To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil holds gains as uncertainty over US-Iran talks supports prices. Oil prices steadied after posting their strongest daily gain in about a month, as uncertainty surrounding US-Iran negotiations raised concerns that disruptions to energy flows from the Persian Gulf could persist. Brent crude traded below USD95/b and WTI near USD92/b after markets reacted to conflicting signals over the status of talks, including reports that Iran had suspended negotiations before President Trump later stated discussions were still ongoing. Trump said a MoU to reopen the Strait of Hormuz could be reached within a week, although key issues remain unresolved. Markets are also monitoring reports that Iran and its regional allies are considering further restrictions on both the Strait of Hormuz and the Bab el-Mandeb Strait. With commercial traffic through Hormuz still constrained and geopolitical tensions extending to Lebanon, investors remain focused on the risk of prolonged supply disruptions in a region that normally handles around one-fifth of global oil and LNG trade.

Gold remains under pressure as Iran talks uncertainty sustains inflation concerns. Gold traded near USD4,490/oz, as conflicting signals from the US and Iran clouded prospects for a diplomatic resolution to the conflict. While President Trump said negotiations were continuing at a rapid pace, reports of renewed tensions around the Strait of Hormuz and mixed messages on regional developments kept markets uncertain. The ongoing risk of prolonged energy supply disruptions has strengthened the US dollar and pushed bond yields higher, all of which have weighed on gold. Gold remains about 15% below its pre-war level, as investors balance geopolitical risks against expectations that persistent inflation and resilient US economic data could delay interest-rate cuts.

MIDDLE EAST - CREDIT TRADING

End of day comment – 01 June 2026. Weak prices and sentiment, tighter spreads. Activity picked up substantially today after last week’s holiday. The morning was firm as cash bids held in light of UST weakness/ oil strength with no resolution over the weekend. Spreads were 3/5bp tighter. Then Iran suspended negotiations with the US and threatened to close the Strait of Hormuz which led to more oil strength/ UST weakness. This time cash adjusted to the left as sellers woke up. We still going out tighter in spreads, but the market has a weak feel and flows have flipped firmly from buyer to seller-initiated trades. most curves are closing -0.25pt/-0.75pt and anywhere from -3bp in the belly to +1bp in the long end in spread terms. The one credit which outperformed today was MOROC, which had a strong bid in the morning and held better in the afternoon sell off. The curve closes up to -0.25pt and up to -5bp with a strong bid in new 38s EUR and long end USD (50s unch/-5bp). Seeing more selling into the close in higher beta credits.

MIDDLE EAST - MACRO / MARKETS

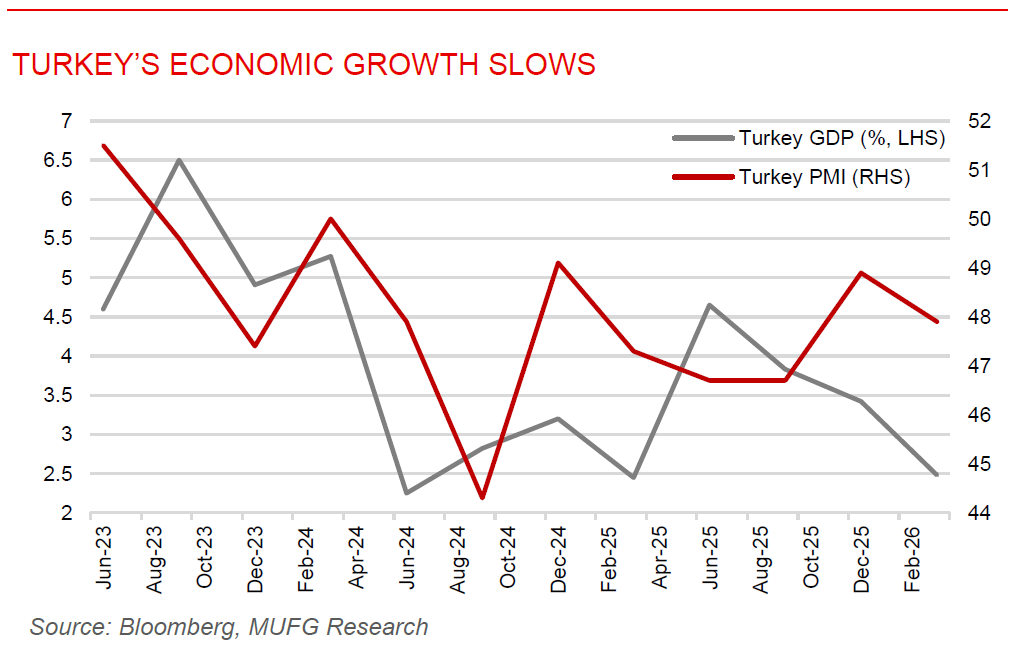

Turkey’s economic growth slows as tight policy and war risks weigh. Turkey’s economy expanded by 2.5% y/y in Q1 2026 from 3.4% y/y in Q4 2025, marking a notable slowdown as higher interest rates and regional tensions weighed on activity. The weaker performance reflects the impact of the central bank’s tighter monetary stance, adopted to stabilise markets and contain inflationary pressures stemming from the Iran war, which has pushed up energy costs for the import-dependent economy. Inflation remains elevated, prompting the central bank to raise its year-end inflation forecast to 24% and fuelling expectations that rates could remain higher for longer. Despite the softer GDP data, there were encouraging signs from the manufacturing sector, with the PMI rising to 49.8 in May, its strongest reading since March 2024, supported by a recovery in export demand and a modest increase in production. However, rising input costs, supply-chain disruptions, and ongoing geopolitical uncertainty continue to weigh on business sentiment, suggesting Turkey’s growth outlook will remain closely tied to inflation dynamics, energy prices, and future monetary policy decisions.

Jordan’s exports grow as trade deficit improves in Q1 2026. Jordan’s national exports rose by 1.6% y/y to JOD2.13bn (USD3bn) in the Q1 2026, reflecting steady progress in the country’s efforts to boost export-led growth under its Economic Modernization Vision. While re-exports declined by 7.1% to JOD561 million, lower imports, down 2.9% to JOD 4.6bn, helped narrow the trade deficit by 6.3% to JOD 1.9bn. As a result, total exports remained broadly stable at JOD 2.69bn, only slightly lower than a year earlier. The trade data highlight the resilience of Jordan’s external sector despite ongoing regional uncertainty and challenging global conditions. The performance also comes against a backdrop of relative macroeconomic stability, supported by fiscal and structural reforms, with S&P recently affirming Jordan’s ‘BB-’ rating and stable outlook. While Jordan’s credit profile remains below that of wealthier Gulf economies, the latest figures suggest gradual improvement in trade dynamics and continued progress toward strengthening the country’s economic fundamentals.