To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil extends rally as US escalates pressure on Iran. Oil prices rose for a third consecutive session, with Brent approaching USD86/b and WTI around USD80/b, after President Trump threatened further military strikes on Iran and the US resumed its blockade of Iranian shipping through the Strait of Hormuz. Fresh US strikes targeting Iran’s coastal military infrastructure and continued attacks on commercial vessels have kept tanker traffic through the Strait of Hormuz severely disrupted, raising concerns over global oil supplies. Although Trump withdrew a proposal to impose transit fees on ships using Hormuz, the renewed conflict has pushed oil prices to their highest level in about a month, while broader regional tensions intensified following Houthi attacks on Saudi Arabia. With shipping through Hormuz still heavily constrained and the conflict expanding across the region, markets are increasingly pricing in the risk of a prolonged supply disruption rather than a temporary geopolitical shock, keeping the near-term outlook for oil firmly skewed to the upside.

Gold stabilises as softer US inflation eases rate hike expectations. Gold prices steadied, with bullion trading near USD4,050/oz, after US inflation unexpectedly slowed in June, reducing expectations of an imminent Fed rate hike. Lower gasoline prices helped ease inflationary pressures, prompting investors to scale back bets on tighter monetary policy and supporting a rebound in gold prices. However, renewed US-Iran tensions and higher oil prices continue to pose upside risks to inflation, while Fed Chair Kevin Warsh reiterated that further policy tightening remains an option if price pressures persist. The softer inflation print has provided temporary relief for gold, but it remains caught between easing US price pressures and the risk that renewed energy market disruptions could delay the Fed’s path toward monetary easing.

MIDDLE EAST - CREDIT TRADING

End of day comment – 14 July 2026. Visually weak on spreads across the board but driven entirely by sticky cash prices, a lethargic market, and few alternatives to switch into. After being quite dear sukuks are coming out a bit as the market digests the SRCSUK deal and many locals are into summer breaks. Arb shops are all trying to sell and buy the same bonds, exacerbating street positions. Aside from the same market participants looking to catch dealers’ offsides after CPI and PBs scrambling to fill cash price orders client engagement was fairly low across the board. For KSA and Kuwait, Sov curves are 2-5bps wider after peaking at about +7bps immediately after the number. We had consistent net sellers into the number and a few sellers after hoping for a cash price pop. Banks, as they tend to, stuck on cash price so underperformed in spreads at +6-10bps. Kuwait continues to be offered on the back of the continued Iranian attacks. We traded the KFHKK 6.25 perps again today down ¼pt from yesterday's level. (Source: Matthew Dunker, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

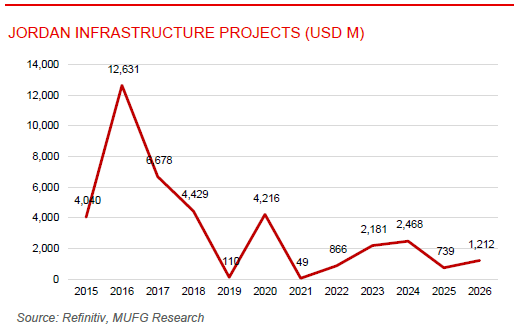

Jordan’s capital spending rises as development projects accelerate. Jordan’s capital expenditure reached approximately JOD452mn (USD637 million) in the first five months of 2026, increasing by around JD28mn from the same period of 2025, equivalent to growth of roughly 6.6% y/y. The spending was allocated under the 2026 state budget to a range of strategic development projects, including the expansion of the Risha gas field, implementation of the National Employment Strategy, and investment in vocational and technical education. The rise is economically significant because capital expenditure generally has a stronger medium-term growth impact than recurrent spending, particularly when directed toward infrastructure, energy capacity, healthcare and workforce development. It also suggests that Jordan is improving budget execution and maintaining development investment despite limited fiscal space and elevated financing needs. Looking ahead, stronger capital-spending implementation should support domestic demand, job creation and productive capacity, although the overall growth impact will depend on whether projects are completed on schedule and accompanied by sufficient private-sector investment.

Egypt to launch eight integrated logistics and trade corridors. Egypt is developing eight integrated logistics and trade corridors to strengthen its position as a regional transport and logistics hub linking Asia, Africa and Europe. The plan includes a northern Arab trade corridor connecting Europe with the Levant via Jordan, Iraq and Syria, and a southern corridor linking Europe with Saudi Arabia and the Gulf through Safaga Port and NEOM. The network will connect ports on the Mediterranean, Red Sea and Suez Canal with railways, highways, logistics centres and industrial zones, while supporting major initiatives such as IMEC, China’s Belt and Road Initiative and the Iraq-Turkey Development Road. The project forms part of Egypt’s broader strategy to enhance connectivity and capitalise on evolving regional trade routes, although its long-term success will depend on attracting cargo volumes, timely infrastructure delivery and maintaining competitiveness against alternative logistics corridors.