Please download PDF from above for the following currencies.

Australian dollar // New Zealand dollar //Canadian dollar // Norwegian krone // Swedish Krona // Swiss franc // Czech koruna // Hungarian forint //Polish zloty // Romanian leu // Russian rouble // South African rand // Turkish lira // Indian rupee // Indonesian rupiah // Malaysian ringgit // Philippine peso //Singapore dollar // South Korean won // Taiwan dollar // Thai baht // Vietnamese dong // Argentine peso // Brazilian real // Chilean peso // Mexican peso // Saudi riyal // Egyptian pound

Monthly Foreign Exchange Outlook

DEREK HALPENNY

Head of Research, Global Markets EMEA and International Securities

Global Markets Research

Global Markets Division for EMEA

E: derek.halpenny@uk.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

E: lee.hardman@uk.mufg.jp

LIN LI

Head of Global Markets Research Asia

Global Markets Research

Global Markets Division for Asia

E: lin_li@hk.mufg.jp

KHANG SEK LEE

Associate

Global Markets Research

Global Markets Division for Asia

E: khangsek_lee@hk.mufg.jp

MICHAEL WAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: michael_wan@sg.mufg.jp

LLOYD CHAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: lloyd_chan@sg.mufg.jp

SOOJIN KIM

Analyst, ESG and Emerging Markets Research – EMEA

DIFC Branch – Dubai

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

July 2026

KEY EVENTS IN THE MONTH AHEAD

1) A 60-DAY NEGOTIATION WINDOW

The focus of the financial markets has shifted away from the US-Iran conflict after the 60-day extension of the ceasefire was agreed in June. The 60-day window is believed to end on 18th August allowing time for the contentious issue of Iran’s nuclear ambitions to be tackled. A US and an Iranian delegation are in Doha for indirect talks, but it is likely that these negotiations will go to the wire and could require a further extension. The IAEA has indicated it will return to Iran for inspections although no date has been announced. Strait of Hormuz tanker traffic will be monitored closely this month and as long as traffic does not tail off notably, crude oil should remain at current lower levels. The issue of Iran wanting full control of traffic will be another source of disagreement given Iran’s attempts to charge tankers for passing through the strait. If crude oil remains stable at around the USD 70pbl level it will likely reinforce the potential for global yields to fall further.

2) LESS ACTIVE MONTH FOR CENTRAL BANKS

Following the nine G10 central bank meetings in June, this month will be a little less active although July will end with a flurry of key meetings. Six G10 central banks meet this month starting with the RBNZ (8th) which didn’t meet in June. Pricing for a hike by the RBNZ has eased somewhat since the drop in crude oil prices extended further in June but the implied probability of a 25bp hike remains close to 70%. The BoC meets a week later (15th) with policy likely to remain on hold. Similarly, the ECB at its meeting (23rd) will keep its policy stance unchanged following the hike in June. The final week of July will see the FOMC meet (29th) followed by the BoE (30th) and then the BoJ (31st) with all three central banks likely to keep policy unchanged. Amongst these three, pricing for a hike is currently highest for the Fed with an implied probability of 32%. These OIS pricings could shift somewhat with Fed Chair Warsh, ECB President Lagarde and BoE Governor Bailey all speaking together at Sintra in Portugal (1st July). The style of Fed Chair Warsh’s communication will be of interest given his indication that he dislikes forward guidance and hence there will be significant interest in his first semi-annual testimony to the House Finance Committee on 14th July. The formal start of the UK Labour Party leadership election will be 9th July and will likely close on 17th July with Andy Burnham probably the sole candidate and hence will become the new Labour party leader and the new Prime Minister.

3) JULY POLITBURO MEETING KEY TO WATCH

This mid year meeting will cover a macro policy review, and set near term policy priorities for H2, including fiscal stimulus. We expect to learn more about property sector support, credit expansion and explicit FX stability guidance too. The read out will shed light on the government’s deliberations on growth support vs. financial stability. Any escalation in pro growth easing (infrastructure, local government financing, consumption support) and a stability focused tone with firm FX language would help anchor RMB expectations and imply a bias for USD/CNY to decline.

Forecast rates against the US dollar - End-Q3 to End-Q2 2027

Spot close 30.06.26 | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

DXY | 101.155 | 99.770 | 98.190 | 96.630 | 96.410 |

JPY | 162.53 | 160.00 | 158.00 | 156.00 | 154.00 |

EUR | 1.1422 | 1.1600 | 1.1800 | 1.2000 | 1.2000 |

GBP | 1.3267 | 1.3260 | 1.3410 | 1.3560 | 1.3480 |

CNY | 6.7857 | 6.7000 | 6.6500 | 6.6000 | 6.6000 |

AUD | 0.6915 | 0.7000 | 0.7100 | 0.7200 | 0.7300 |

NZD | 0.5677 | 0.5700 | 0.5800 | 0.5900 | 0.6000 |

CAD | 1.4200 | 1.4000 | 1.3800 | 1.3600 | 1.3500 |

NOK | 9.9047 | 9.7410 | 9.4920 | 9.3330 | 9.2500 |

SEK | 9.6906 | 9.4830 | 9.2370 | 9.0000 | 8.9170 |

CHF | 0.8080 | 0.7930 | 0.7800 | 0.7630 | 0.7580 |

|

|

|

|

|

|

CZK | 21.240 | 20.860 | 20.420 | 20.000 | 19.920 |

HUF | 311.61 | 306.00 | 300.80 | 291.70 | 287.50 |

PLN | 3.7624 | 3.6720 | 3.5930 | 3.5170 | 3.5170 |

RON | 4.5844 | 4.5170 | 4.4660 | 4.4170 | 4.4330 |

RUB | 77.854 | 76.490 | 77.710 | 77.980 | 80.730 |

ZAR | 16.395 | 16.600 | 16.400 | 16.200 | 16.000 |

TRY | 46.656 | 49.000 | 51.500 | 53.000 | 54.500 |

|

|

|

|

|

|

INR | 94.660 | 92.500 | 93.000 | 94.000 | 95.000 |

IDR | 17902 | 18100 | 18350 | 18500 | 18700 |

MYR | 4.0825 | 4.1000 | 4.1500 | 4.1000 | 4.0000 |

PHP | 61.318 | 61.500 | 61.000 | 60.500 | 60.000 |

SGD | 1.2940 | 1.3100 | 1.3200 | 1.3000 | 1.2700 |

KRW | 1548.6 | 1520.0 | 1500.0 | 1480.0 | 1460.0 |

TWD | 31.842 | 31.600 | 31.300 | 31.100 | 30.900 |

THB | 33.251 | 33.800 | 34.400 | 34.000 | 33.800 |

VND | 26304 | 26400 | 26500 | 26600 | 26700 |

|

|

|

|

|

|

ARS | 1481.1 | 1525.0 | 1575.0 | 1625.0 | 1675.0 |

BRL | 5.1753 | 5.2000 | 5.1000 | 5.0000 | 4.9000 |

CLP | 921.05 | 900.00 | 890.00 | 880.00 | 870.00 |

MXN | 17.472 | 17.500 | 17.500 | 17.250 | 17.250 |

| |||||

SAR | 3.7567 | 3.7500 | 3.7500 | 3.7500 | 3.7500 |

EGP | 49.171 | 49.750 | 51.000 | 52.500 | 54.000 |

Notes: All FX rates are expressed as units of currency per US dollar bar EUR, GBP, AUD and NZD which are expressed as dollars per unit of currency. Data source spot close; Bloomberg closing rate as of 5:00pm London time, except VND which is local onshore closing rate. All consensus forecasts are Bloomberg sourced.

