To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds steady as ceasefire extension hopes emerge. Oil prices stabilised, with Brent below USD95/b and WTI near USD91/b, as signs of a potential ceasefire extension between the US and Iran supported cautious optimism for renewed negotiations. Discussions to prolong the truce aim to create space for a broader peace agreement, even as tensions remain high around the Strait of Hormuz, where US blockades and Iranian restrictions have largely halted shipping. The conflict, now in its seventh week, continues to disrupt global energy markets, tightening supply, fuelling inflation, and weighing on economic growth, while US inventory declines and strong export demand, particularly from Asia, offer some support to prices. Despite tentative diplomatic progress, significant obstacles remain, including disputes over reopening key shipping routes and Iran’s nuclear program, leaving the market highly sensitive to further geopolitical developments.

Gold rises on diplomatic hopes despite ongoing tensions. Gold prices climbed, rising up to 1% to around USD4,838/oz as renewed optimism over a potential US-Iran diplomatic resolution eased inflation concerns, even as tensions persist around the Strait of Hormuz. Reports of a possible ceasefire extension and continued negotiations, supported by signals from President Trump, boosted market sentiment, while softer oil prices and a weaker US dollar further supported gold. Although expectations of prolonged higher interest rates continue to weigh on gold, improving investor demand, evidenced by inflows into gold-backed ETFs, has helped prices recover some recent losses. Still, gold remains down about 8% since the conflict began, reflecting earlier liquidity pressures and the broader impact of tighter monetary conditions.

MIDDLE EAST - CREDIT TRADING

End of day comment – 15 April 2026. The spread tightening continues. Morning bids were strong carrying over from yesterday. Especially long end bonds were bought on the back of the risk on mood and lower overnight UST yields. The first wobble came with the Wapo report that the US is sending more troops to the region. Also, UST started falling and flows became more two ways. However, the cash bid broadly held and spreads tightened with the UST move. Still sellers outstripped buyers at EOD with some late ETF outflows. ADGB closed -3bp. Activity was mainly in 34s (+0.20pt/-3bp) and long end, 54s +0.5pt/-3bp. In the afternoon the curve saw more UAE index names getting sold by ETFs on the back of the EMBI phase out. QATAR outperformed again, very little selling in 10y+ bonds, I close 50s +0.625pt/-5bp. OMAN closed -5bp but here as well we saw a bit of selling and profit taking from RM/ETF in the afternoon. 31s was active closing +0.25pt/-5bp, 48s +0.625pt/-bp. Fin bonds saw most interest to buy Sukuks, but offer-side liquidity is hard to find. The AT1 bid is still strong but prices were broadly unchanged. The main quasi sovgn curves closed in line with the sovgn -5bp with some late activity in ADQABU and MUBAUH.

MIDDLE EAST - MACRO / MARKETS

Israel inflation eases but rate cuts remain unlikely. Israel’s inflation slowed to 1.9% y/y in March from 2.0% y/y in February, falling below expectations and remaining within the Bank of Israel (BoI)’s ±2% target range, but the decline is unlikely to prompt near-term interest rate cuts. Despite softer price pressures, rising global energy costs following the conflict with Iran and disruptions around the Strait of Hormuz continues to pose inflationary risks. As a result, the BoI has kept its policy rate steady at 4%, with Governor Amir Yaron signalling that any easing will depend on future inflation trends. Meanwhile, a strong shekel, now at multi-decade highs, has added pressure on exporters, prompting calls for rate cuts, though policymakers remain cautious given ongoing geopolitical and energy-related uncertainties.

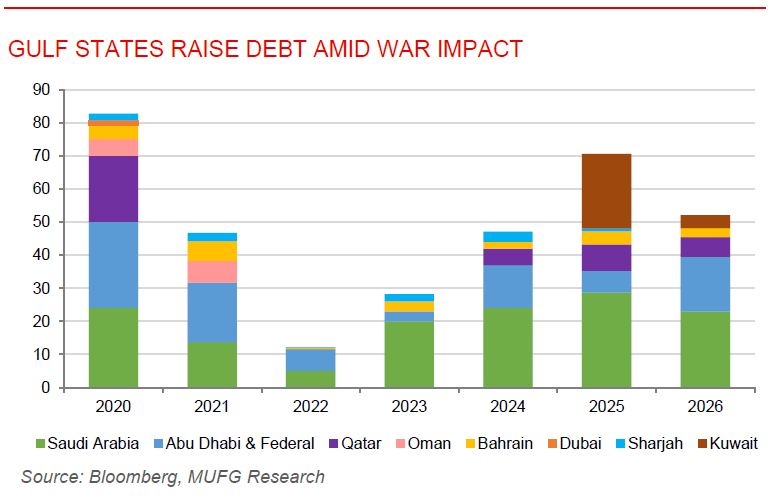

Gulf states tap private debt market as war strains revenues. Gulf monarchies have raised nearly USD10bn through private bond placements in April, marking their first international borrowing since the Iran war disrupted regional economies and energy flows. The shift toward private markets allows governments to secure funding more quickly and with greater certainty on pricing, avoiding the volatility of public markets amid heightened geopolitical risk. The fundraising comes as the conflict-related disruptions have sharply reduced oil and gas exports, Qatar halted LNG shipments while flows from the UAE and Kuwait have declined, putting pressure on fiscal revenues despite the region’s vast sovereign wealth holdings. Governments are building precautionary liquidity buffers to navigate near-term uncertainty and continue financing ambitious economic diversification plans, while also responding to rising borrowing costs and increased investor scrutiny. Although demand from large global asset managers remains solid, higher credit risk premiums and the use of less liquid private placements signal a more cautious investor environment, even as a tentative ceasefire has created a limited window for opportunistic issuance.