Macro focus – France’s 2027 presidential race starts to take shape: Marine Le Pen’s eligibility to contest the 2027 presidential election as the National Rally candidate has pushed the event into sharper focus. Polling suggests that Le Pen is on course to reach the second round and ultimately has a plausible path to the Élysée. The composition of the next parliament may matter as much as the presidential result after an extended period of fragmentation and drift. For investors, the key questions are around fiscal policy, reform prospects and France’s relationship with the EU. Meanwhile, in the UK, Nigel Farage’s decision to trigger a by-election has generated plenty of political headlines. The market implications are minimal unless it leads to weaker momentum for his Reform party and raises the temptation for incoming PM Burnham to trigger a snap general election.

What we’re watching next week: It’s a relatively light European data schedule next week with highlights being euro area industrial production and the final HICP release, as well as UK monthly GDP for May. We will also be watching appearances from central bank officials particularly closely after re-escalation between the US and Iran and the subsequent rise in energy pricing. The ECB’s Schnabel and BoE Governor Bailey are set to make speeches ahead of their respective upcoming policy meetings.

French 2027 presidential election moves into focus

Marine Le Pen is back in the race – and could plausibly win

There has been no shortage of political drama in Europe this week. The most consequential development came in France. An appeals court upheld Marine Le Pen’s conviction for misuse of European parliament funds but significantly reduced the period of ineligibility from five years to 15 months, which has already been served. This cleared the National Rally (RN) leader to stand in next year’s presidential elections (the first round of which will be held on 18 April 2027). Le Pen confirmed her intention to stand.

The ruling has increased the focus on what has long been viewed as a key political risk event in Europe. Until this week, our assumption had been that Le Pen’s electoral ban meant that Jordan Bardella, Le Pen’s 30-year old protégé, would be the RN candidate for president. Some polling had suggested that Bardella could actually be the stronger electoral prospect. But RN has quickly pivoted to a joint-ticket approach with Le Pen as the presidential candidate and Bardella as the prospective prime minister. On paper this arrangement could allow RN to combine Le Pen’s experience with Bardella’s stronger appeal among younger and more moderate voters.

It’s worth mentioning that Le Pen’s legal issues have not completely disappeared. The court maintained the conviction and imposed a custodial sentence which could ultimately involve monitoring with an electronic tag. Le Pen has stated that she will appeal, meaning the sentence will be suspended during the process. If a final ruling is delivered before the election Le Pen could face the logistical challenges associated with electronic monitoring during the final phase of the campaign.

But from a political perspective, the decision has removed uncertainty around RN’s candidate and arguably strengthened Le Pen, who has again shown she can survive setbacks. Polls conducted after she announced her intention to run show Le Pen well on course to reach the second round under France’s two-round electoral system with around 35% of the vote. More significantly, she currently has a narrow lead in run-off scenarios over the next-best candidate, centre-right former PM Édouard Philippe. Toluna Harris (here) puts it at 51-49, and Ifop (here) at 54-46. Other scenarios show Le Pen beating Gabriel Attal (another ex-PM and member of Macron’s Renaissance party) with a slightly larger margin.

We see bot Philippe and Attal as essentially interchangeable from a market perspective – both pro-Europe, in favour of structural reform and fiscally orthodox. A run-off between Le Pen and hard-left veteran Jean-Luc Mélenchon, both Eurosceptic and unorthodox, is the more feared scenario. Mélenchon has never progressed beyond the first round and is polling around 15% but could plausibly advance if support for candidates from the centre is fragmented. On current polling, Le Pen comfortably beats Mélenchon in the second round.

It is already a crowded field and other candidates may yet emerge. Being a front-runner at this stage is no guarantee of victory. Looking back to the April 2017 election, Macron was initially seen as an interesting outsider, and he did not formally announce his presidential candidacy until November 2016. But looking across the current polling, an RN presidency is certainly plausible. Polymarket gives a combined implied probability of around 33% for Le Pen or Bardella to be next French president.

French political risk set to move into sharper market focus

There is uncertainty around RN’s policy platform but, broadly speaking, the prospect of an RN administration is somewhat less troubling for investors than would have been the case in years gone by. RN has gradually moderated its positions, abandoning calls to leave the euro or hold a referendum on EU membership. Instead the argument now is to reform the EU from within. There is an obvious parallel with Giorgia Meloni's trajectory in Italy. She moderated her policy platform, placing greater emphasis on immigration and security issues while looking to avoid policies that could unsettle markets in a fiscally-constrained environment.

Investors would certainly hope for the same approach if Le Pen were to secure the French presidency. France comes into the campaign period with weak growth, a divided parliament and limited capacity to deliver any meaningful fiscal consolidation. Public debt is approaching 120% of GDP and the state auditor has said that a credible plan to reduce this burden is required as interest costs “suffocate” public finances. The fiscal deficit widened to 5.1% of GDP in 2025 and is likely to deteriorate slightly in 2026. The government has cut its annual growth forecast from 0.9% to 0.7% (matching our forecast), reflecting both the Iran conflict and consequences of political uncertainty around the budget.

Indeed, the parliamentary election, which a new president would surely call, is arguably as important as the presidential one. France has had to deal with legislative logjam and has seen five PM since Macron’s ill-fated decision to call a snap election in 2024. Polling for the National Assembly is limited at this stage but based on first-round presidential preferences it’s far from clear that any group will be able to secure a workable majority at the next election. That would mean a lack of meaningful reform, fiscal or otherwise, and frozen agendas more broadly. RN’s position on pension reform, the most significant fiscal challenge, remains unclear.