US dollar

Spot close 30.06.26 | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

USD/JPY | 162.53 | 160.00 | 158.00 | 156.00 | 154.00 |

EUR/USD | 1.1422 | 1.1600 | 1.1800 | 1.2000 | 1.2000 |

Consensus | Consensus | Consensus | Consensus | ||

USD/JPY | 158.00 | 156.00 | 155.00 | 153.00 | |

EUR/USD | 1.1600 | 1.1800 | 1.1800 | 1.1800 |

MARKET UPDATE

The US dollar, on a DXY basis, advanced by 2.3% in June adding to the 0.9% gain in May, closing at the highest monthly close level since March 2025. With the focus on Middle East risks receding the FX market reverted to being driven more by rate spreads, which was to the benefit of the dollar. The 2-year yield in the US closed 17bps higher whereas yields in the euro-zone, the UK and Japan either remained stable or declined. The flat to lower yields elsewhere reflected the sharper than expected decline in crude oil prices that have now fully retraced the US-Iran conflict jump. The fact that US yields still moved higher was of course down to the FOMC meeting in June and the comments from Fed Chair Warsh. There was a notable shift in the dots profile toward monetary tightening while Chair Warsh emphasised the message of the Fed ensuring it would achieve price stability. However, we would argue that the dots profile was more a reflection of the past and a dots profile done today with Nymex trading at USD 70pbl would likely be different. OIS pricing indicates 45bps of monetary tightening by March 2027 which we see as excessive.

The speed in which crude oil prices have fallen diminishes the inflation risks notably while there are other factors that will also help lower inflation. The tariffs implemented in 2025 are set to fall out of the annual CPI calculations over the coming months that will add downside pressure to annual inflation while a quirk in rental inflation should also reverse in H2. That will help ease Fed concerns over inflation risks that should see yields decline going forward. Apart from the RBNZ, no other G10 central bank has as much tightening priced as the Fed and hence there is scope for US yields to fall relative to elsewhere. This should see this recent dollar buying momentum reverse. We would also expect some renewed focus on US fiscal risks. The fiscal outlook remains dire with the IMF projecting deficits out to 2030 in the region of 7% of GDP and the mid-term elections could well result in policy gridlock that pushes addressing the fiscal problem further into the future.

The US dollar has rebounded fuelled by Fed rate hike expectations that we believe will soon begin to fade. Inflation is set to recede while GDP growth excluding AI-related activities has been subdued. Consumer confidence remains around covid-lows that highlights vulnerabilities. Fiscal risks coming back into focus as yields decline will encourage renewed hedging of US assets and weigh on the dollar.

OUTLOOK

The US dollar, on a DXY basis, advanced by 0.9% in May, partially reversing the drop in April as the dynamics in the FX market started to change. Brent crude oil and risk became less influential in driving the US dollar and there was a shift back to the more traditional driver – rate spreads. This was prompted by the jump in US yields as investors reassessed the Fed policy stance and considered the need for monetary tightening given the continued rise in inflation pressures. The 2-year UST bond yield jumped by 13bps in May whereas in Europe, the 2-year yield dropped by 11bps and the UK the drop was a larger, 24bps. US yields basically played catch-up from underpriced risks of hikes while in Europe investors viewed hiking as overpriced. The risk now is that the momentum higher for yields in the US could reverse if this reported US-Iran deal is confirmed and energy prices fall further. That said, we do not expect initial big moves. Brent crude oil is already close to 20% down in just two weeks and hence much of the good news associated with a deal is priced.

While the argument put forward of the need for a rate hike in the US remains unconvincing in our view it is clear that the debate on Fed policy has shift from no change or a cut to no change or a hike with most comments from Fed officials now assessing the risks between a hike or no hike. The FOMC minutes from the April meeting indicating broadening support for the implied easing bias to be dropped and a growing view that a hike would be needed if inflation remained elevated. However, we should not underestimate the potential influence of Fed Chair Warsh. He is known to favour trimmed measures of inflation as a more accurate measure of underlying inflation conditions and the Dallas Fed Trimmed Mean YoY CPI rate fell to 2.3% in April – the measure has been stable around this level for three months and the lowest since August 2021. If a US-Iran extended ceasefire deal is agreed, then Warsh will push this view harder and that will likely result in the rates curve removing the current pricing of a risk of hikes back to the potential for easing.

US inflation data is likely to show a pick-up in the coming months but happening in the context of a 60-day deal extension and the reopening of the Strait of Hormuz will allow Fed officials to look through this and focus on potential downside risks to growth. We see that approach as reinforcing downside risks for the US dollar and hence we are maintaining our bearish outlook for the dollar over the forecast period.

INTEREST RATE OUTLOOK

Interest Rate Close | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

Policy Rate | 3.63% | 3.63% | 3.38% | 3.13% | 3.13% |

3-Month T-Bill | 3.81% | 3.65% | 3.50% | 3.25% | 3.13% |

10-Year Yield | 4.47% | 4.25% | 4.13% | 4.00% | 3.88% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

For the last 6 weeks our view partially hinged on the Strait of Hormuz reopening, where we operated under the assumption that once some version of a more lasting ceasefire was agreed upon, that oil prices would drop down towards the mid-70s. Well, WTI oil prices made a move to $70 and briefly under by the end of June. Granted US gasoline prices are proving a bit more sticky, but in general the energy component for consumer prices will see a notable decline in the coming months if this holds. Inflation expectations have declined in sympathy but outright nominal rates are being held back given that real rates have remained elevated. A lot of this has to do with the recent hawkish pivot and change in leadership at the Fed, with Kevin Warsh’s first FOMC presser also coming across as hawkish (see link). We believe the market pricing is inconsistent now, with rate expectations pricing in both a slight rise in rates to then be followed by a cut later in 2027. We think the bar to hike rates is high in the US, especially post the recent drop in oil prices and see the Fed on hold until late 2026 before making two more rate cuts to hit neutral rate levels of ~3.00%.

(George Goncalves)

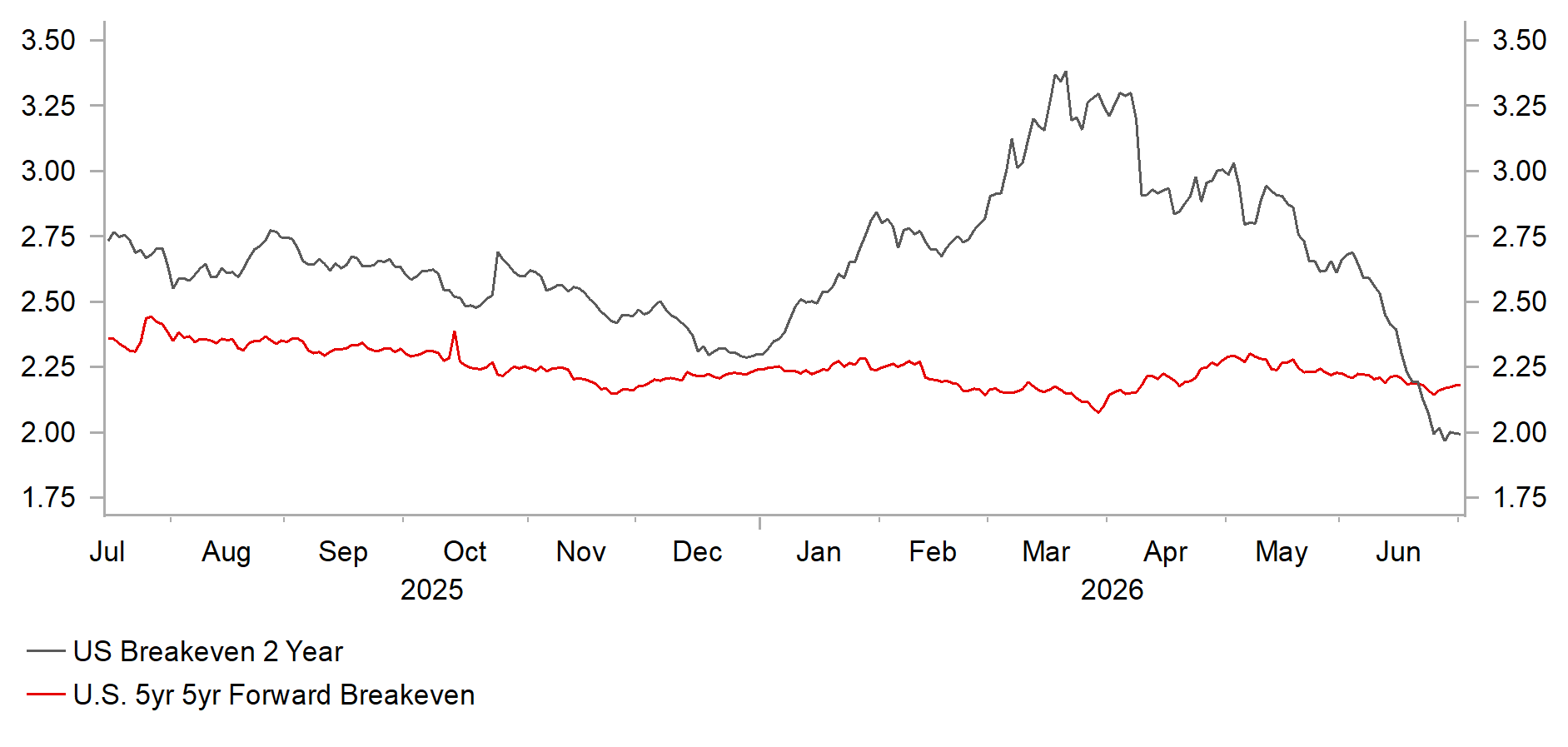

SHORT-TERM VS. LONG-TERM US BREAKEVEN INFLATION RATES

Source: Bloomberg, Macrobond & MUFG GMR

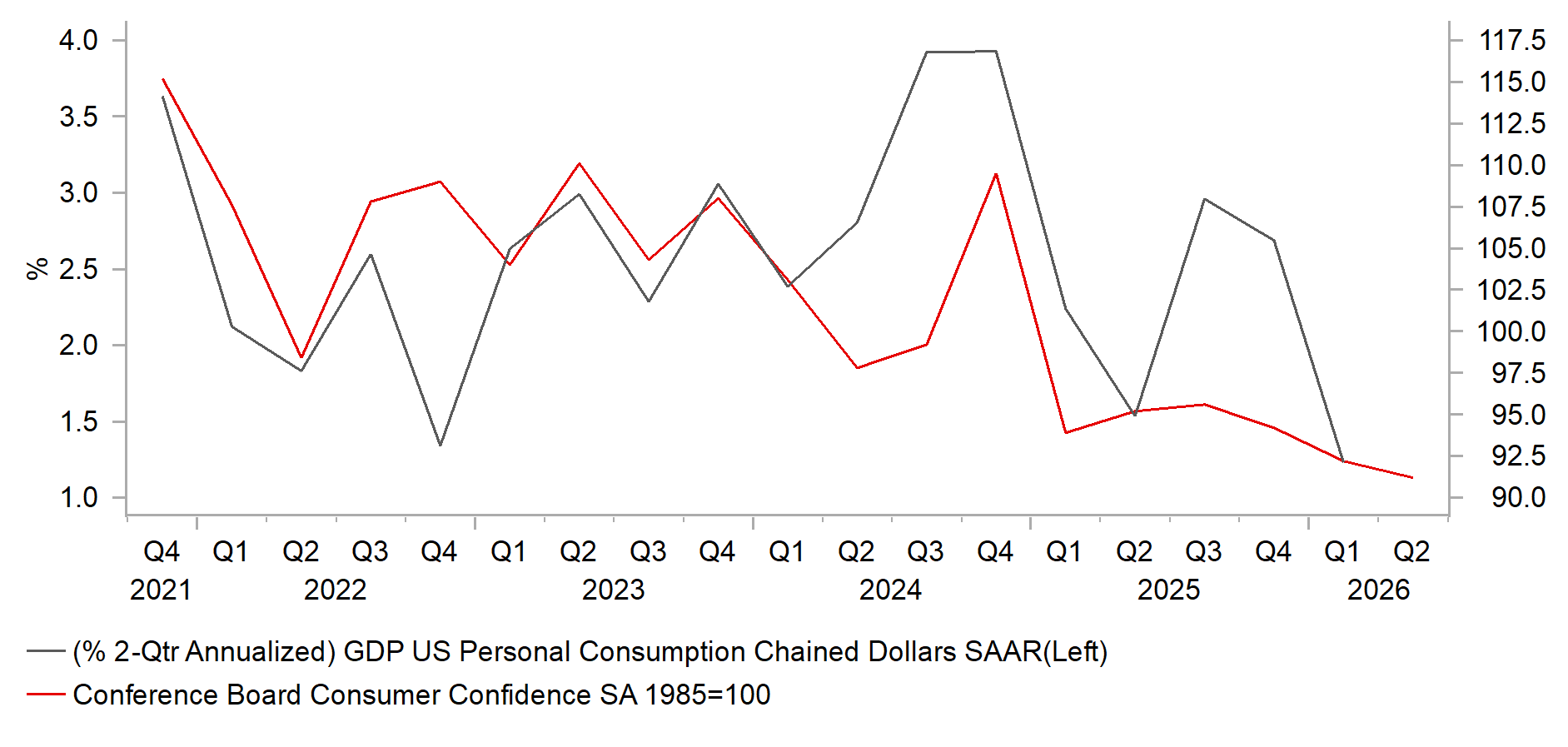

US PERSONAL CONSUMPTION VS. CONSUMER CONFIDENCE

Source: Bloomberg, Macrobond & MUFG GMR

Japanese yen

Spot close 30.06.26 | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

USD/JPY | 162.53 | 160.00 | 158.00 | 156.00 | 154.00 |

EUR/JPY | 185.64 | 185.60 | 186.40 | 187.20 | 184.80 |

Consensus | Consensus | Consensus | Consensus | ||

USD/JPY | 158.00 | 156.00 | 155.00 | 153.00 | |

EUR/JPY | 184.00 | 184.00 | 182.00 | 182.00 |

MARKET UPDATE

In June the yen weakened versus the US dollar in terms of London closing rates from 159.15 to 162.53. However, the yen strengthened marginally versus the euro from 185.93 to 185.64. The BoJ at its meeting in June raised the key policy rate by 25bps to 1.00%, the highest level since 1995 and the third 25bp hike since January 2025. The BoJ also confirmed it would continue cutting JGB monthly purchases at a pace of reduction of JPY 200bn per quarter through to Q1 2027 and would then halt the reduction with monthly purchases by then falling to JPY 2trn per month.

OUTLOOK

The yen weakened further in June with USD/JPY breaking above the intervention levels from April/May and above the recent high of 161.95 to trade at levels not seen since 1986. The record JPY 11.7trn worth of yen selling by the MoF has come to very little in terms of strengthening the yen but it could be argued that it continues to play a role in deterring yen selling at these levels. The MoF has been less vocal on threatening intervention in recent weeks but Finance Minister Katayama on 30th June repeated that Japan and the US are aligned on FX policy, implying support for further intervention if required. Katayama’s explicit threats to intervene are now having little impact. The US 2-year yield closed 17bps higher in June following the hawkish FOMC meeting and the MoF may well be more accepting of further yen weakness at least until the global backdrop becomes more aligned to a weaker US dollar. It is our view that this will happen given we see the next Fed move to be a cut. The sharp decline in crude oil is also yen supportive from a terms of trade perspective.

As expected, the BoJ hiked its key policy rate by 25bps in June, but the action failed to deter yen selling. The communication from the BoJ suggested a continued pace of raising rates every six months and this is deemed too cautious to provide support for the yen. We see a growing risk that the BoJ may need to up the pace of rate hikes, and hikes in September and December is an increasing risk. The BoJ communications in June did point to an increased upside inflation risk which without response helps to fuel yen selling as expectations increase of yields remaining lower for longer in real terms. A more active BoJ would also help dispel the belief amongst investors that the Takaichi government is holding the BoJ back from hiking. There were reports by Bloomberg at the end of June that a government economic policy document set for release in July would include a call for “appropriate” monetary policy – a suggested hint for continued BoJ caution. Inflation is set to pick up again after falling below the 2.0% target. The BoJ forecasts the nationwide core CPI to reach 2.8% this fiscal year. That could be raised further given the upside risks.

If US yields fail to decline and expectations of a BoJ rate hike in September remain low (5bps priced currently), then USD/JPY could keep moving higher with the MoF reluctant to continue intervening. We do ultimately see US yields falling from current levels which coupled with further BoJ rate hikes will prompt USD/JPY to fall.

INTEREST RATE OUTLOOK

Interest Rate Close | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

Policy Rate | 1.00% | 1.25% | 1.25% | 1.50% | 1.50% |

3-Month Bill | 0.90% | 1.10% | 1.30% | 1.50% | 1.60% |

10-Year Yield | 2.68% | 2.70% | 2.60% | 2.60% | 2.50% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year JGB yield increased marginally in June, by 1bp to close at 2.68%, the highest monthly close since May 1997. The modest move higher in June followed a 14bp jump in May suggesting the upward momentum in yields may be fading. But even the modest increase in June was telling given yields in the other key bond markets all declined in June as crude oil prices fell further. The same issues continue to weigh on the JGB market that points to upside risks over the short-term. The BoJ raised rates in June but maintained a cautious tone and guidance on future moves. A rate increase every six months is deemed as too slow given the policy rate remains negative in real terms and there is a risk that the BoJ may need to up the pace of tightening. A rate hike in September is possible and the risk is under-priced. The Takaichi government pressuring the BoJ to remain cautious remains an issue that will only be removed by bolder BoJ action. The Takaichi long-term investment plan totalling JPY 370trn has also undermine bond investor confidence. We assume further BoJ hikes and more stable inflation in 2027 will help stabilise yields.

