To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil declines as Hormuz flows recover. Oil prices extended their losses, with Brent trading below USD71/b and WTI around USD68/b, as increasing flows through the Strait of Hormuz and signs of progress in indirect US-Iran negotiations continued to ease supply concerns. Oil shipments through the waterway have recovered to over 10mb/d, while UAE exports have returned to pre-war levels, reinforcing expectations of improving regional supply. However, key issues, including Iran’s nuclear program and its insistence on overseeing shipping through Hormuz, remain unresolved, suggesting negotiations could be prolonged despite constructive diplomatic signals. Oil prices are likely to remain under downward pressure as supply continues to normalise and geopolitical risk premiums unwind, although setbacks in negotiations or renewed security incidents could still trigger periods of volatility.

Gold rebounds as Fed eases rate hike concerns. Gold prices extended their rebound, with gold rising to around USD4,066/oz, after Fed Chair Kevin Warsh delivered a less hawkish-than-expected message, easing expectations of further rate hikes this year. While Warsh reaffirmed the Fed’s commitment to returning inflation to its 2% target, his comments reduced immediate tightening concerns and supported demand for gold. Meanwhile, mixed US economic data, including slower manufacturing growth but resilient private sector hiring, kept markets focused on upcoming payrolls data for further clues on the Fed’s policy path. Gold could find near-term support if expectations for additional rate hikes continue to soften, although persistent inflation and a resilient US economy are likely to limit upside potential.

MIDDLE EAST - CREDIT TRADING

End of day comment – 01 July 2026. The start of the month was greeted with a pronounced weakness in UST overnight. Cash prices adjusted to the left. Early afternoon around Warsh's comments and ISM numbers UST began a recovery with a steepening bias. However, cash didn't follow, and spreads continued to widen out. In terms of flows the month end selling was visible in the early part of the day, accounts and dealers tried to sell what was sold yday. Into the close seeing small ETFs inflows and some international and local retail buying which is starting to lift prices a touch. At eod the market is on average 3bp wider with the distribution from unch to +5bp. Long end bonds are up -1pt and +2/3bp, belly and short end -0.125/-0.25pt and +3/5bp. The UAE complex is still an underperformer post index removal. In sovgn mainly the ADGB curve, in quasis mainly MUBUAH. Newly issued RAKBNK 31s and MASQUH 6.625 perps traded 0.125 to 0.25pt below reoffer in the morning and remained there in the afternoon. The market is going out with a weak feel, the underlying rates move has thrown another layer of weakness into a market which is positioned long. NFP next ahead of the long weekend tomorrow. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

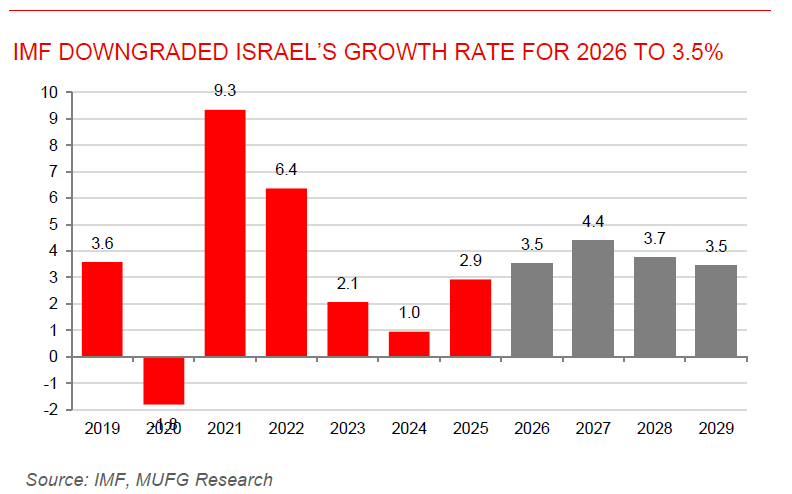

IMF downgraded Israel growth as regional conflict weighs on outlook. The IMF expects Israel’s economy to remain resilient but significantly affected by the ongoing Middle East conflict, lowering its 2026 GDP growth forecast to 3.5% from 4.8% before the war. Elevated defence spending, labour shortages due to military mobilisation and reduced foreign workers, and higher energy prices are expected to keep inflation temporarily elevated and widen fiscal deficits, with public debt projected to rise above 70% of GDP. While the banking sector remains well-capitalised and financial markets have stabilised, the IMF recommends maintaining a moderately tight monetary policy, implementing gradual fiscal consolidation through revenue measures, and accelerating structural reforms to boost labour participation, infrastructure, and AI competitiveness. The Fund notes that downside risks remain dominated by renewed regional escalation, while a durable peace and broader regional integration could provide meaningful upside through stronger trade, investment, and economic growth.

Turkey’s manufacturing contraction deepens in June. Turkey manufacturing sector weakened in June, with the PMI falling to 47.1 from 49.8 in May, returning to contraction as geopolitical uncertainty from the Middle East conflict weighed on business activity. Output, new orders, and export demand all declined, prompting manufacturers to scale back purchasing activity, inventories, and employment, extending the sector’s downturn to 27 consecutive months. At the same time, input cost and output price inflation continued to moderate, reaching their lowest levels in several months, offering some relief from cost pressures. Overall, the data suggests that softer domestic and external demand, coupled with regional uncertainty, continues to weigh on Turkey’s manufacturing sector, although easing inflation could provide a more supportive backdrop if market conditions stabilise in the second half of 2026.