To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil jumps as Israel-Iran clashes threaten fragile ceasefire. Oil prices surged after Israel launched strikes on military targets in Iran in response to missile attacks from Iran, raising concerns that a fragile regional ceasefire could unravel. Brent briefly climbed above USD97/b while WTI rose past USD94/b, as renewed hostilities added uncertainty to already stalled US-Iran peace negotiations. The conflict continues to disrupt energy flows through the Strait of Hormuz, a critical route for global oil and gas exports, while tensions involving Lebanon and Hezbollah remain a major obstacle to a broader settlement. Despite ongoing diplomatic efforts, markets remain concerned that even a peace agreement would not immediately restore normal energy flows due to damaged infrastructure, mined waterways, and production outages. The renewed escalation has reinforced fears of prolonged supply disruptions, keeping upward pressure on oil prices despite OPEC+ plans to gradually increase output.

Gold falls as renewed Israel-Iran tensions and higher rate expectations weigh. Gold extended its decline, falling toward USD4,300/oz, as renewed military exchanges between Israel and Iran heightened inflation concerns and reinforced expectations of higher interest rates. The latest escalation, including Israeli strikes on Iranian targets and Iran’s missile launches, has further complicated efforts to secure a broader regional peace agreement. Persistent disruptions to energy flows through the Strait of Hormuz continue to support oil prices and fuel inflation fears, reducing the appeal of non-yielding assets such as gold. Additional pressure came from stronger than expected US economic data, which increased expectations that the Fed could keep rates higher for longer. Despite the recent weakness, continued gold purchases by China’s central bank, which added around 10 tonnes to its reserves last month, highlight ongoing long-term demand for the precious metal.

MIDDLE EAST - CREDIT TRADING

End of day comment – 05 June 2026. It was a constructive morning today, flows were getting better two ways compared to yday with some buyers stepping into long end bonds. Post NFP the market went hiding and not much traded. ETFs were sellers on the back of the macro risk off move. After moves like this in underlying rates, especially the flattening we have seen in UST it will normally take 2/3 days for spreads to normalise. At eod, we are closing our long bonds about flat in spreads and 2/10y bonds -3/-4bp. One credit which stood a bit out today was Oman which was under pressure in the belly, OMAN 31s closed -0.625pt/+3bp. UST Yields up/spreads tighter and vice versa works in a mean reverting market. If this though is the start of a repricing of FED rate path expectations there can be no doubt that the cash market looks vulnerable at these spread levels. Time will tell. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

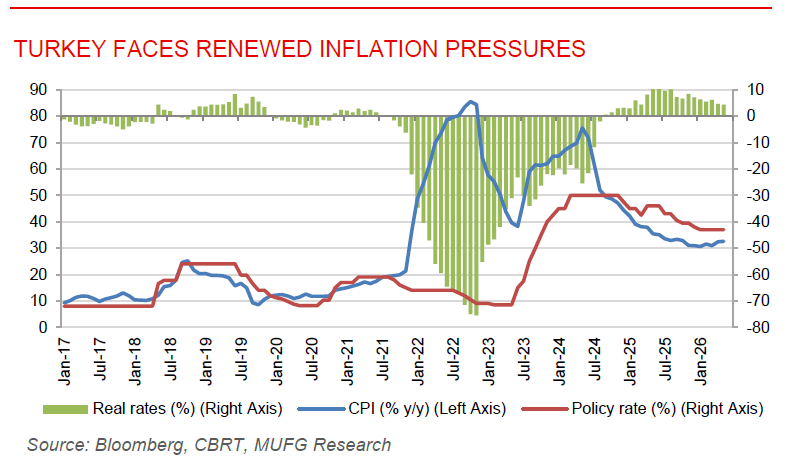

Turkey inflation rises again as energy costs keep pressure on prices. Turkey’s annual inflation rose to 32.6% y/y in May from 32.4% y/y in April, marking a second consecutive monthly increase as higher energy costs linked to the Middle East conflict continued to filter through the economy. However, monthly inflation slowed sharply to 1.7% from 4.2% in April, suggesting that underlying price pressures may be easing despite the challenging external environment. The data has reinforced expectations that the Central Bank of Turkey (CBRT) could keep its policy rate unchanged at 37% at its meeting on June 11, having already tightened liquidity conditions following the outbreak of the regional conflict. Turkey remains particularly vulnerable to higher oil and gas prices due to its heavy reliance on energy imports, prompting policymakers to suspend their previous inflation forecast range and adopt a more cautious stance. While softer monthly inflation offers some relief, persistent currency volatility, elevated energy costs, and geopolitical uncertainty continue to pose risks to the disinflation process, with the central bank still targeting year-end inflation of 24%.

Aramco price cut signals easing market tightness but highlights fiscal pressure. Saudi Aramco cut the official selling price (OSP) of its flagship Arab Light crude to Asia by USD6/b for July-loading cargoes, lowering the premium to USD9.5/b above the Oman/Dubai benchmark. The move, larger than market expectations, marks a second consecutive monthly reduction following the sharp spike in crude differentials caused by disruptions to Strait of Hormuz flows earlier this year. While the premium remains historically elevated, the decline reflects softer Asian demand, particularly from China, as high oil prices have squeezed refinery margins and reduced crude purchases. The pricing adjustment suggests that the extreme tightness seen in physical oil markets during the peak of the conflict may be easing. However, lower realised oil prices could weigh on Aramco’s earnings, dividend capacity, and Saudi Arabia’s fiscal position at a time when the Kingdom is already running a budget deficit. Looking ahead, August OSPs, Aramco’s Q2 earnings, Asian refining margins, and developments in Hormuz shipping flows will be key indicators of whether market conditions continue to normalise or tighten again.