In terms of some joint scenarios, a Philippe (or similar profile) presidency and a centrist majority in the national assembly would raise fiscal reform hopes and be the most market-friendly. A Le Pen presidency with cohabitation (i.e. a centrist/left PM) would see the RN platform constrained but would likely mean a continuation of policy drift. A Le Pen presidency and RN parliamentary majority would raise fears of fiscal loosening and more EU friction, and likely cause OAT-Bund spreads to widen.

For now, the focus turns to the draft 2027 budget which will be prepared over the summer and presented to parliament in the autumn before a vote in December. In both 2024 and 2025 the usual process failed and a special law was initially required as a stopgap to roll-over the previous framework. It’s hard to see much appetite for compromise or indeed tax rises ahead of the presidential election – and there’s plenty of risk that will remain the case after it as well.

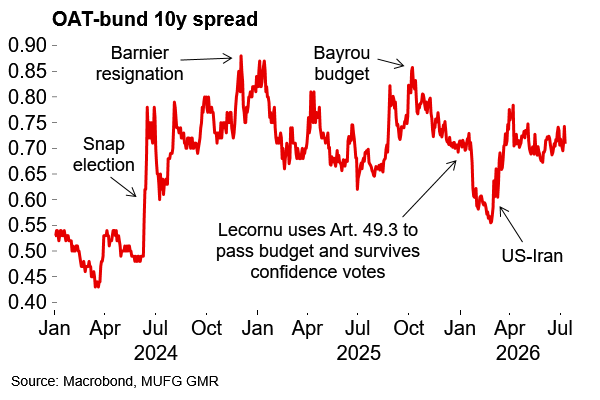

Markets have priced in a persistent political risk premium

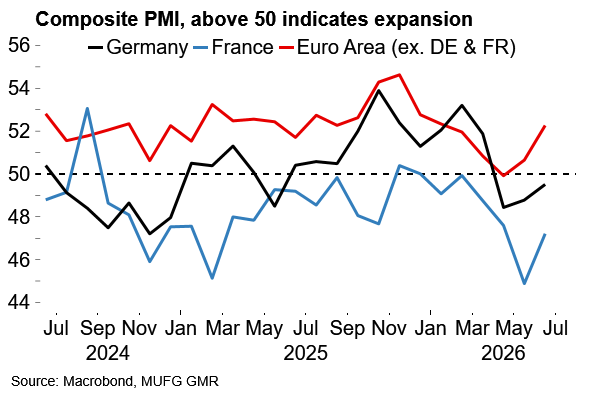

French business sentiment has trailed that of EZ peers

Can Nigel Farage control the narrative?

Meanwhile, another prominent Eurosceptic politician was making news across the Channel in the UK. On the same day as the Le Pen ruling, Nigel Farage delivered the surprise announcement that he would resign as MP but then immediately contest the resulting by-election, which will be held on 13 August. The move comes as UK parliamentary authorities investigate allegations surrounding the declaration of donations and financial support from wealthy backers.

Farage denies wrongdoing and argues that he is being targeted by the political establishment. His resignation seems to be an attempt to seize control of the narrative. However, all other major political parties have refused to participate in the by-election. That means some political theatre of Farage versus an assortment of colourful independents rather than a meaningful electoral test. Farage is heavily favoured to regain his seat (with ~90% implied probability on prediction markets).

The most important question for us is whether the episode damages Farage's personal standing and, by extension, the momentum of his Reform UK party. Reform continue to lead national polls but have faded a little since last autumn, and continued focus on Farage’s finances might become more of a headwind. If a clearer trend emerges then the temptation could increase for incoming PM Burnham to hold a snap election. Otherwise, the story is just political noise and the market implications seem negligible.

What we’re watching next week

Central bank speakers in focus after US-Iran re-escalation

It’s a relatively light European data schedule next week with highlights being the euro area industrial production and final HICP releases, as well as UK monthly GDP for May. The HICP numbers will provide a bit more detail on underlying inflation rivers after the below-consensus headline print of 2.8% in June. We expect UK GDP to have edged higher, boosted by warm weather, leaving the Q2 average rate at 0.2% Q/Q in the absence of revisions.

We will also be watching appearances from central bank officials particularly closely after following re-escalation between the US and Iran and subsequent rise in energy pricing. Influential ECB hawk Isabel Schnabel is set to speak before the quiet period ahead of the 23 July meeting. BoE governor Andrew Bailey is also set to speak at Mansion House on Tuesday. We continue to expect a final ECB hike in September but dropped our call for BoE tightening after officials showed little sign of urgency to raise rates amid soft UK data and retracing energy prices.

Key data releases and events (week commencing Monday 13 July)

Day | Time | Region | Event | Period | Consensus | MUFG | Previous |

Mon 13 Jul | 17:45 | EC | ECB's Schnabel Speaks | - | - | - | - |

Tue 14 Jul | 21:00 | UK | BOE Governor Bailey speaks at Mansion House | - | - | - | - |

Wed 15 Jul | 10:00 | EC | Industrial Production SA MoM | May | 0.3 | 0.5 | 0.1 |

Thu 16 Jul | 7:00 | UK | Monthly GDP (MoM) | May | 0.1 | 0.2 | -0.1 |

16 Jul-22 Jul |

| EC | ECB's Pre-Rate Decision Quiet Period | Jul | - | - | - |

Fri 17 Jul | 10:00 | EC | CPI YoY | Jun F | 2.8 | 2.8 | 2.8 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR