To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil eases as Israel-Lebanon ceasefire raises hopes for wider de-escalation. Oil prices edged lower after three days of gains as Israel and Lebanon agreed to a ceasefire, potentially removing a key obstacle to broader US-Iran negotiations. Brent crude slipped toward USD97/b and WTI traded near USD96/b, although both remain sharply higher this week. Markets continue to focus on efforts to extend the US-Iran truce and reopen the Strait of Hormuz, but negotiations remain slow and sporadic flare-ups in regional tensions persist. Despite hopes for progress, Iran has warned of retaliation if attacks continue, underscoring the fragile security environment. Meanwhile, shrinking crude inventories and ongoing disruptions to flows through Hormuz continue to support prices, highlighting concerns that global supply buffers are becoming increasingly strained.

Gold gains as Israel-Lebanon ceasefire offers hope for de-escalation. Gold edged higher toward USD4,465/oz as investors bought on weakness following a conditional ceasefire agreement between Israel and Lebanon, which could support wider efforts to ease tensions across the Middle East. The agreement comes as the US and Iran continue negotiations on extending their truce and reopening the Strait of Hormuz, although a final deal remains elusive. While hopes of de-escalation have improved sentiment, ongoing uncertainty around energy flows through Hormuz continues to support oil prices and sustain inflation concerns. These pressures could keep major central banks cautious on interest rates, limiting upside for non-yielding assets such as gold. Despite the recent rebound, gold remains around 16% below its pre-conflict level as markets continue to balance geopolitical risks against the prospect of higher-for-longer interest rates.

MIDDLE EAST - CREDIT TRADING

End of day comment – 03 June 2026. Weaker risk sentiment today. Overnight US/Iran traded fire and oil was up/ UST down on the Kuwait airport attack. That set the tone for much of the day. Activity dropped meaningfully as buyers stepped aside and the street was reluctant to bid bonds. The main sovgn names close 1/2bp wider. ADGB had sellers across the curve again, mainly in 34s today which closed -0.375pt/+2bp. Long end bonds were offered down in ADGB and QATAR, but there was an element of shorts offering down on a weaker day, not many bonds traded, QATAR 46s closed -0.5pt/+2bp. MOROC also gave back some of the strength we had seen lately, 50s closing -0.75pt/+5bp. Fins again had a quiet day, FABUH 4.299 31s saw some early trades closing -0.20pt/+1bp. Quasi sovereign mirrored sovgn moves with afternoon trades in MUBAUH and QPETRO. Whilst oil is coming off into the close, UST hover around the lows and credit indices at the wides, GCC will need better news to hold the recent spread tightening we have seen. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

GCC anchors regional M&A activity despite geopolitical headwinds. According to Ansarada’s Middle East M&A Market Analysis report, Middle East M&A activity remained relatively resilient in Q1 2026, with 196 announced deals worth USD23.3bn, despite a decline from USD31.3bn a year earlier amid ongoing geopolitical tensions. Saudi Arabia was among the strongest performers, recording 24 deals and modest growth in transaction volume, supported by Vision 2030 initiatives and continued investment activity from the Public Investment Fund (PIF). The UAE remained a key regional hub with 33 deals worth USD2.2bn, although investors adopted a more selective approach to capital deployment. Transportation led deal value, while technology remained the most active sector by volume, followed by energy, healthcare, and industrials. Looking ahead, a robust pipeline of privatisations, IPOs, and sovereign-backed investments across the GCC is expected to support a recovery in deal activity during the second half of 2026, reinforcing the region’s appeal as a destination for long-term capital and strategic investment.

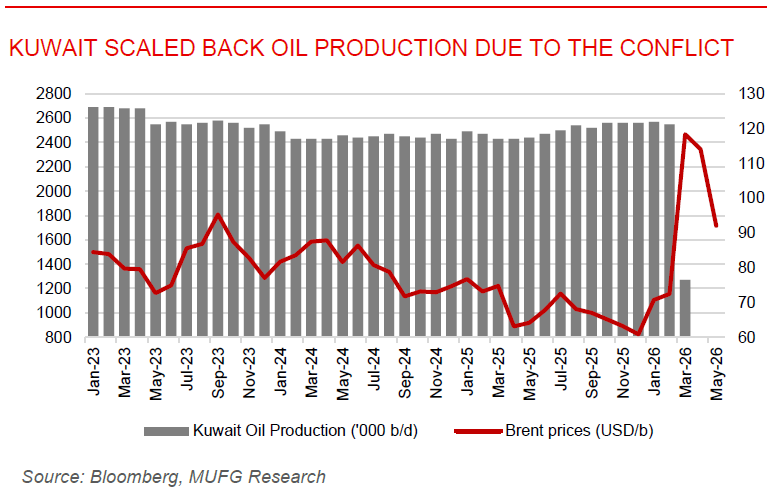

Kuwait explores alternative export routes as Hormuz risks persist. Kuwait is considering expanding its overseas oil storage capacity and exploring alternative export routes following the disruption to energy flows through the Strait of Hormuz. According to Kuwait Petroleum Corporation, the waterway remains unsafe for energy shipments despite not being fully blocked, prompting discussions with neighbouring countries on potential pipeline solutions and increased storage arrangements abroad. As Kuwait relies entirely on Hormuz for crude exports, the conflict has forced the country to scale back oil production while maintaining minimum operational levels to preserve field integrity. The move highlights growing concerns among Gulf producers about the long-term reliability of Hormuz as a key export corridor. While Kuwait continues to supply some refined products within the Gulf, authorities estimate crude production could return to around 70% of normal levels within two months of Hormuz reopening, with refinery operations expected to normalize within weeks.