To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds steady as Iran talks offset regional tensions. Oil prices stabilised after their first decline of the week, with Brent trading around USD95/b and WTI near USD93/b, as optimism over ongoing US-Iran negotiations balanced concerns over continued tensions in Lebanon. President Trump said discussions with Iran were progressing well and described efforts to end the conflict as being in their final stages, although no major break through has yet been announced. Markets remain focused on the prospect of reopening the Strait of Hormuz, a key route for global energy supplies, but uncertainty persists as Hezbollah rejected a US-backed ceasefire proposal and Israeli military operation continue in Lebanon. Additional support for prices came from reports of disruptions at Oman’s Mina Al Fahal export terminal, one of the few remaining Gulf oil loading points operating outside Hormuz. Despite recent gains, oil prices remain well below levels seen before the April ceasefire, reflecting continued uncertainty over the pace of any lasting regional resolution.

Gold heads for weekly loss as Iran talks stall and inflation risks persist. Gold fell below USD4,450/oz and was on track for a weekly decline of around 2%, as uncertainty surrounding US-Iran negotiations and renewed Middle East tensions weighed on sentiment. Despite President Trump stating that peace talks are in their final stages, Iranian officials indicated little progress has been made, while recent clashes involving Hezbollah, Kuwait, Bahrain, and US forces highlighted the fragility of regional stability. The prolonged disruption to energy flows through the Strait of Hormuz has kept oil prices elevated and inflation concerns alive, reinforcing expectations that central banks may keep interest rates higher for longer. This has continued to pressure non-yielding assets such as gold, which remains about 16% below its pre-conflict level.

MIDDLE EAST - CREDIT TRADING

End of day comment – 04 June 2026. The market was weak and felt heavy, especially in spread terms. Very few bonds are higher in cash price today, most are unchanged in price and some lower. Combined with the UST move that put spreads 3/4bp wider on average. Client flows were light, dealers are starting to cut out of risk. In the long end DUGB 50s was the underperformer today on street selling and closed -0.375pt/+6bp. Belly bonds underperformed long end in general though, ADGB 1.7 31s last cleared unch/+4bp vs ADGB long end +2bp. Quasi sovgn broadly followed sovgn moves. MUBAUH long end was underperforming with 49s closing -0.25pt/+4bp, ADNOUH 47s outperforming closing +0.125pt/+1bp. Fins were mixed, the market there remains very technical with some bonds like sukuks in general very well bid, but sellers in more liquid names like FABUH and AT1. On the corps side DPWDU had a bid today on the back of some Hormuz/ deal hopes after the Israel/Lebanon ceasefire. 49s closed +0.25pt/unch and 28s +0.125pt/unch. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

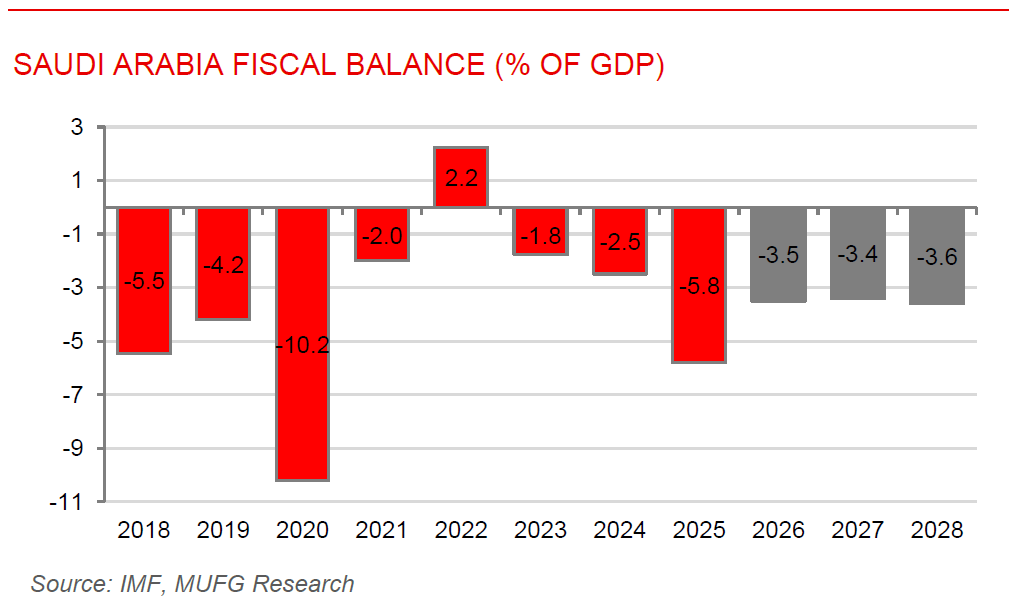

MF sees Saudi economy remaining resilient despite regional conflict. The IMF said Saudi Arabia’s economy remains resilient despite disruptions caused by the ongoing Middle East conflict, supported by strong fiscal buffers, diversified infrastructure, and continued progress under Vision 2030. After growing 4.5% in 2025, economic growth is expected to slow to around 2% in 2026 as reduced maritime traffic through the Strait of Hormuz weighs on both oil and non-oil activity. However, the Kingdom has mitigated the impact through alternative export routes, including the East-West pipeline and Red Sea ports, while strong government finances, ample reserves, and the Public Investment Fund provide important economic buffers. The IMF expects inflation to remain contained at around 2.3%, although higher shipping and insurance costs may add some upward pressure. Looking ahead, the Fund emphasised the important of maintaining fiscal discipline, advancing diversification reforms, and expanding private sector participation to strengthen long-term growth and resilience.

EBRD highlights diverging economic paths across non-GCC MENA. The EBRD’s latest Regional Economic Prospects report highlights increasingly divergent economic trends across non-GCC MENA economies amid ongoing regional tensions. Morocco and Egypt continue to show relative resilience, supported by strong tourism, remittance inflows, and reform-driven growth, while Morocco is expected to grow by 4.4% in 2026 despite a modest slowdown from 2025. Jordan and Tunisia are projected to maintain positive, albeit moderate, growth, although Tunisia continues to face fiscal and inflationary challenges. Lebanon’s economy is gradually recovering from a low base, while Iraq stands out as the region’s weakest performer, with lower oil production and export disruptions weighing heavily on growth and government revenues. The report underscores how countries with diversified sources of foreign currency earnings and stronger reform frameworks are proving more resilient, while economies more dependent on hydrocarbons or facing structural vulnerabilities remain exposed to ongoing geopolitical and trade disruptions.