To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil surges as US strikes Iran, escalating Middle East tensions. Oil prices jumped, with Brent rising above USD76/b and WTI climbing above USD72/b, after US launched strikes on more than 80 targets in Iran in response to attacks on commercial shipping in the Strait of Hormuz, significantly escalating regional tensons. The US also revoked the sanctions waiver that had allowed limited Iranian oil exports, while Iran vowed to retaliate and reports emerged of missile and drone attacks targeting Bahrain and Kuwait. The renewed escalation has reignited concerns over supply disruptions through the Strait of Hormuz, with attacks on multiple commercial vessels highlighting the continued vulnerability of regional energy infrastructure. Going forward, the latest developments are likely to restore part of the geopolitical premium that had largely unwound in recent weeks, although the broader outlook will depend on whether the conflict escalate further or diplomatic efforts resume.

Gold holds steady as Fed outlook offsets geopolitical risks. Gold prices traded in a narrow range hovering around USD4,100/oz, as investors balanced renewed geopolitical tensions against expectations for US monetary policy. Fresh US airstrikes on Iran and higher oil prices revived concerns over inflation, reinforcing expectations that the Fed could keep interest rates higher for longer, a headwind for the non-yielding gold. Markets are now awaiting the release of the Fed’s June meeting minutes for further guidance on the policy outlook. Meanwhile, continued gold purchases by China’s central bank and strong reserve diversification by global central banks provided underlying support for prices. Gold is likely to remain range-bound in the near term with geopolitical uncertainty offering support while higher for longer interest rate expectations continue to limit upside potential.

MIDDLE EAST - CREDIT TRADING

End of day comment – 07 July 2026. Price action becomes more and more flow driven and/ or positioning driven. That makes again today for a wide distribution in daily change outcomes. There was some weakness in SHJGOV long end into the close with 50s/51s -1pt/+8bp. But other than that long end bonds held relatively well today, ADGB especially which has buyers in 49s and 54s closing unch/-4bp. Quasis still has MUBAUH short/belly bonds sub 7y underperforming on dealer longs, 33s closed -0.25pt/+2bp. In fins new MASQUH 6.625 perps had an ugly day closing -0.375pt/+7bp. On the strong side FABUH sukuks had buyers with the highest print in 29s closing +0.125pt/-7bp. Flows overall dropped markedly from yday and trax about 50% lower than a normal day. On the new issue front Saudi Real Estate priced 2.75bn sukuk: 1.25bn 5.5y @T+85bp and 1.5bn 10y @T+95bp which offer a 10bp NIP. Ajman Bank priced 300mm of PNC 5.5 AT1 sukuks at 6.5%. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

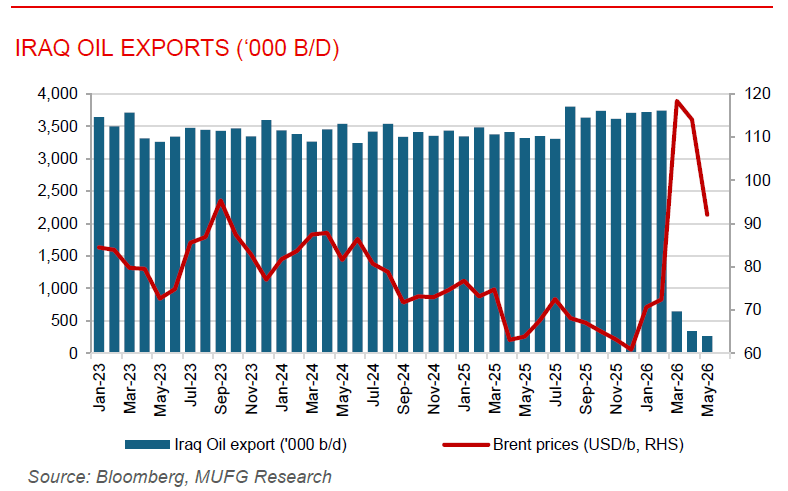

Iraq restores oil output as exports bottlenecks ease. Iraq has restored production at three major southern oil fields, West Qurna 1, North Rumaila, and Artawi, to full capacity as tanker arrivals increase and export operations through the Strait of Hormuz continue to recover. The move reverses temporary production cuts implemented in late June, when intermittent shipping disruptions and limited storage capacity constrained exports despite the US-Iran interim peace agreement. Improving tanker availability and the resumption of crude loadings are now allowing Iraq to gradually increase exports, with international traders also helping market Iraqi crude to Asian refiners. Although Iraq remains behind Saudi Arabia and the UAE in returning to pre-war export levels, the latest production increase signals improving export logistics and a continued normalisation of the country’s oil sector. Going forward, the pace of tanker movements through Hormuz and Iraq’s ability to sustain higher export volumes will be key to its recovery and efforts to regain market share in Asia.

Egypt’s non-oil PMI falls to multi-year low. Egypt’s non-oil private sector weakened further in June, with PMI falling to 46.0 from 47.1 in May, marking the sixth consecutive month of contraction and the weakest reading since January 2023. Business activity was weighed down by weak domestic demand, slowing new orders, supply chain disruptions, and higher input costs linked to the regional conflict and shipping disruptions through the Strait of Hormuz. Output declined for a fifth consecutive month, while firms continued to reduce employment and purchasing activity, although inflationary pressures eased from May’s elevated levels as input and output cost growth moderated. Despite the challenging operating environment, business confidence remained cautiously positive on expectations that easing geopolitical tensions, lower energy prices, and government support could help improve activity in H2 2026. However, the latest PMI points to a moderation in Egypt’s economic growth momentum during the second quarter. Going forward, easing regional tensions and improving supply chains should support a gradual recovery, although weak domestic demand is likely to keep business conditions subdued in the near term.