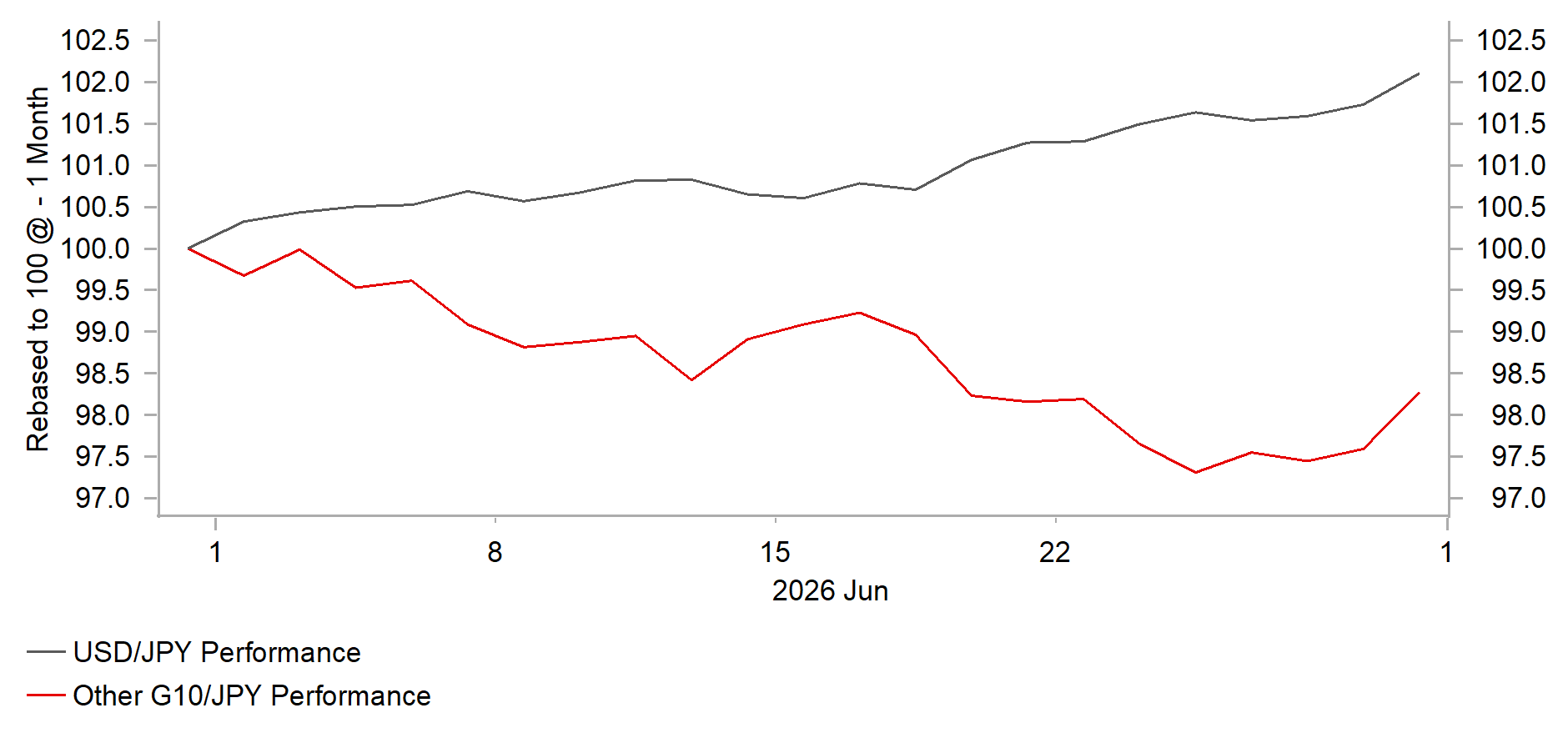

JPY PERFORMANCE AGAINST USD & OTHER G10 FX

Source: Bloomberg & MUFG GMR

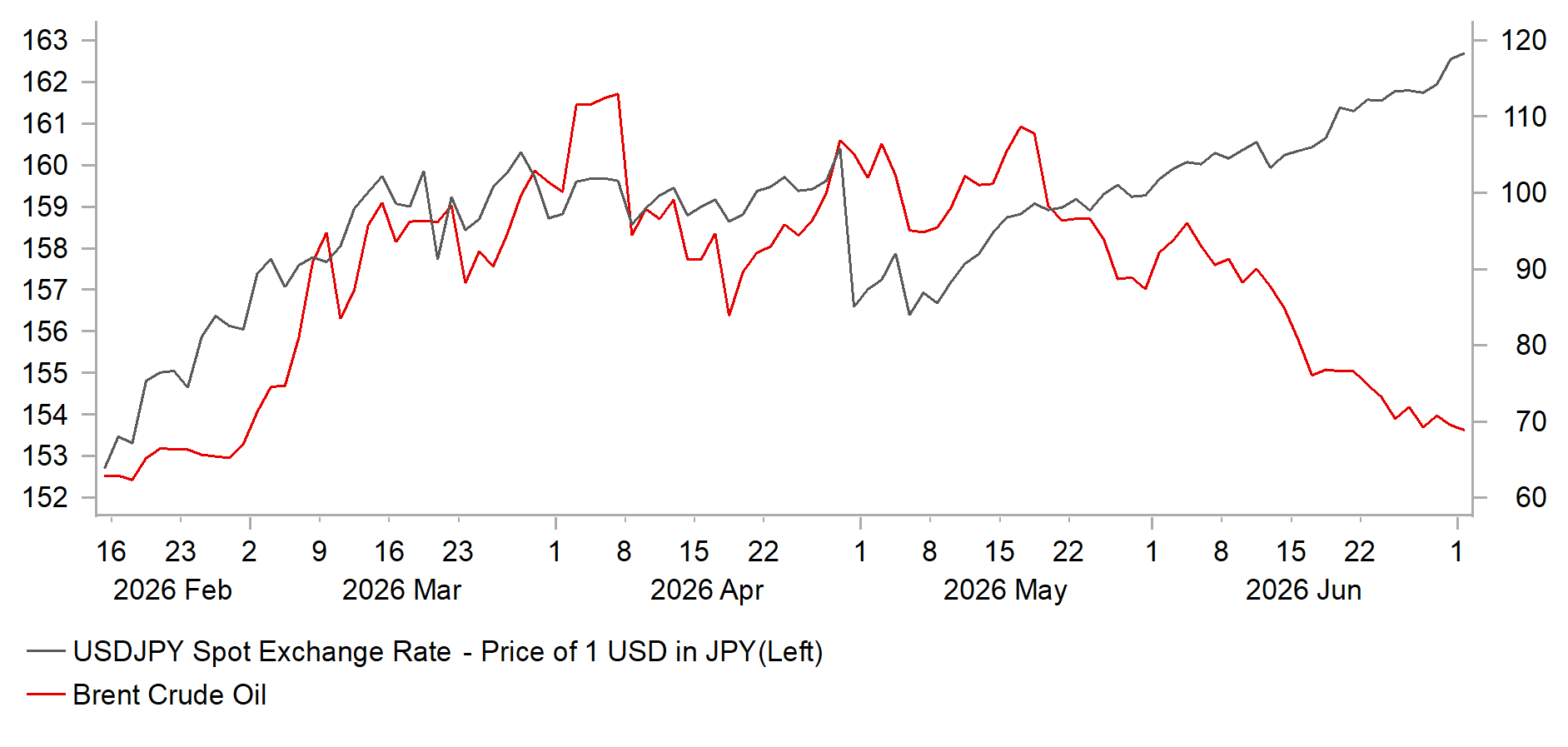

USD/JPY VS BRENT CRUDE

Source: Bloomberg, Macrobond & MUFG GMR

Euro

Spot close 30.06.26 | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

EUR/USD | 1.1422 | 1.1600 | 1.1800 | 1.2000 | 1.2000 |

EUR/JPY | 185.64 | 185.60 | 186.40 | 187.20 | 184.80 |

Consensus | Consensus | Consensus | Consensus | ||

EUR/USD | 1.1600 | 1.1800 | 1.1800 | 1.1800 | |

EUR/JPY | 184.00 | 184.00 | 182.00 | 182.00 |

MARKET UPDATE

In June the euro weakened against the US dollar in terms of London closing rates from 1.1683 to 1.1422. The ECB at its meeting in June raised the deposit rate by 25bps to 2.25% - the first hike since September 2023 when the ECB completed its tightening cycle following the global inflation shock. Balance sheet reduction continues with the ECB’s projected maturities from both APP and PEPP expected to result in a EUR 500bn reduction in balance sheet holdings in 2026

OUTLOOK

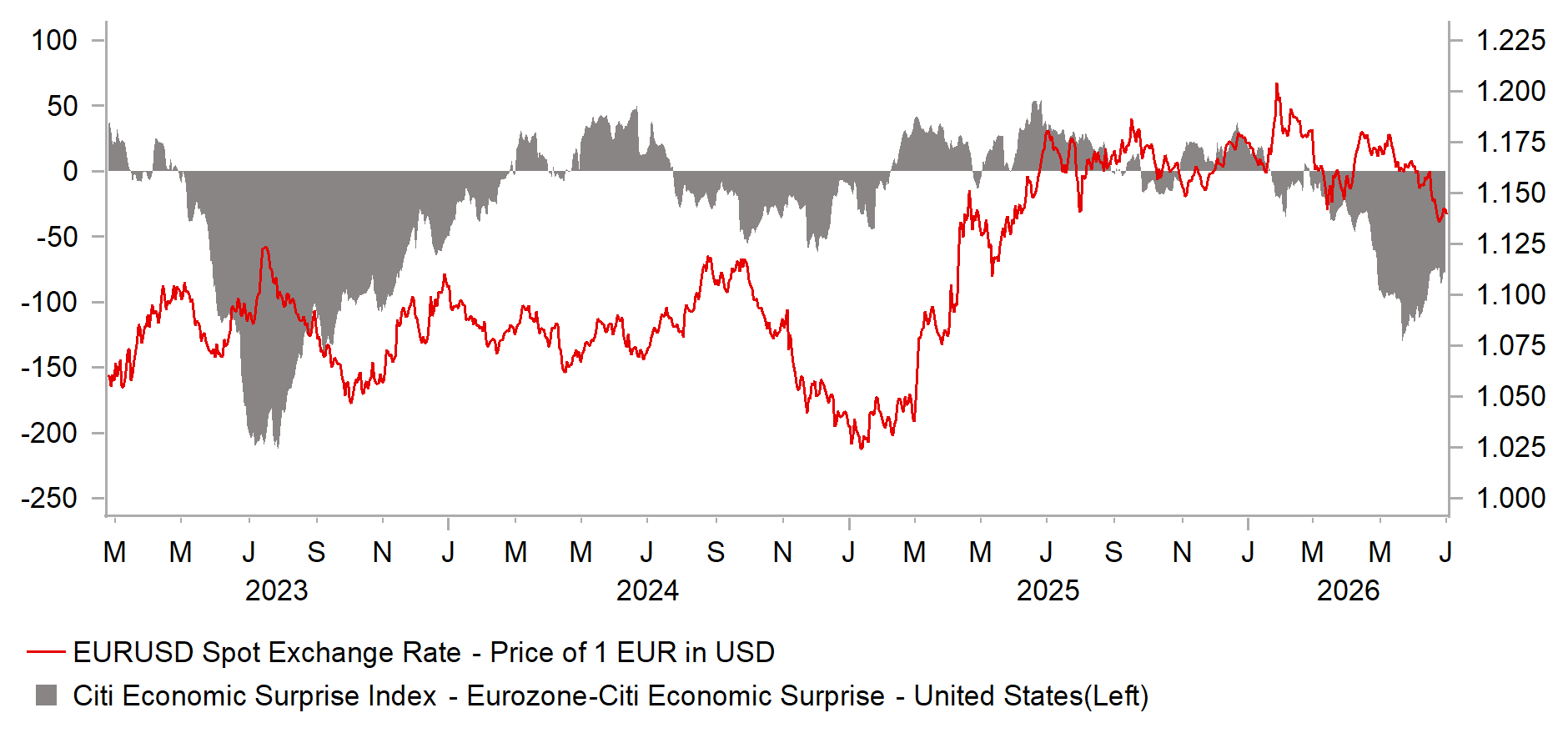

The euro weakened versus the US dollar further in June with expectations of additional rate hikes from the ECB diminishing. We did not expect to see Brent crude oil prices falling as rapidly and assumed there would be a more substantial geopolitical risk premium throughout the remainder of 2026 which would have resulted in an inflation level that prompted the ECB to hike again. That view is certainly in doubt if crude oil remains at these levels or obviously fall further. Prior to the ECB rate hike in June, the OIS market was close to pricing three rate hikes and now roughly one hike is priced – so a rate hike has been removed fuelled by the sharp decline in crude oil prices following the ceasefire extension deal. The drop in crude oil and some of the inflation data do suggest that second-round inflation risks are less than feared. We did not expect the ECB to hike on three occasions in any case and still view one further rate hike as feasible although the risks have certainly shifted to the potential of no additional rate hikes. However, ECB Chief Economist Philip Lane did state that the top of the neutral policy range had likely drifted higher to 2.50%, which implies there being limited risk to one further rate hike to provide insurance. The ECB 1-year inflation expectation reading fell from 4.0% in April to 3.5% in May, below the consensus. However, the 3-year level remained at 2.9%, slightly above the market consensus.

