To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds steady as Hormuz flows continue to recover. Oil prices were broadly stable, with Brent trading around USD72/b and WTI near USD69/b, as increasing flows through the Strait of Hormuz and ongoing US-Iran negotiations continued to ease supply concerns. Saudi crude exports have recovered to around 90% of pre-war levels, while Brent’s prompt spread remained in contango, signalling ample near-term supply. Although diplomatic discussions have made progress toward a long-term agreement, key issues, including Iran’s nuclear program, the future governance of Hormuz, and potential transit fees-remain unresolved and could delay a comprehensive peace deal meanwhile, the recovery in Gulf exports, together with rising oil volumes of Iranian oil held offshore, continues to add to short-term supply. Going forward, oil prices are likely to remain range-bound to slightly weaker as regionals supply continues to recover and geopolitical risk premiums fade, although unresolved diplomatic issues could still generate intermittent market volatility.

Gold rises as weak US jobs data eases rate hike expectations. Gold prices extended their gains, rising to around USD4,195/oz, after weaker-than-expected US jobs data reduced expectations of a Fed rate hike. Investors lowered the probability of a July rate increase as softer labour market conditions eased concerns over further monetary tightening, providing support for the non-yielding metal. Gold also benefited from renewed concerns over the Fed’s independence amid President Trump’s continued criticism of the central bank, while lower oil prices and easing geopolitical tensions following progress in US-Iran talks helped moderate inflation expectations. Gold is likely to remain supported if expectations for further Fed tightening continue to fade, although improving geopolitical conditions could limit further upside.

MIDDLE EAST - CREDIT TRADING

End of day comment – 02 July 2026. Short end bonds moved wider lagging the rates moves across almost all sectors. Otherwise, most IG curves were unchanged in spreads while BHRAIN continues to tick wider and TURKIYE widened a touch. ETB/arb account flows have remained thin while real money has been largely inactive with fast money and the street kicking around newish bonds amongst themselves. For KSA/KUWIB, recent days seem to have lifted the hangover in the newly issued PIFKSA bonds with the 4⅞% 29s levelling out with the rest of the curve, a local cleaning up the PIFKSA 33s, and one dealer gobbling up the free float on the PIFKSA 56s. Those 29s are going out -2bps with the rest of the curve mostly unchanged. There was demand for 34s and 35s in the am. KSA Sov volumes were muted while trading was focused on squaring positions acquired yesterday in the 10-year sector. Small amounts of T2 traded, with us selling our SNBAB 6 35 axe and the street chasing to cover a short in SABBAB 35s. (Source: Matthew Dunker, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

UAE non-oil growth slows amid regional uncertainty. The UAE’s non-oil private sector expanded at its slowest pace in over five years in June, with the PMI falling to 50.8 from 52.6 in May, while Dubai’s PMI declined to 50.7, its weakest reading since January 2021. Regional geopolitical tensions continued to weigh on client activity, tourism, and business confidence, resulting in softer new order growth and the first decline in employment in more than four years, with job losses accelerating to their fastest pace since August 2020. Businesses also faced higher transportation and commodity costs, leading to a further squeeze on profit margins as input cost inflation outpaced selling price increases. On a more positive note, supply chain conditions improved as shipping disruptions through the Strait of Hormuz eased, shortening delivery times, while resilient domestic demand, government investment, construction activity, and digital services continued to provide support. Overall, the data point to a moderation rather than a contraction in the UAE’s non-oil economy, with easing geopolitical tensions and improving logistics expected to support a gradual recovery in business activity during H2 2026.

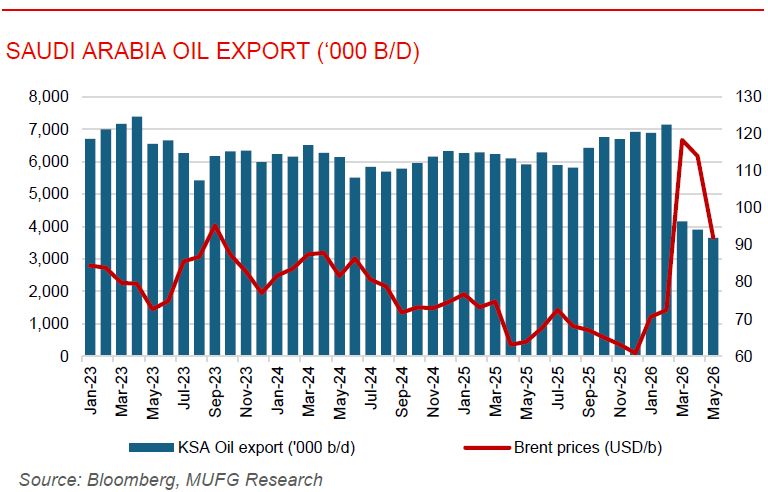

Saudi oil exports rebound as Hormuz traffic normalises. Saudi Arabia’s crude oil exports have rebounded to near pre-war levels, averaging 6.3mb/d over the six days through Wednesday, close to the KSA’s 2025 average and ~90% of February levels, as tanker traffic through the Strait of Hormuz continues to normalise following the US-Iran interim peace agreement. The recovery has been driven by increased loadings from Ras Tanura, continued exports via the East-West Pipeline to Yanbu on the Red Sea, and a growing number of Bahri-operated tankers successfully transiting Hormuz. Aramco has also increased spot crude sales to Asian customers, while additional tanker chartering suggests exports could rise further in the coming weeks. The rapid recovery in Saudi exports, alongside the UAE’s return to pre-conflict export levels, highlights the normalisation of Gulf oil supply and the continued unwinding of the geopolitical risk premium that had supported oil prices.