Key Points

Upward momentum in USDSGD has been building recently, amid higher US yields and uncertainty around US-Iran negotiation. But we expect SGD to remain resilient against both USD and regional peers. MAS policy provides a strong anchor. A steeper S$NEER slope (est. ~1% pa) reinforces an appreciation bias. USDSGD volatility has been contained, and any near-term upside in USDSGD is likely capped by strong technical resistance around the 1.2900 level in my view.

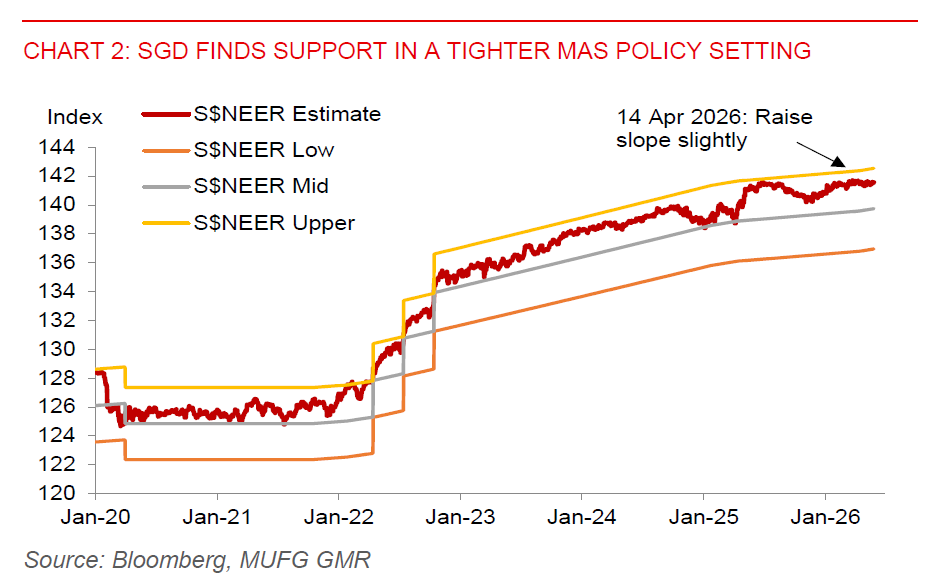

Singapore’s headline inflation remains contained at 1.8%yoy in April, while MAS has signalled that the monetary policy stance is appropriate. This suggests MAS could be on hold in July meeting. Nevertheless, we expect S$NEER to remain in the upper half of the band. Our $SNEER estimate is currently about 0.7% below the upper policy band, leaving room for SGD resilience or even outperformance should external conditions improve. Meanwhile, inflation risks continue to linger.

Singapore’s growth and external buffers remain supportive of SGD. Q1 GDP growth was 6%yoy, industrial production rose 17.6%yoy in April, and export momentum has accelerated since February, led by electronics. Singapore’s large current account surplus (>17% of GDP) and resilient bond inflows, driven by safe-haven demand, further provide a strong buffer against external shocks.

Energy diversification is crucial in mitigating near-term supply risk. Singapore’s natural gas import sources are well diversified, with no single country accounting for more than 30% of its gas imports. Medium-term investments, including a second LNG terminal (set to be operational by 2030) and ongoing expansion in renewable energy capacity, should enhance energy resilience.

Key downside risks to SGD stem from US rates and geopolitics. First, higher US yields continue to underpin USD strength, limiting SGD upside. Second, a prolonged Hormuz disruption that triggers a global energy crunch would pose a significant downside risk, given Singapore’s heavy reliance on imported natural gas for 95% of electricity generation. A surge in oil and gas prices have also raised import costs and weakened the terms of trade.

On rates, we forecast SORA 3-month compounded at 1.15% in Q2, 1.30% in Q3, 1.36% in Q4, and 1.40% in Q1 2027. While MAS tightened policy in April, market expectations for Fed hikes and higher US yields could dominate, implying limited downside in SORA. Meanwhile, SORA could gradually normalise relative to US rates.