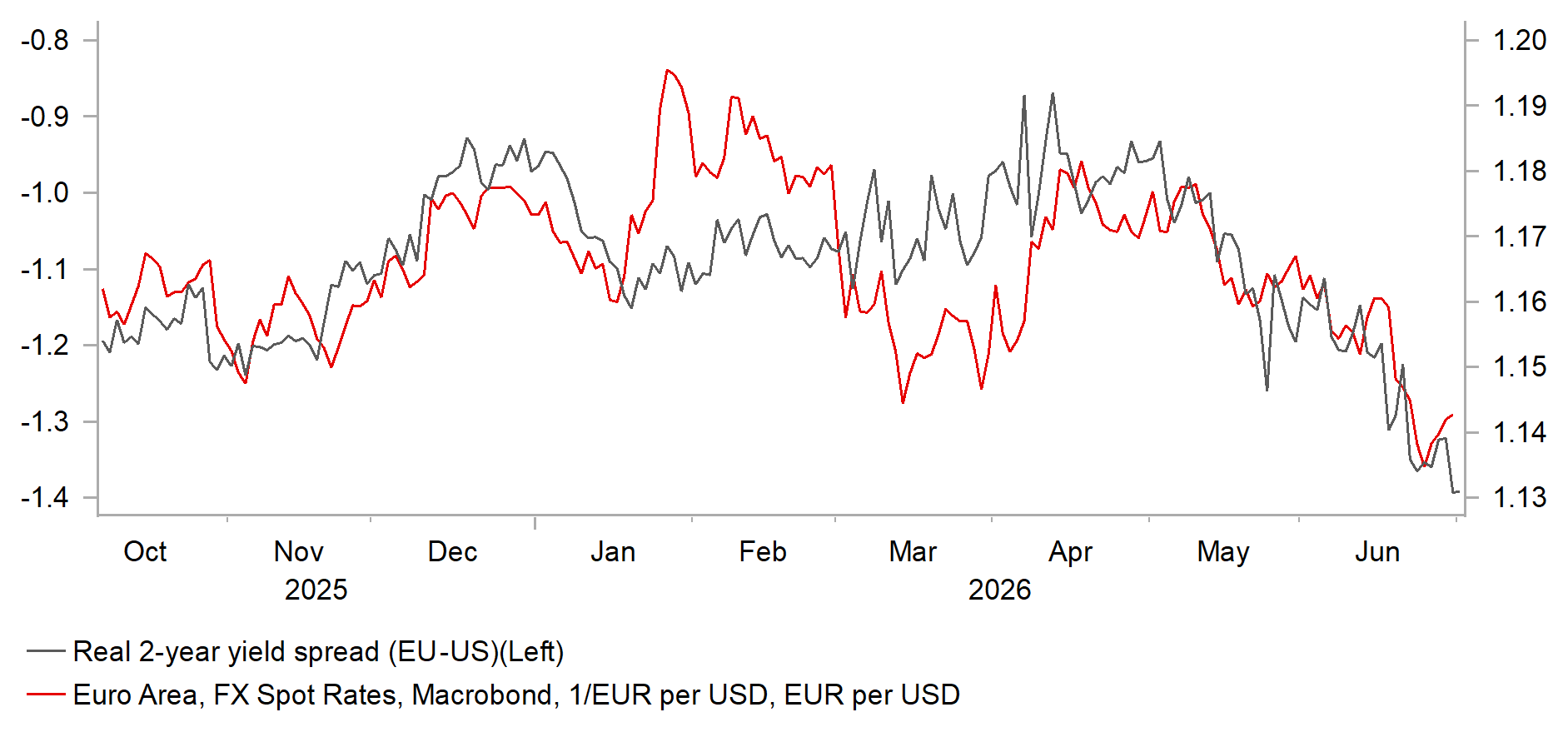

As we have highlighted before, the reduced concerns and focus on the US-Iran conflict and the sharp drop in crude oil prices have seen the gradual importance of rate spreads for FX increase. Relative macro has been revived as a driver of FX. The 2-year EU-US swap spread fell sharply in May and modestly further in June as excessive rate hike pricing was removed from the curve in Europe. If crude oil prices remain around current levels, we would conclude that pricing for a Fed rate hike is more unrealistic than an ECB hike and would assume the spread has scope to move back in favour of a retracement higher in EUR/USD. ECB rhetoric implies reduced risk of a hike but given the ECB has hiked, it remains plausible that a further insurance hike is delivered.

EUR/USD has now traded below the 1.1500-level for the longest period since June last year but we do not see this as a signal of a sustained move lower. Yield spreads have become a more important driver of FX again and we expect EUR/USD to recover as Fed rate hike expectations recede while the ECB hikes one last time

INTEREST RATE OUTLOOK

Interest Rate Close | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

Policy Rate | 2.25% | 2.50% | 2.50% | 2.50% | 2.50% |

3-Month Bill | 2.38% | 2.60% | 2.55% | 2.50% | 2.50% |

10-Year Yield | 2.86% | 2.90% | 2.90% | 2.80% | 2.60% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year German bund yield declined in June, closing 8bps lower at 2.86% with the continued decline in crude oil prices easing inflation risks. The price of Brent crude oil has fully reversed the US-Iran conflict surge which should ease considerably the energy-related pass-through to broader inflation. Some of the rhetoric from ECB officials in June certainly indicates a shift to a more neutral bias going forward. However, the scope for an additional hike as an insurance remains. Chief Economist Philip Lane’s comment of the neutral rate drifting higher is one indication of a lower hurdle to raising rates while he also added that energy pass-through risks would persist for some time indicating that the window for a hike will remain open possibly through the rest of this year. President Lagarde also stated that the euro-zone economy had become more resilient to external shocks suggesting the economy could weather a hike if required. If we are correct we would see a hike as certainly adding to curve flattening momentum as inflation risks recede further. The speed of decline in crude oil prices has resulted in the 10-year bund yield falling more notably in June and we have tweaked our 2026 yield levels modestly lower.

EUR/USD VS. EZ-US SHORT-TERM REAL YIELD SPREAD

Source: : Bloomberg, Macrobond & MUFG GMR

EUR/USD VS. ECONOMIC SURPRISES IN EZ & USD

Source:: Bloomberg, Macrobond & MUFG GMR

Pound Sterling

Spot close 30.06.26 | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

EUR/GBP | 0.8609 | 0.8750 | 0.8800 | 0.8850 | 0.8900 |

GBP/USD | 1.3267 | 1.3260 | 1.3410 | 1.3560 | 1.3480 |

GBP/JPY | 215.63 | 212.10 | 211.90 | 211.50 | 207.60 |

Consensus | Consensus | Consensus | Consensus | ||

GBP/USD | 1.3300 | 1.3400 | 1.3500 | 1.3600 |

MARKET UPDATE

In June the pound weakened versus the dollar in terms of London closing rates, moving from 1.3481 to 1.3267. However, the pound strengthened marginally against the euro from 0.8666 to 0.8609. The MPC at its meeting in June kept the key policy rate unchanged at 3.75%, after six 25bp cuts since August 2024.

