To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil stabilises as US-Iran talks raise hopes for Hormuz reopening. Oil prices steadied after a sharp decline, with Brent trading below USD102/b and WTI near USD96/b, as markets assessed renewed diplomatic efforts between the US and Iran aimed at ending the conflict and gradually reopening the Strait of Hormuz. US has reportedly presented Iran with a preliminary framework that could lead to easing the blockade and restoring shipping flows, although Iran has yet to respond. Despite signs of progress, tensions remain high, with President Trump warning that military action could resume if no agreement is reached. The war has severely disrupted global energy markets since February, leaving shipping traffic through Hormuz near standstill and driving sharp volatility in oil prices. Meanwhile, rising fuel costs are increasing political pressure on the US administration, while record US fuel exports and declining crude inventories highlight the ongoing global supply crunch caused by the conflict.

Gold steadies as hopes for US-Iran ease inflation fears. Gold stabilised near USD4,690/oz after posting its biggest daily gain since March, as investors assessed renewed optimism surrounding a potential US-Iran agreement to end the conflict. Falling oil prices and easing inflation concerns pushed bond yields and the dollar lower, supporting gold prices. Iran is reportedly reviewing a new US proposal that could lead to the lifting of the blockade on the Strait of Hormuz and an end to the nearly 10-week war, while President Trump reiterated that a deal could be close if Iran accepts US conditions. Despite improving market sentiment, officials from the Fed cautioned that inflation remains above target, highlighting the risk that interest rates could stay elevated for longer. Gold has fallen around 11% since the conflict began, as the energy stock and Hormuz closure fuelled expectations of tighter monetary policy.

MIDDLE EAST - CREDIT TRADING

End of day comment – 06 May 2026. Yields lower and spreads tighter. The market started on the front foot with Trump suspending project freedom and around mid-morning more headlines were crossing the tape about a possible peace agreement. The market peaked early afternoon when both sides walked back a touch from the axios report and we are closing off the highs/tights. Flows were still balanced once the market repriced, especially away from sovgn bonds there are still willing sellers which overall balanced the flows buyers to sellers 1:1. Sovgn bonds outperformed though, in IG led by ADGB long end where 54s closed +1pt/-5bp. In higher betas SHJGOV long end got bid up strongly with 50s closing +1.5pt/-13bp. Qatar and Oman lagged a touch with both curve -2/-3bp as they had outperformed all April. Quasi sovgn issuers underperformed as bonds sold yday were still floating around the market, especially in UAE names, ADQABU 34s was active and closed +0.375pt/-1bp.

MIDDLE EAST - MACRO / MARKETS

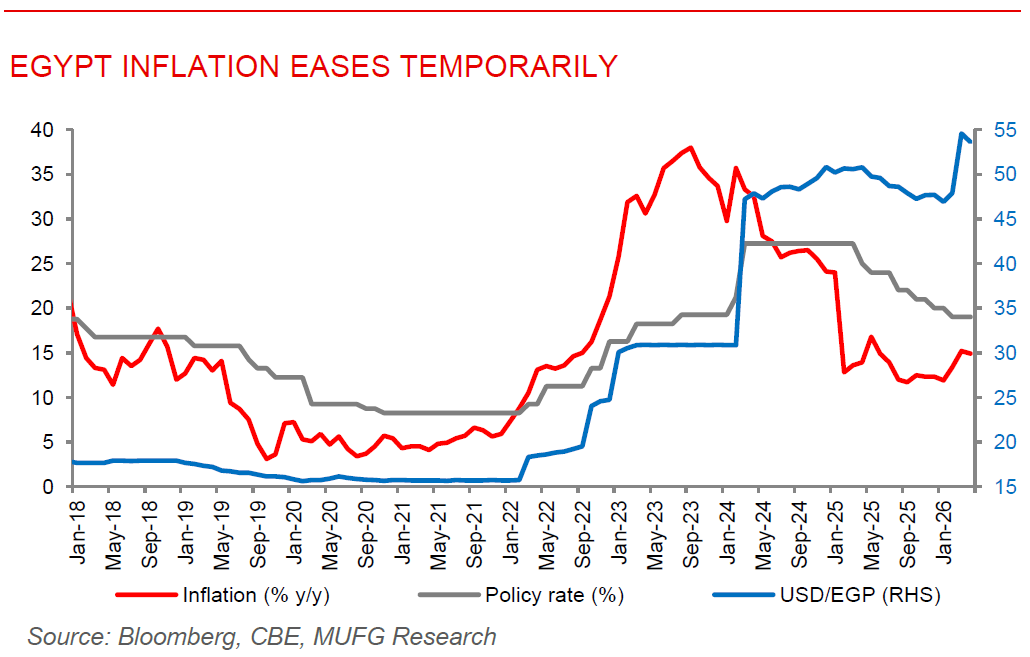

Egypt inflation eases temporarily amid ongoing regional pressures. Egypt’s inflation unexpectedly slowed to 14.9% y/y in April from 15.2% y/y in March, despite mounting economic pressures stemming from the Iran war, higher fuel costs, and continued weakness in the Egyptian pound. The slowdown came against consensus for a sharper increase and may reduce the likelihood of an immediate interest rate hike by the Central Bank of Egypt (CBE) at its upcoming meeting. However, the broader outlook remains challenging as Egypt continues to face spillover effects from regional instability, including higher energy import costs linked to disruptions in the Strait of Hormuz and renewed pressure on foreign capital flows and the currency. Although inflation has declined substantially from the record highs seen in 2023, authorities continue to warn of upside risks from energy price increases and geopolitical uncertainty. Looking ahead, inflationary pressures are expected to reaccelerate in the coming months, while the CBE is expected to keep rates unchanged at its policy meeting on May 21 amid persistent inflation risks.

Abu Dhabi explores new defence investment vehicle amid regional tensions. Abu Dhabi is reportedly considering the creation of a new defence-focused investment vehicle aimed at strengthening the UAE’s military capabilities and expanding its global defence footprint following heightened regional conflicts. Preliminary discussions involving senior officials have focused on establishing a platform that could invest in international defence manufacturers, drone technology firms, cybersecurity, and advanced military technologies across the US, Europe, Turkey, and Ukraine. The proposed vehicle would likely sit outside existing sovereign wealth funds and defence companies, mirroring specialised investment platforms such as MGX for AI. The discussions also align with the UAE’s broader strategy to localise defence production, reduce dependence on foreign suppliers, and position itself as a regional defence and technology hub. Existing efforts include the rapid expansion of EDGE Group, which has become the country’s largest weapons manufacturer and recently deepened partnerships with the US and South Korea firms in drones and cybersecurity.