To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds steady as OPEC+ increases supply. Oil prices traded in a narrow range, with Brent below USD72/b and WTI near USD69/b, as continued recovery in shipping through the Strait of Hormuz and another planned OPEC+ production increase of 188,000b/d reinforced expectations of improving global supply. Saudi Arabia’s crude exports have already recovered close to pre-war levels, while the UAE has also restored exports, contributing to a looser physical market. Meanwhile, Brent and Dubai crude time spreads remained in contango, reflecting ample near-term supply, and Gulf producers are expected to lower official selling prices further to maintain competitiveness. Looking ahead, oil prices are likely to remain under downward pressure as Gulf exports normalise, OPEC+ gradually unwinds production cuts, and the geopolitical risk premium continues to fade. However, renewed disruptions in the Strait of Hormuz or setbacks in US-Iran negotiations remain key upside risks to prices.

Gold holds gain as Fed rate hike expectations ease. Gold prices held firm, with gold trading near USD4,160/oz, after posting its first weekly gain since May as weaker US jobs data and lower oil prices reduced expectations of further Fed rate hikes. The sharp decline in oil prices, driven by recovering flows through the Strait of Hormuz and higher OPEC+ supply, has eased inflationary pressures and improved the outlook for lower interest rates, providing support for the non-yielding metal. Meanwhile, renewed political pressure from President Trump to reshape the Fed has revived concerns over the central bank’s independence, continuing to underpin demand for gold as a hedge against policy uncertainty. Gold is likely to remain supported if expectations for tighter monetary policy continue to soften, although a stronger US dollar and further easing of geopolitical risks could limit upside potential.

MIDDLE EAST - MACRO / MARKETS

Turkey inflation eased as energy prices fall, but CBRT likely to stay cautious. Turkey’s annual inflation eased to 32.1% in June y/y from 32.6% in May y/y, marking the first slowdown since the outbreak of the Iran conflict, as lower energy prices following the partial normalisation of Strait of Hormuz flows and softer food inflation helped moderate price pressures. Monthly inflation also slowed to 1.0% from 1.7% in May, supporting expectations that inflation will gradually decline to around 30% by year-end, although still above the Central Bank of Turkey (CBRT)’s 26% forecast. Despite the improvement, inflation expectations remain elevated and underlying price pressures persist, suggesting the central bank is likely to keep its policy rate at 37%, while gradually reducing the effective funding rate from 40% back to 37% as market conditions normalise. Overall, the data indicate that Turkey’s disinflation process has resumed, but the pace is expected to remain gradual, with energy prices, domestic inflation expectations, and geopolitical developments in the Middle East remaining key risks to the outlook.

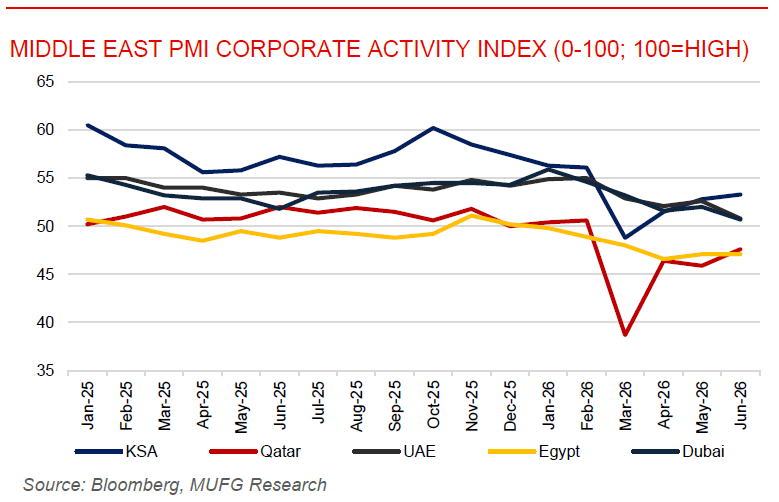

June PMI signals diverging momentum across the region. Saudi Arabia’s non-oil private sector strengthened in June, while Qatar showed tentative signs of stabilisation and Lebanon returned to modest expansion. Saudi Arabia’s PMI rose to 53.3 from 52.8 in May, reaching a four-month high as stronger domestic demand supported faster growth in new orders and business activity, although export orders remained weak and cost pressures stayed elevated. Qatar’s PMI improved to 47.6 from 45.9, also a four-month high, but remained below the 50 thresholds. Nevertheless, output stabilised after six straight months of decline, construction activity improved and business expectations strengthened, even as input-cost inflation accelerated. Meanwhile, Lebanon’s PMI increased to 50.3 from 49.7, moving back into expansion for the first time in four months as output and new orders recorded their strongest gains over the same period, pointing to a tentative improvement in private-sector conditions. Looking ahead, the near-term outlook remains uneven, with Saudi Arabia likely to retain the strongest momentum on the back of resilient domestic demand, while Qatar’s recovery will depend on a sustained improvement in new business and Lebanon’s expansion remains fragile given broader financial and structural constraints.

Iraq accelerates oil exports as Hormuz flows recover. Iraq is accelerating its crude exports as shipping through the Strait of Hormuz continues to normalise, improving access to key Asian markets following the US-Iran interim peace agreement. Iraq Basrah Medium and Basrah Heavy crude is increasingly being marketed on a delivered basis, making cargoes more attractive to refiners in South Korea, China, and other Asian markets while helping Iraq catch up with Gulf producers that have already restored exports close to pre-war levels. The improved logistics and greater availability of Iraqi barrels come as Middle Eastern producers compete more aggressively for market share through more flexible pricing, contributing to softer global oil prices. The recovery in Iraq’s exports marks another step toward the normalisation of Gulf oil supply, although the county still faces challenges in fully restoring production and exports while competing with Saudi Arabia, the UAE and other regional producers in an increasingly well-supplied Asian market.