OUTLOOK

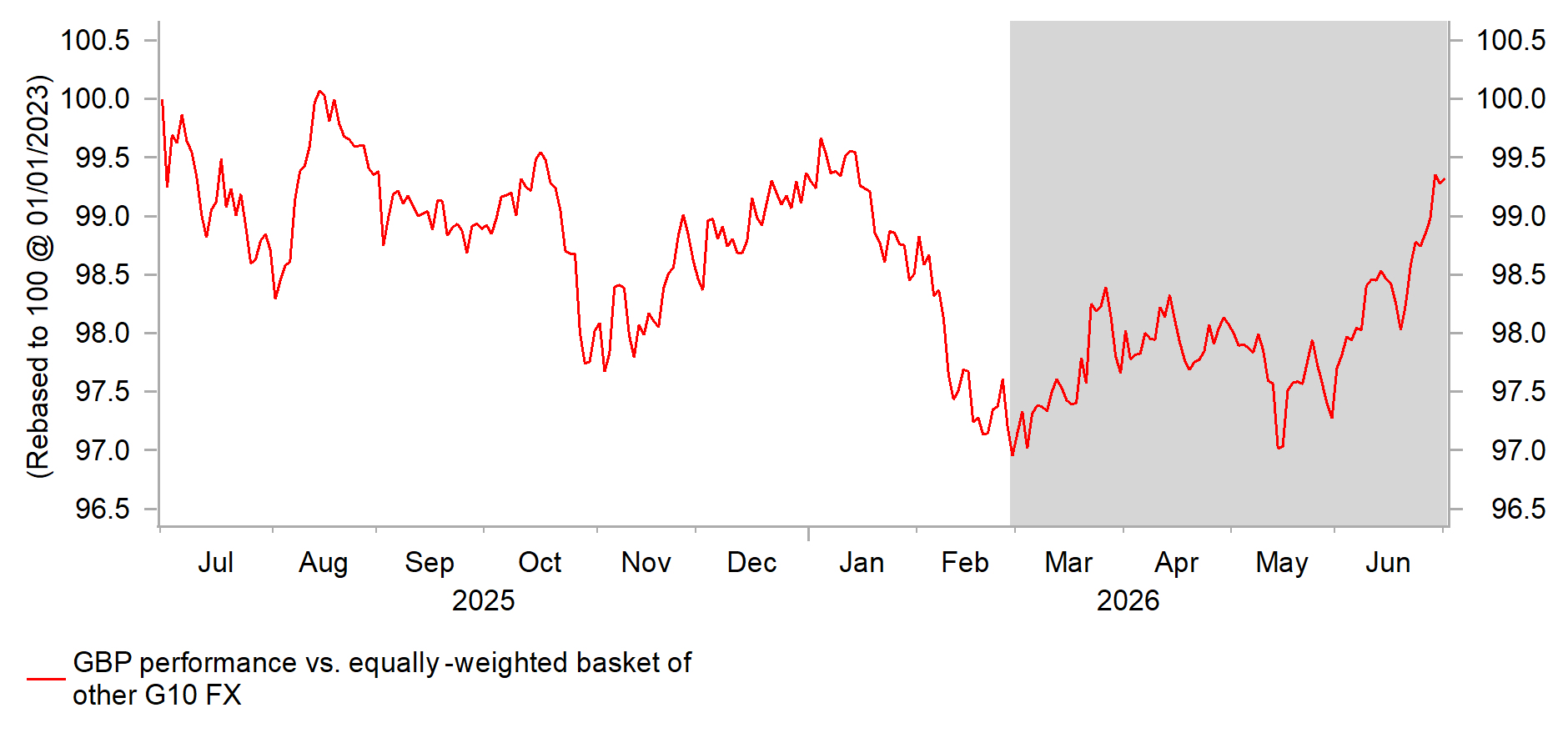

The pound weakened versus the US dollar but strengthened versus the euro and was close to unchanged on a BoE trade-weighted basis. In fact, after the US dollar, the pound was the next best performing G10 currency in June and indeed over the period since the Middle East conflict began at the end of February. Yield support helped explain that performance earlier during the Middle East conflict but not in June with the pound performing better relative to yield spread moves versus the dollar and euro. The lack of evidence of inflation feed-through from energy may be helping investor confidence although that risk will linger over the coming months. The exceptional low levels of volatility also tends to help support the pound, which usually performs poorly during periods of market stress, given the UK’s external funding needs due to the current account deficit. There may also finally be some signs after years of negativity (post Brexit) that investors see value in UK assets. Bloomberg reports nearly GBP 50bn of inbound M&A deals on a year-to-date basis. Buyers have paid a 35% average premium for UK-listed companies this year.

We have changed our call on BoE rate hikes from expecting two hikes to remaining on hold following the last two CPI data releases that were weaker than expected. In addition, the speed of decline in crude oil prices also provides capacity for the BoE to remain on hold. While lower yields are generally FX negative, in the case of the UK with policy already mildly restrictive, the reduced need to monetary tightening reduces downside growth risks and is providing support for the pound. Ever since Brexit, the UK has been viewed as a country with higher inflation risks. The lack of inflation so far since the start of the Middle East conflict may well be helping to reverse years of declining investor confidence (also seen by M&A developments).

The improved inflation backdrop is helping to deter Gilt market selling on political uncertainties. Andy Burnham looks set to become PM following PM Starmer’s resignation and so far, this change in leadership has not prompted fiscal concerns. Andy Burnham appears to be more focused on reforms, like further devolution and reduced red tape to reinvigorate housing construction. Burnham has also promised “discipline of the current fiscal rules”. We assume limited political instability.

Much of the recent GBP/USD moves have been USD-driven with the pound broadly stable. Given our US dollar bearish view is being maintained we expect the pound to advance versus the dollar while we have lowered the upside scope for EUR/GBP based on the receding risks related to the conflict in the Middle East.

INTEREST RATE OUTLOOK

Interest Rate Close | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

Policy Rate | 3.75% | 3.75% | 3.75% | 3.50% | 3.50% |

3-Month Bill | 3.89% | 3.85% | 3.75% | 3.40% | 3.40% |

10-Year Yield | 4.76% | 4.80% | 4.70% | 4.50% | 4.40% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

