To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil stabilises as markets monitor US-Iran talks. Oil prices stabilised, with Brent trading above USD73/b and WTI near USD70/b, after recording their sharpest quarterly decline since the pandemic as improving prospects for a lasting US-Iran agreement continued to ease supply concerns. Progress in indirect negotiations has supported a gradual recovery in shipping through the Strait of Hormuz, while Iranian exports have increased following the easing of maritime restrictions and Russian crude shipments have also risen, adding to global supply. However, uncertainty remains over key issues, including Iran’s nuclear program and future governance of the Strait of Hormuz, which could complicate negotiations during the ongoing ceasefire period. Oil prices are likely to remain under downward pressure as supply continues to recover and geopolitical risk premiums fade, although setbacks in negotiations or renewed disruptions to Hormuz could trigger short-term price volatility.

Gold extends decline on hawkish Fed outlook. Gold prices extended their losses, with gold falling below USD3,980/oz to its lowest level since November, as expectations for higher US interest rates continued to weigh on investor sentiment. Comments from Fed officials reinforced the possibility of further policy tightening, while resilient US labour market data supported the case for keeping rates higher for longer. Meanwhile, progress in US-Iran peace talks continued to reduce geopolitical risk premiums, further dampening demand for safe haven assets. Gold is likely to remain under pressure in the near term as higher for longer rate expectations and easing geopolitical tensions outweigh safe haven demand, although any setback is diplomacy or signs of slowing US economic activity could provide support for prices.

MIDDLE EAST - CREDIT TRADING

End of day comment – 30 June 2026. The morning was very constructive as bonds which recently widened most got bid up. That spanned from MUBAUH short end to ADGB long end and cash was 0.25/0.5pt higher with spreads up to 5bp tighter. Late morning though the month end outflows started and more RM started selling in the afternoon into month end. With UST selling off dealers moved cash to the left and spreads gradually widened. At eod the market feels heavy again. ADGB closed up to 0.25pt lower and up to 3bp tighter. QATAR showed the same move with far less activity. In the quasi space MUBAUH was most active across the curve but gave up all early morning cash price gains to close broadly unch/-2bp. Sentiment has overall improved over the last 2 sessions. However, month end outflows were probably a bit bigger than expected today, so the market will be looking if outflows persist in the new month and whether dealers will want to lighten books ahead of NFP/ long holiday weekend. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

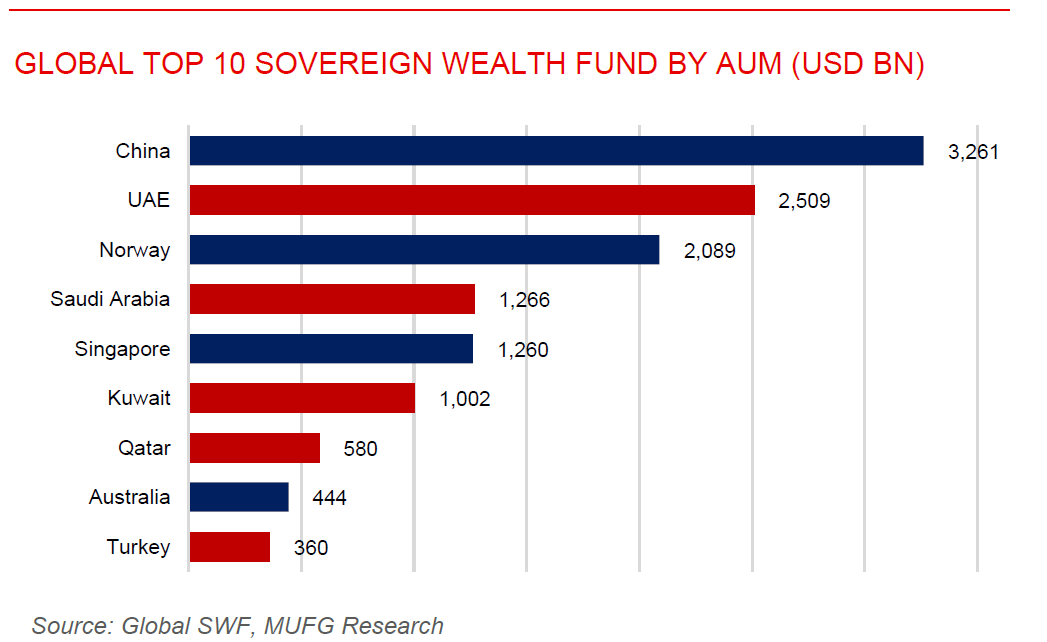

PIF assets reach USD1.2 trillion as diversification drive accelerates. Saudi Arabia’s Public Investment Fund (PIF) increased its total assets to SAR4.54 trillion (USD1.21trillion) at the end of 2025, up 5.1% y/y, while gross revenue rose 9% to SAR449.9bn and net profit more than doubled to SAR65.1bn, supported by stronger operating performance. The fund also maintained a robust liquidity position with over SAR350bn in cash and cash equivalents, providing ample capacity to pursue its investment strategy. During 2025, PIF expanded its strategic initiatives by launching the AI company Humain, establishing Expo 2030 Riyadh Co., forming new partnerships with global asset managers, and diversifying its funding sources through its inaugural EUR1.65bn green bond and commercial paper programme. The strong financial performance underscores PIF’s growing role as the key driver of Saudi Arabia’s Vision 2030 agenda, supporting economic diversification, capital market development, and investment across strategic sectors.

Saudi’s current account returns to surplus in Q1, while reserves ease in May. Saudi Arabia’s current account returned to a surplus of USD4.1bn in Q1 2026, reversing from a USD8.2bn deficit in Q4 2025 and improving from a USD2.8bn deficit in Q1 2025, according to data published by the Saudi Central Bank. The improvement was mainly supported by stronger goods surplus, which widened to USD30.1bn from USD21.4bn a year earlier, while the services deficit narrowed slightly to USD10.7bn. However, workers’ remittances abroad increased to USD17.3bn, highlighting continued outward income flows. On the financial account side, the deficit narrowed to USD960mn, compared with USD9.9bn a year earlier, while net direct investment recorded a surplus of USD1.7bn. Separately, SAMA data showed Saudi Arabia’s official reserve assets declined by SAR24.8bn, or 1.3% m/m, to SAR1.83 trillion in May, although reserves remained 6.4% higher y/y. Overall, the data point to an improvement in Saudi Arabia’s external position in Q1, although the monthly decline in reserve assets suggests that external buffers should continue to be monitored closely.