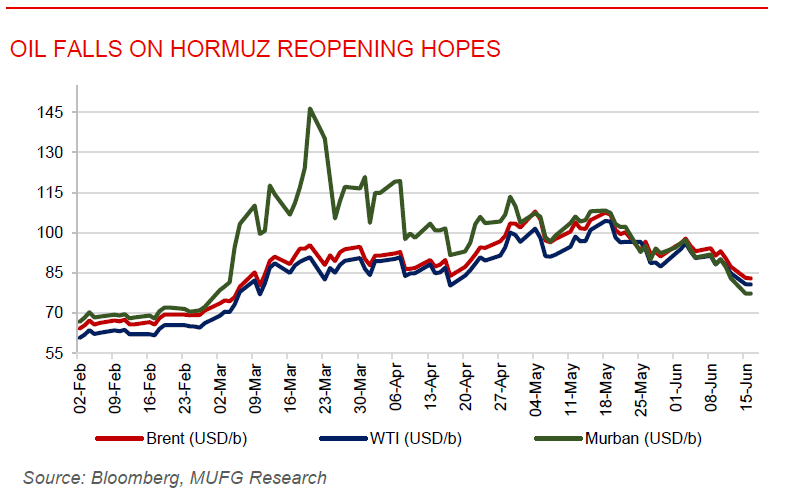

Oil falls as Hormuz reopening prospects weigh on market sentiment. Oil prices fell with Brent dropping below USD83/b and WTI nearing USD81/b, as markets increasingly priced in the prospect of a US-Iran agreement that could restore energy flows through the Strait of Hormuz. Optimism surrounding a gradual recovery in Gulf exports has reduced the geopolitical risk premium built up during the conflict. Physical crude markets also weakened, with the Dubai and Murban forward curves shifting into contango for the first time since the war began, signalling easing concerns over immediate supply shortages. Expectations of higher exports were reinforced by ADNOC’s latest crude sales tenders and the prospect of additional barrels entering the market from floating storage inside the Persian Gulf. While uncertainty remains over the timing and practical implementation of the agreement, oil flows through Hormuz had already begun recovering before the deal announcement. We expect Brent to remain in the USD80–90/b range in the near term as improving supply prospects offset still-tight inventories and lingering geopolitical risks.

Gold gains as US-Iran deal raises hopes for Hormuz reopening. Gold held onto recent gains near USD4,315/oz after the US and Iran announced an interim agreement aimed at ending the conflict and lifting maritime blockades in the Strait of Hormuz. The prospect of improved energy flows and lower oil prices has helped ease inflation concerns, although uncertainty remains over how quickly shipping and commodity exports can normalize. Gold remains significantly below its pre-war levels, reflecting reduced safe-haven demand and expectations that major central banks may keep interest rates elevated. Investors are now focused on upcoming policy meetings, particularly the Fed, for further guidance on the monetary policy outlook.

MIDDLE EAST - CREDIT TRADING

End of day comment – 15 June 2026. Strong day but off the highs. The market gapped higher with the overnight news of an agreement between US/ Iran to be signed on Friday. Again, like we saw Friday the risk on trade was seen mainly in long end bonds and higher beta credits. In the afternoon though the move faded as RM took advantage of tighter levels to sell mainly UAE index phase out names. On the other side ETFs were sizeable buyers throughout the day and the street still tried to get risk on board by bidding up bonds. At eod ADGB outperforms QATAR in IG, long end bonds leading, 54s +1pt/-7bp vs 34s +0.375pt/-3bp, QATAR is more like 2-5bp tighter. In higher betas SHJGOV was the outperformer and here as well long end leading, 50s closed +1.25pt/-13bp. Started also to see corporate bonds getting active and turning risk on, DPWDU had late profit taking but still closed +0.875pt/-6bp in 48s/49s. ALDAR hybrids also started clearing and finding more interest than lately, 55s/56s close +0.75pt/-12bp. With the performance of Friday and today primary markets should be wide open. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

Moody’s affirms UAE, Abu Dhabi, and Sharjah ratings amid regional conflict. Moody’s affirmed the UAE’s and Abu Dhabi’s Aa2 ratings and Sharjah’s Ba1 rating, all with stable outlooks, underscoring the country’s strong credit fundamentals despite the ongoing Middle East conflict. The UAE’s rating is supported by high per-capita income, a diversified economy, strong institutions, very low federal debt, and expected backing from Abu Dhabi if needed. Abu Dhabi’s rating remains anchored by exceptionally large financial assets exceeding 300% of GDP, low debt, and its ability to reroute part of its oil exports, although Moody’s expects the wider UAE economy to contract in 2026 before rebounding in 2027 as trade flows normalise. Sharjah’s rating reflects its diversified economy and improving fiscal position, supported by stronger real estate-related revenues and future corporate tax inflows, though its narrower revenue base, higher debt burden, and exposure to trade, logistics, tourism, and real estate remain constraints. Overall, Moody’s expects the UAE’s strong fiscal buffers, federal institutions, and Abu Dhabi’s balance sheet strength to absorb the shock, while prolonged geopolitical risks remain the key downside risk to growth and diversification.

Saudi inflation remains contained despite regional pressures. Saudi Arabia’s inflation rate rose modestly to 1.8% y/y in May 2026, from 1.7% y/y in April, remaining among the lowest globally despite regional geopolitical tensions. The increase was mainly driven by higher housing and utility costs, alongside moderate rises in transportation and hospitality prices. However, inflation remains firmly anchored within the 1.7–2.0% range seen over the past 18 months, supported by ongoing housing supply expansion and broader Vision 2030 reforms. The subdued inflation environment preserves SAMA’s policy flexibility, allowing it to broadly track future Fed policy moves without significant domestic inflation constraints. Compared with regional peers such as Turkey and Egypt, Saudi Arabia continues to maintain a highly stable price environment, reinforcing the Kingdom’s strong macroeconomic fundamentals.