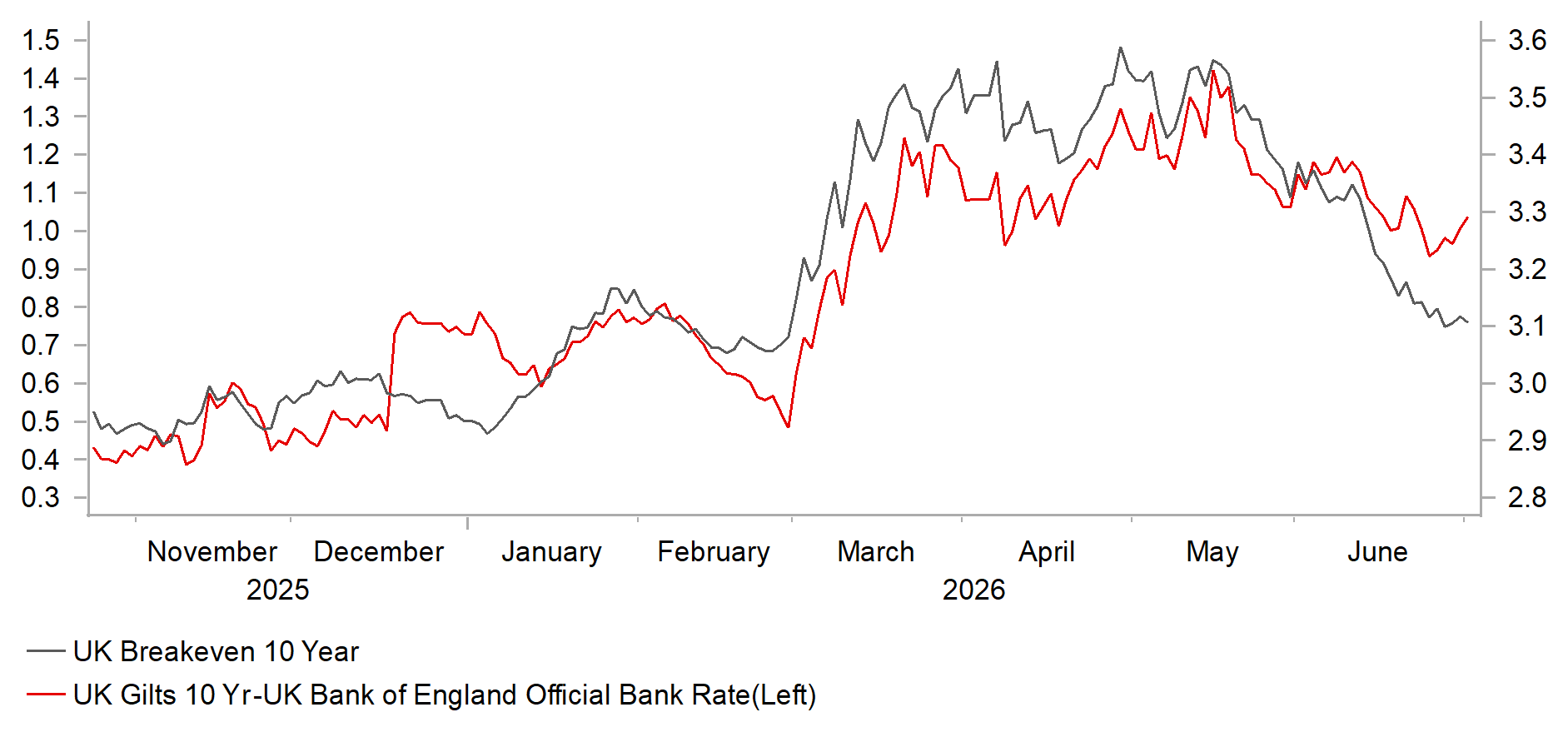

The 10-year Gilt yield declined again in June, by 5bps to close at 4.76%. The decline in the 10-year yield in May and June largely coincided with the turning point in crude oil prices as optimism over a ceasefire and the resumption of traffic through the Strait of Hormuz. In addition, the fears over an inflation overshoot in the UK have not been realised and while inflation is still likely to drift higher over the coming months (OFGEM cap increase in July) investors have lowered their assumptions for peak UK inflation. We have too and as a result we have scrapped our call for two rate hikes from the BoE and assume policy will remain on hold before rate cuts can resume later in 2027. We had also assumed a crude oil risk premium of around USD 10-15pbl but Brent has already fully retraced the post-conflict increase that opens up scope for front-end yields globally to gradually decline from here. We previously assumed the 10-year yield would fall to 4.50% by Q1 2027 but given the speed of crude oil price retracement and based on the assumptions that we do not see a sustained rebound or any notable political instability and a smooth leadership change, we have lowered our Gilt yield projections.

UK 10Y GILT YIELD vs. BREAKEVEN INFLATION

Source: : Bloomberg, Macrobond & MUFG GMR

GBP PERFORMANCE SINCE US-IRAN CONFLICT BEGAN

Source: : Bloomberg, Macrobond & MUFG GMR

Chinese renminbi

Spot close 30.06.26 | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

USD/CNY | 6.7857 | 6.7000 | 6.6500 | 6.6000 | 6.6000 |

USD/HKD | 7.8421 | 7.8200 | 7.8200 | 7.8200 | 7.8200 |

Consensus | Consensus | Consensus | Consensus | ||

USD/CNY | 6.7700 | 6.7400 | 6.7100 | 6.7000 | |

USD/HKD | 7.8000 | 7.8000 | 7.8000 | 7.8000 |

MARKET UPDATE

In June, USD/CNY moved from 6.7658 to 6.7857. On 22nd June, the PBoC kept the 1Y and 5Y LPR steady at 3.00% and 3.50% respectively. The PBoC introduced the overnight reverse repo operation as a new monetary policy tool on 29th-30th June, with the operation volume disclosed but not the interest rate.

OUTLOOK

China’s economy weakened further in May from April, with softness broadening across domestic demand, reaffirming the “two-speed” nature of the economy as exports and industrial production remained resilient. In particular, the FAI contraction became more pronounced, with YTD growth slumping to -4.1%yoy in May as infrastructure investment slowed and manufacturing investment unexpectedly contracted, the first decline since the Covid period. Similarly, retail sales also weakened, with demand for big-ticket items remaining soft but staple goods growth holding up, highlighting persistently weak household confidence. The weakness in demand was also reflected in May CPI inflation, with core inflation edging down to 1.1%yoy, suggesting limited spillover from higher energy prices. Household deleveraging remained evident, with loan balances contracting for a second consecutive month in May, reflected in both short-term and longer-term borrowing. While tech-related exports and industrial production continue to demonstrate resilience, the broader economic slowdown cannot be fully offset by these sectors alone. On the other hand, the latest June official PMIs showed a modest pickup in manufacturing (+0.3ppts to 50.3) and services activity (+0.1ppts to 50.4), although we remain cautious regarding the pace of any recovery in domestic demand. The Politburo meeting in April launched the “Six Networks” initiative, establishing a unified infrastructure priority for the upcoming 15th Five-Year Plan period, covering water, power grids, computing, next-generation communications, urban pipelines and logistics. This initiative serves as a large-scale investment and stimulus engine that supports demand, employment and industrial activity in the near term, while enhancing productivity over the medium to longer term. It is estimated to generate RMB7tn of investment this year (around 14% of 2025 FAI).

The CNY was resilient in June weakening only modestly (0.3%), despite the broader 2.3% dollar gain. A hawkish Fed repricing, higher US yields, resilient US data dominated the Dollar’s movement, despite the decline in oil prices. Looking forward, these external factors, together with domestic developments including the July Politburo meeting, will be the main drivers for USD/CNY movement. We also expect more clarity from the July Politburo on policy supports for the economy in near term, and more information on the road map of investment activities of the “six networks”. These likely anchor a mild strengthening bias for CNY against the dollar. With the market still trying to figure out Fed’s potential new framework, it is likely to see some increased policy uncertainty and volatility in US dollar and Asian currencies, having said that, the CNY likely remains relatively resilient compared with Asian peers.

INTEREST RATE OUTLOOK

Interest Rate Close | Q3 2026 | Q4 2026 | Q1 2027 | Q2 2027 | |

LPR 1Y | 3.00% | 3.00% | 3.00% | 3.00% | 3.00% |

7-Day Reverse Repo Rate | 1.40% | 1.40% | 1.40% | 1.40% | 1.40% |

10-Year Yield | 1.73% | 1.80% | 1.90% | 1.90% | 1.90% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

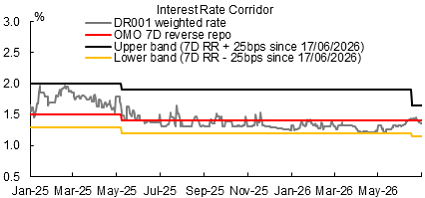

The PBOC conducted overnight reverse repo operation on 29-30 June. Introducing overnight reverse repos into the PBOC’s toolkit follows Governor Pan Gongsheng’s remarks at the Lujiazui Forum (17–18 June), where he emphasised further refining the interest rate framework to enhance price-based policy transmission and improve precision in short-term rate control. Notably, the PBOC currently discloses only injection volumes for overnight reverse repo operations, without publishing the rate—likely to avoid the market overinterpreting the tool as signalling a policy shift. We do not expect this change to alter the 7-day reverse repo rate’s role as the sole policy rate in the near term. The 7-day tenor remains dominant in collateralised repo markets (e.g. GC007, R-007), supported by strong liquidity and its ability to span weekend funding needs. Policy implications: Near term: 7-day reverse repo rate remains the primary tool, with overnight one as a supplementary liquidity fine-tuning instrument; Longer term: The overnight rate could gradually evolve into a policy anchor. PBOC’s easing bias likely to be expressed through other means including liquidity injection, credit expansion and LPR adjustment and etc.

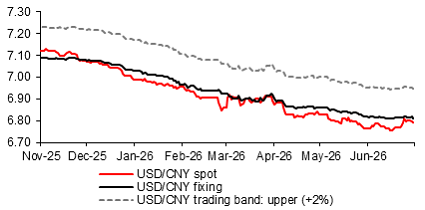

MARKET APPRECIATION BIAS ON CNY SEEMS TO HAVE EASED SOMEWHAT

Source: : Bloomberg, MUFG GMR

OVERNIGHT INTERBANK REPO RATE CURRENTLY BACK TO AROUND 1.40%

Source: : Bloomberg, MUFG GMR