To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil stabilises as peace talks loom despite ongoing blockade. Oil prices steadied after recent losses, with Brent holding below USD95/b and WTI near USD91/b, as the market balanced hopes for renewed US-Iran negotiations against ongoing supply disruptions from the blockade of the Strait of Hormuz. President Trump indicated talks could resume within days, raising optimism for a ceasefire, even as US forces continue to restrict Iranian oil exports and Iran considers pausing shipments to avoid escalation. The conflict has significantly disrupted global energy markets, tightening supplies and weighing on demand, with the IEA warning of reduced consumption. While a potential de-escalation could gradually restore up to 2-3mb/d of supply, rising US crude inventories and continued geopolitical uncertainty are keeping oil markets volatile. Going forward, despite this calmer mood, the difficulty of restarting global trade routes means the current supply crunch will linger, preventing prices from falling too far.

Gold holds near USD4,850/oz on hopes of US-Iran deal. Gold prices held firm near USD4,850/oz, supported by growing optimism that the US and Iran may reach a negotiated settlement, easing inflation concerns tied to recent energy supply shocks. The metal’s gains were reinforced by a weaker US dollar and strong equity markets, while stabilising oil prices reduced pressure on inflation expectations that had previously weighed on gold. President Trump signalled that talks could resume within days, boosting sentiment despite ongoing tensions around the Strait of Hormuz, where a US blockade continues to restrict Iranian exports. Although gold has declined about 8% since the conflict began due to earlier liquidity-driven selloffs and expectations of higher interest rates, lingering geopolitical risks, potential tariff reinstatements, and continued energy disruptions are maintaining underlying support for prices.

MIDDLE EAST - CREDIT TRADING

End of day comment – 14 April 2026. Markets remain firmly risk on. DJT set the markets up on the front foot with his post London comment and the mixture of higher UST and tighter spread made for some bigger moves in cash today. Long end ADGB has found a bid, although there are still a few bonds to work through, 54s closed _0.875pt/-4bp. ADGB also did another private placement of 2bn in 33s at undisclosed reoffer level, on the back of it the street saw 150mm of 34s going through today in the low T+30s. Qatar was inactive, there aren't any sellers or lose bonds around and I had the curve 3/bp tighter at EOD. SHARSK/SHJGOV caught a strong bid today led by SHARSK 36s closing +0.75pt/-7bp. OMAN also continued to squeeze as the street wants to buy long end with only small RM selling into higher prices, 51s closed +1pt/-6bp. Quasi sovereign tightened to the same extend than sovereign today, seen some activity in ADQABU and MUBAUH with duration bonds outperforming and both curves -3/-5bp.

MIDDLE EAST - MACRO / MARKETS

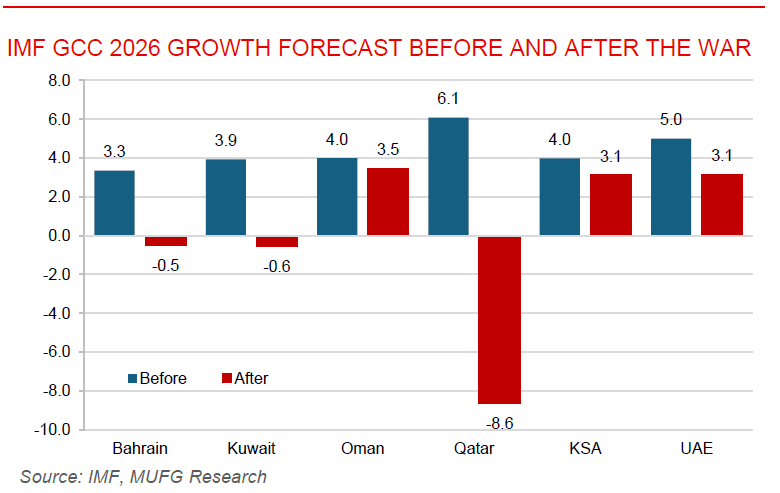

IMF cuts global growth outlook amid oil shock and war risks. The International Monetary Fund (IMF) downgraded its global growth forecast to 3.1% for the year from 3.3%, citing the economic fallout from the Middle East conflict, which has triggered a major energy shock and heightened uncertainty. The near-closure of the Strait of Hormuz and resulting surge in oil prices are expected to drive inflation higher and weigh on economic activity, particularly in emerging markets where growth was revised down to 3.9%. while the baseline assumes a short-lived conflict, the IMF warned that prolonged disruptions or severe damage to energy infrastructure could push global growth as low as 2%, near recession levels, with inflation rising sharply. Advanced economies are relatively less affected, with the US still expected to grow 2.3%, but Europe faces more pronounced slowdowns, and the Middle East region is set for a sharp deceleration. Overall, the outlook has “abruptly darkened”, with risks tiled to the downside as the trajectory of the conflict and energy markets remains highly uncertain. The IMF is set to release its Regional Economic Outlook for the Middle East this Thursday.

IMF explores emergency support options for Lebanon amid war impact. The IMF is in discussions with Lebanon over fast-track financial assistance of around USD800 million to USD1bn to help the country cope with the economic and humanitarian fallout from the ongoing Middle East conflict. The proposed funding would focus on budget support and urgent relief efforts as Lebanon, already in default since 2020 and facing a prolonged economic crisis, struggles with the added strain of war-related disruptions. While negotiations for a broader IMF reform program continue under Prime Minister Nawaf Salam, immediate financing has become a priority given the country’s fragile situation, including s sharply contracted economic and limited access to traditional IMF emergency tolls due to its debt default. The situation is further exacerbated by ongoing conflict within Lebanon underscoring the country’s acute vulnerability and urgent need for external support.