To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds steady as Trump-Xi talks begin amid ongoing Hormuz disruption. Oil prices established as US President Trump and Chinese President Xi began high-level talks in Beijing, while the Iran was and the near closure of the Strait of Hormuz continued to disrupt global energy markets. Brent traded near USD106/b and WTI hovered around USD101/b, with investors balancing hopes for improved US-China relations against persistent supply risks in the Middle East. The IEA warned that global oil markets will remain “severely undersupplied” until at least October even if the conflict ends next month, as flows through Hormuz have dropped sharply since hostilities began in late February. Meanwhile, US pressure on Iranian oil exports intensified through additional sanctions and banking restrictions targeting Chinese-linked trade. Markets are also monitoring the expiry of a US sanctions waiver allowing purchases of Russian oil cargoes, which could further tighten supply conditions for major importers such as India.

Gold pressured by rising US inflation and higher rate expectations. Gold remained under pressure near USD4,700/oz as stronger than expected US inflation reinforced expectations that the Fed will keep interest rates elevated for longer. Gold extended losses after US wholesale inflation accelerated in April to its fastest pace since 2022, while Treasury yields climbed toward their highest levels since July, weighing on non-yielding assets. Additional pressure came after the Senate confirmed Kevin Warsh as the next Fed chair, raising investor focus on the future direction and independence of monetary policy. Inflation concerns have intensified as US consumer prices rose 3.8% y/y, driven by sharp increases in gasoline, housing, food, and travel costs following the Iran war and ongoing disruptions in global energy markets.

MIDDLE EAST - CREDIT TRADING

End of day comment – 13 May 2026. With higher UST yields there was again pressure on the long end of the curves. QATAR 50s was again for sale closing -0.5pt/+3bp. Long end ADGB did a touch better, closing 54s -0.375pt/+2bp. For now, higher yields in the long end are bringing sellers out as the fear of more volatility/ weakness trumps the higher yields. That again is not as pronounced in the shorter end/belly of the curves. Whilst prices adjust to the left, spreads are gradually tightening, seen 10y ADGB closing -0.10pt/-1bp, with interest to buy 33s and 36s. Equally financial bonds are reasonably sticky in cash terms with prices in the main senior bonds hardly changed and spreads 2/3bp tighter. In quasis, QPETRO bonds were active, there is still buying interest in 31s (unch/-2bp) and 41s (unch/-2bp) but sellers in 51s (-0.25pt/+1bp) which is more corelated to risk sentiment/ sovgn moves. Corporate bonds saw the first buyers today in ALDAR hybrids, 55s closed unch/-2bp and in DPWDU short end where 29s and 30s where bid closing unch/-2bp. Overall activity though was very low, and markets start to feel uneasy about the rates move.

MIDDLE EAST - MACRO / MARKETS

Middle East war expected to slow Islamic Finance growth in 2026. S&P Global Ratings expects global Islamic finance growth to slow to 5%-10% in 2026 from 10.2% in 2025, as the Middle East war disrupts energy flows, weakens economic activity, and pressures fiscal balances across key GCC markets. The agency said the effective closure of the Strait of Hormuz is weighing on growth prospects in GCC while also affecting trade, tourism, real estate, and investment activity. Although higher oil prices offer some support, reduced export volumes are expected to increase reliance on debt issuance, with governments likely favouring conventional bonds over sukuk in some cases. S&P’s base case assumes the US and Iran eventually reach an agreement allowing oil flows to gradually resume, though disruptions may persist. Despite slower growth, Islamic banks are expected to remain relatively resilient, supported by continued lending demand and market share gains in core markets, while sustainable finance and digitalization remain key long-term growth drivers for the industry.

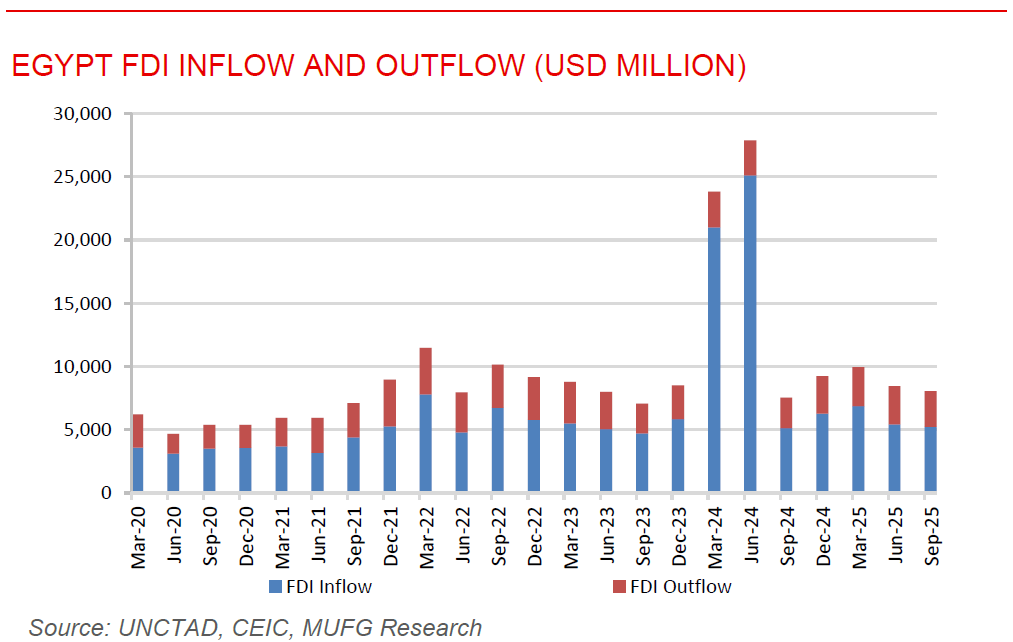

Egypt unveils major investment zone plan to boost long-term FDI. Egypt unveiled a major long-term investment initiative targeting up to USD77.5bn of investments across seven new investment zones over the next 20 years, as the government intensifies efforts to position the country as a regional FDI hub. The programme aims to support 214 projects and create around 1.2 million jobs, building on the existing network of active investment zones that already host more than 1,200 projects. A key pillar of the strategy is the expansion of the “Golden License” system, which streamlines approvals for strategic projects through a single-window mechanism covering land allocation, construction, and operating permits. The initiative reflects Egypt’s broader push to attract private capital through regulatory reforms, infrastructure upgrades, and trade facilitation measures. The broader signal is that Egypt is positioning itself for a stronger FDI cycle in the second half of 2026, supported by structural reform momentum and improving investor confidence.