To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil jumps as US-Iran escalation raises Hormuz supply risks. Oil prices rose after a second round of US strikes on Iranian targets heightened tensions in the Middle East and raised concerns over further disruptions to energy flows through the Strait of Hormuz. Brent crude briefly climbed above USD95/b and WTI approached USD93/b as Iran threatened to halt vessel movements through the strategic waterway, although US officials maintained that commercial shipping continued to transit the strait. the latest escalation adds uncertainty to already fragile ceasefire negotiations and risks prolonged supply disruptions that have constrained global crude, fuel, and LNG exports since the conflict began. While some Gulf oil shipments have gradually resumed, overall flows remain well below pre-war levels, keeping geopolitical risk premiums elevated. Also, US crude inventories fell for a seventh consecutive week, underscoring tightening supply conditions and providing additional support to oil prices.

Gold volatile as renewed US-Iran strikes fuel inflation concerns. Gold experienced sharp swings after the US launched another round of strikes against Iran, increasing uncertainty around efforts to reach a peace agreement. Gold initially fell toward USD4,000/oz before rebounding, reflecting volatile investor sentiment as Iran announced plans to close the Strait of Hormuz to all vessels. The prolonged disruption to global energy flows has pushed oil prices higher and intensified inflation concerns, increasing the likelihood that central banks will maintain a tighter monetary stance. Recent US inflation data showed price growth accelerating to its fastest pace in more than three years, reinforcing expectations of higher for longer interest rates. Gold remains significantly below its pre-conflict levels, with additional selling pressure emerging after prices broke below key long-term technical support levels.

MIDDLE EAST - CREDIT TRADING

End of day comment – 10 June 2026. The Market was on average +2/3bp and it is starting to feel we widen every day a tad. To be sure, it is mostly coming from the rates side, but cash prices were flat at best and in some cases a touch lower. It also starting to add up over a week where for example the ADGB curve is 7/10bp wider depending on the bond. In terms of flows ETFs remain the marginal flow which skews the buyer: seller ratio which today was about 1:2. Long bonds underperformed today as the risk off mood took cash prices 0.125pt lower on average and spreads +3bp. UAE related index names continue to underperform as the index phase out flows continue to worsen technicals. To be sure, price action is orderly and bid side liquidity abundant, who wants out, gets out. Another underperformer recently was the belly of OMAN, today led by OMAN 32s closing -0.125pt/+4bp and over the week is now 15bp wider. On the new issue side, DIBUH 6.25 perps had a strong reception with local retail flows supporting secondary markets, bonds closed 100.40/100.50 from 100 reoffer. The market has developed a certain immunity towards US/Iran headlines, that said there continues to be a buyer strike and good news from that front is needed to change the flows. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

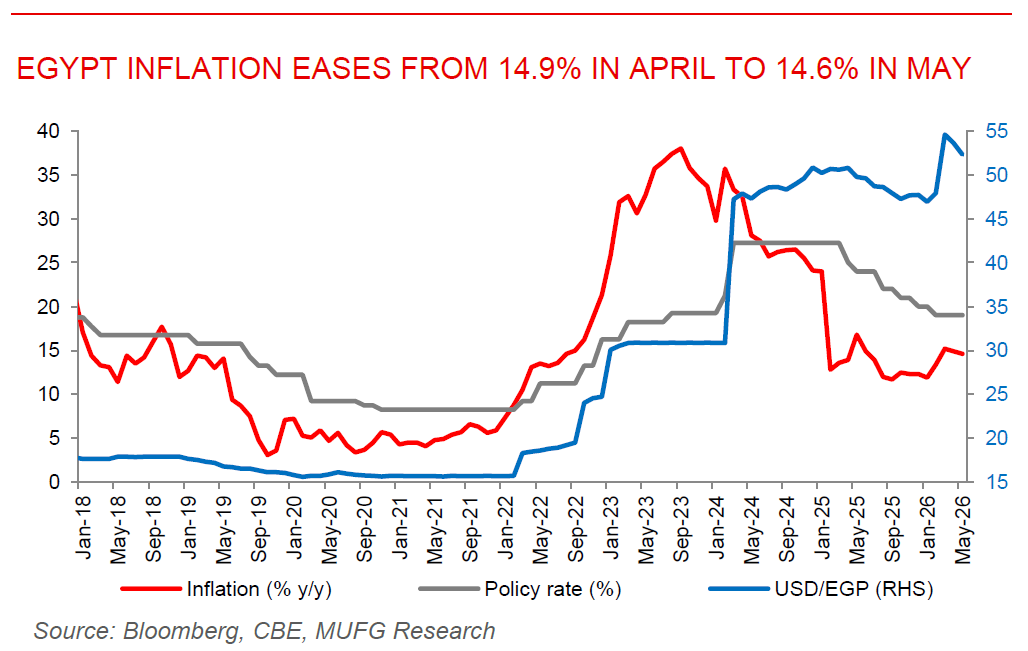

Egypt inflation eases again, supporting expectations of rate hold. Egypt’s inflation slowed from 14.9% y/y in April to 14.6% y/y in May, despite ongoing pressures from higher energy costs and currency weakness linked to the Middle East conflict. The moderation was largely driven by favourable base effects and relative exchange-rate stability, which helped offset the impact of rising fuel and commodity prices. Core inflation remained unchanged at 13.8% y/y, although monthly inflation accelerated to 1.6%, indicating that underlying price pressures remain present. The data strengthens expectations that the Central Bank of Egypt (CBE) will keep interest rates unchanged at its July meeting, extending its cautious wait-and-see approach. While inflation as surprised on the downside in recent months, the CBE recently revised its 2026 inflation forecast higher and continues to warn that prolonged regional tensions, higher energy prices, and fiscal adjustment measures could delay the return to single-digit inflation.

Saudi economy supported by oil recovery and strong investment activity. Saudi Arabia’s economy maintained solid momentum in Q1 2026, with nominal GDP rising 6.3% y/y to SAR1.27 trillion and real GDP expanding 3.0%, supported by a 12.3% increase in oil sector activity and resilient domestic demand. Investment activity strengthened notably, with gross fixed capital formation rising 5.1% after weakness through much of 2025, driven by both private sector spending and a sharp 54% increase in government investment. Economic fundamentals remained supportive, with inflation contained at 1.7% in April, and unemployment declining to 7.2%. credit to SMEs continued to expand, reaching a record SAR46bn, while foreign investor holdings in Saudi capital markets rose to SAR458bn. Although the PMI eased to 52.8 in May, it remained firmly in expansionary territory, highlighting the continued resilience of the Kingdom’s non-oil economy amid a supportive oil price environment.