To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil rises as fresh Hormuz attacks renew supply concerns. Oil prices edged higher, with Brent rising toward USD73/b and WTI above USD69/b, after renewed attacks on commercial vessels in the Strait of Hormuz highlighted persistent security risks despite ongoing US-Iran peace efforts. Shipping through the Strategic waterway has continued to recover but remains below pre-conflict levels, underscoring that geopolitical risks have not fully subsided. However, the upside in oil prices is likely to remain limited as Saudi Arabia has cut its August official selling prices, OPEC+ continues to unwind production cuts, Gulf exports are recovering, and the physical market remains well supplies, with Brent-Dubai spreads in contango signalling ample near-term supply. While isolated security incidents may trigger short-term price spikes, the broader outlook remains for relatively subdued oil prices as increasing supply and easing geopolitical risk premiums outweigh temporary disruptions.

Gold slips as Hormuz attacks revive inflation concerns. Gold prices declined for a second consecutive session, with gold falling to around USD4,125/oz, as renewed attacks on commercial vessels in the Strait of Hormuz pushed oil prices higher and revived concerns over inflation. The rise in energy prices increased expectations that central banks, particularly the Fed, could keep interest rates higher for longer, weighing on the non-yielding precious metal. However, losses were relatively limited as investors awaited the release of the Fed’s June meeting minutes for further guidance on the policy outlook, following weaker than expected US jobs data that recently reduced expectations for near-term rate hikes. Looking ahead, gold is likely to remain range-bound in the near term, with geopolitical tensions providing intermittent support, while the outlook for US monetary policy and inflation remains the key driver of prices.

MIDDLE EAST - CREDIT TRADING

End of day comment – 06 July 2026. Mixed day. Whilst activity was average, technicals are starting to play out across curves. That made for a wide distribution of price/spread changes across names/ curves. In general, long end bonds outperformed as cash prices moved a touch higher and UST continued to steepen, ADGB 49s last traded +0.25pt/-3bp on the day. Against this though short end and belly bonds are still not benefitting from the steeper UST curve as market makers are long and are trying to reduce. Closing this sector at best unch/+1bp. Recent new issues are trading weak, MASQUH perps last traded at 99.60 from 100 reoffer and RAKBNK 31s around 99.50 from 99.835 reoffer. In terms of flows sellers outnumbered buyers nearly 2:1. We saw EM dedicated RM in the afternoon selling the UAE names which got removed from the EM index, so it seems that selling flow has still some bonds to go. On the primary side Saudi Real Estate mandated a dual tranche sukuk and Ajman Bank a PNC 5.5y AT1 sukuk. (Source: Matthew Dunker, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

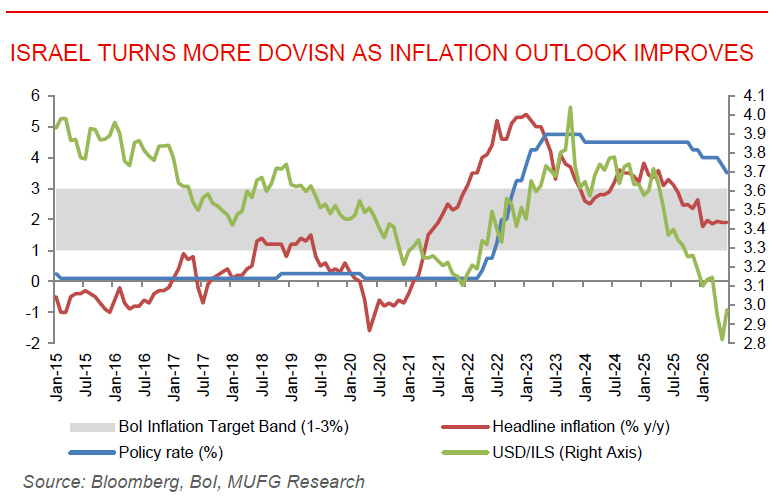

Bank of Israel cuts rates and signals further monetary easing. The Bank of Israel (BoI) lowered policy rate by 25bps to 3.5%, the lowest level since late 2022, marking its second consecutive rate cut as inflation eased to 1.9% in May, comfortably within the BoI’s ±2% target range. The BoI revised its 2026 GDP growth forecast up to 4% while lowering its 2026 inflation forecast to 1.8%, reflecting stronger than expected economic activity, softer energy prices, and improving inflation dynamics. It also expects the fiscal deficit to narrow to 4.9% of GDP in 2026, with public debt stabilising at 69% of GDP, and projects the policy rate to decline further to 3.0% by mid-2027 if inflation continues to ease. Governor Amir Yaron indicated that faster monetary easing would be justified should inflation expectations move closer to the lower end of the target range, although he emphasised that future policy decision will remain data-dependent. Overall BoI had adopted a more dovish stance as inflationary pressures recede and growth prospects improve, but renewed geopolitical tensions or higher than expected defence sending remain key risks that could delay the pact of policy easing.

IMF sees resilient growth but urges stronger reforms in Algeria. The IMF expects Algeria’s economy to grow by 3.8% in 2026, supported by higher hydrocarbon prices that are strengthening export and fiscal revenues, despite persistent fiscal and external vulnerabilities. While the fiscal deficit narrowed to 10.5% of GDP in 2025, public debt rose to 52.1% of GDP and international reserves declined due to weaker hydrocarbon exports and strong import growth driven by public investment. The IMF projects the current account deficit to narrow in 2026 as oil prices remain supportive, but warns that fiscal buffers have weakened and inflation could rise temporarily. The Fund called for continued structural reforms to diversify the economy, strengthen the private sector, an reduce dependence on hydrocarbons. Overall, the IMF views Algeria’s near-term outlook as positive, but stresses that sustained reforms will be essential to strengthen macroeconomic resilience, rebuild fiscal and external buffers, and support long-term private sector-led growth.