To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil rebounds as fresh US-Iran clashes threaten fragile ceasefire. Oil prices rose after the US launched strikes on Iranian targets in response to the downing of an American helicopter near the Strait of Hormuz, raising concerns that recent progress toward de-escalation could unravel. Brent crude briefly climbed above USD93/b while WTI approached USD90/b, as markets assessed the risk of renewed disruptions to regional energy supplies. Iran responded with drone attacks targeting US assets in the Gulf, highlighting the continued fragility of the ceasefire and ongoing peace negotiations. The latest escalation threatens to prolong restrictions on traffic through the Strait of Hormuz, a critical route for global oil and gas exports, while declining US crude inventories underscore tightening supply conditions. Going forward, developments in US-Iran negotiations, security conditions around Hormuz, and the pace of inventory drawdown will be key drivers of oil market sentiment.

Gold slides as renewed US-Iran clashes reinforce higher-rate concerns. Gold extended its decline, falling below USD4,175/oz, after fresh military exchanges between the US and Iran raised concerns that efforts to end the Middle East conflict could stall. The latest escalation, including US strikes on Iranian targets and Iran’s retaliatory actions, has increased uncertainty around the security of the Strait of Hormuz, a key route for global energy supplies. Rising oil prices have renewed inflation concerns, strengthening expectations that major central banks may keep interest rates elevated for longer, a negative backdrop for non-yielding assets such as gold. The precious metal is now roughly 20% below its pre-conflict level, with additional selling pressure emerging after prices fell below key technical support levels closely watched by investors.

MIDDLE EAST - CREDIT TRADING

End of day comment – 09 June 2026. Flows remained somewhat heavy today as ETFs continued to sell bonds seconded by RM. Cash prices though were mostly unmoved throughout the day and spreads had a bit a rollercoaster with UST. With the equity vol in the last hour and synthetic credit widening off the tights, we are seeing more selling into the close. A theme of the last 2/3 sessions has been that belly bonds underperform duration, take ADGB 31s closing -0.10pt/+4bp vs 54s -0.125pt/unch. Then technicals remain sticky, take the QATAR curve where 33s PP bonds have an ongoing offer and widened +7bp (today +2bp) over a week whereas 34s/35s have been unch in spread over the same time. There was strength in SHARSK/SHJGOV today closing up to +0.125pt higher and about 3bp tighter on average. On the new issue side DIBUH priced a 1bn USD PNC6 AT1 at 6.25%. It looks like size over price was prioritised here. In the corporate world we have seen ALDAR hybrid bonds starting to clear and closing +0.25pt/-3bp. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

Kuwait crude exports signal gradual recovery in Gulf energy flows. Kuwait has begun offering crude cargoes to Asian refiners for the first time since the outbreak of the Iran conflict, signalling a gradual recovery in oil exports through the Strait of Hormuz. State-owned Kuwait Petroleum Corporation is reportedly marketing at least 4 million barrels of crude to buyers in China and South Korea, with the cargoes already having successfully transited the waterway. The move follows similar export activity by UAE producers and suggests that Gulf exporters are increasingly finding ways to restore shipments despite ongoing security risks and navigation challenges. While overall oil flows from the Gulf remain well below pre-war levels, the resumption of Kuwait exports points to improving supply conditions and offers some relief to Asian refiners that depend heavily on Middle Eastern crude grades. The development also indicates that regional producers are adapting to the new operating environment through closer coordination of tanker movements and alternative export logistics.

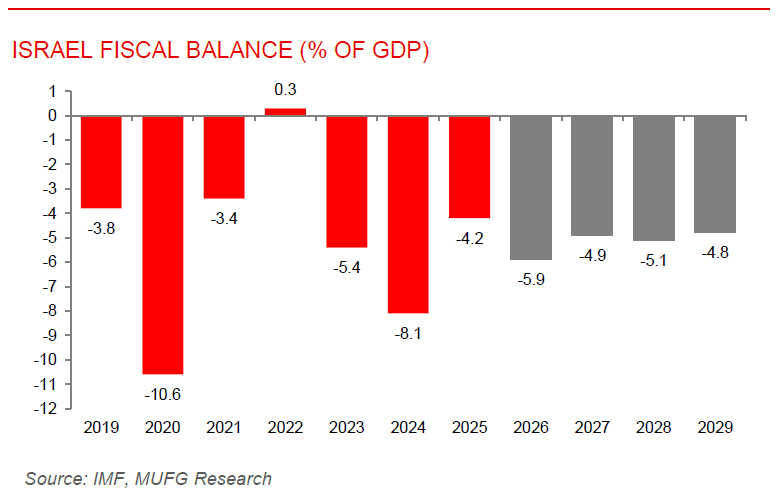

Israel’s fiscal deficit narrows, supported by strong revenue growth. Israel’s fiscal position improved in May 2026, with the rolling 12-month budget deficit narrowing to 3.75% of GDP, the lowest level since late 2023 and well below the government’s full-year target of 4.9%. The improvement was driven by robust tax revenue collection, including significant one-off receipts from large technology-sector transactions, while government spending growth remained relatively restrained despite ongoing military operations. Revenues continued to benefit from the resilience of Israel’s technology sector, helping offset the fiscal burden of elevated defence expenditures and higher debt-servicing costs. Nevertheless, the underlying fiscal picture remains more challenging than the headline figures suggest, as defence spending has increased structurally since the conflict began and additional military and reconstruction-related expenditures are expected. As a result, while recent data point to improving fiscal metrics, investors caution that a portion of the deficit reduction reflects exceptional revenue gains rather than a broad-based improvement in the fiscal balance.