To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds weekly gains despite Hormuz disruptions. Oil prices steadied, with Brent trading above USD76/b and WTI near USD72/b, as markets balanced ongoing US-Iran negotiations against renewed security risks in the Strait of Hormuz. Although technical talks between US and Iran remain ongoing, recent US strikes on Iranian targets, retaliatory attacks, and multiple incidents involving commercial vessels have significantly reduced tanker traffic through the strategic waterway, keeping supply concerns elevated. Despite the escalation, both sides have stopped short of returning to full-scale conflict, and elements of the interim agreement remain intact, preventing a more severe disruption to regional energy exports. Market participants are also closely monitoring Gulf producers’ export allocations and the IEA’s latest oil market assessment for further signals on supply conditions.

Gold holds steady as geopolitical risks offset rate expectations. Gold prices traded broadly unchanged, with gold hovering around USD4,120/oz, as investors balanced renewed US-Iran tensions against expectations that the Fed will keep interest rates elevated. While diplomatic talks between US and Iran continue, recent military exchanges and the reimposition of US sanctions on Iranian oil have revived concerns over energy prices and inflation. At the same time, the Fed’s June meeting minutes reinforced a cautious policy stance, suggesting policymakers remain prepared to keep rates higher if inflation proves persistent. Continued central bank purchases, particularly by China, have also provided an important source of support for gold. Gold’s direction is becoming less about geopolitical headlines and more about whether higher energy prices feed into inflation expectations. If the latest escalation proves temporary, monetary policy is likely to remain the dominant driver of gold prices.

MIDDLE EAST - CREDIT TRADING

End of day comment – 09 July 2026. Early close on an uneventful day. The spread widening continues though. Early morning we had again US strikes on Iran and retaliation against BHRAIN, Kuwait and Qatar today. Oil prices though never signalled concern, UST recovered and seem to have re-corelated with oil price moves. Flows again were on the low side, it was good to see some RM buying bonds in the morning, but ETF outflows and dealer longs killed any attempt to walk cash prices higher today. Like yesterday ADGB curve was the strongest, once again led by long end 49s closed +0.375pt/-1bp. But that is about the only sector closing tighter today. The rest especially quasi sovgn bonds was very sticky in cash price terms and widened with the UST move about 2/4bp. Into the close there are some dealer bids to bring quasis more in line with sovgn/macro moves. But what is missing at the end of the day are buyers to clear the technicals. As said yday the path of least resistance is wider, esp if UST yield were to move lower. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

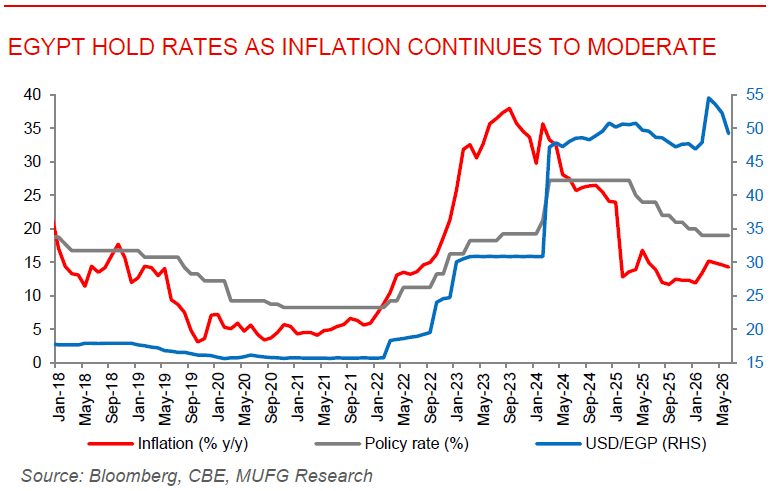

Egypt holds rates as inflation continues to moderate. The Central Bank of Egypt (CBE) kept its deposit rates unchanged at 19% and lending rates at 20% for a third consecutive meeting, in line with market expectations, as it balanced continued progress in disinflation against persistent regional uncertainty. Annual inflation eased to 14.3% y/y in June from 14.6% y/y in May, marking another downside surprise, while the Egyptian pound has appreciated since the previous MPC meeting, reflecting improving macroeconomic conditions and stronger external financing. Nevertheless, the CBE expects inflation to rise temporarily during Q3 2026 due to unfavourable base effects and reiterated its commitment to maintaining a restrictive monetary stance until inflation converges toward its 7% (±) target by H2 2027. The decision also reflects caution amid renewed US-Iran tensions and the potential impact of higher energy prices on inflation and external balanced. While our base case remains for rates to stay on hold through the remainder of 2026, continued downside inflation surprises, improving external conditions, and easing regional tensions would strengthen the case for a gradual rate cut alter this year, most likely in Q4 2026.

Turkey and Iraq move to extend strategic oil pipeline agreement. Turkey and Iraq are expected to sign a one-year extension of the Kirkuk-Ceyhan pipeline agreement before its July 27 expiry, ensuring the continued operation of the key export route linking northern Iraq to Turkey’s Mediterranean port of Ceyhan. The pipeline, which has a capacity of around 1.6mb/d has remained largely idle since 2023 following an international arbitration dispute, but its extension is strategically important as it provides Iraq with an alternative export corridor that bypasses the Strait of Hormuz, where roughly 90–95% of Iraq’s crude exports currently transit via southern Gulf terminals. For Turkey, the agreement reinforces its ambition to become a regional energy hub while supporting transit revenues and energy security. If exports resume, the pipeline could significantly diversify Iraq’s export infrastructure and reduce its dependence on the Gulf.