Key Points

USDMYR has recently broken lower and we stay constructive on the ringgit despite Middle East risks. Near-term volatility is expected, but fundamentals should support ringgit appreciation over next 12 months.

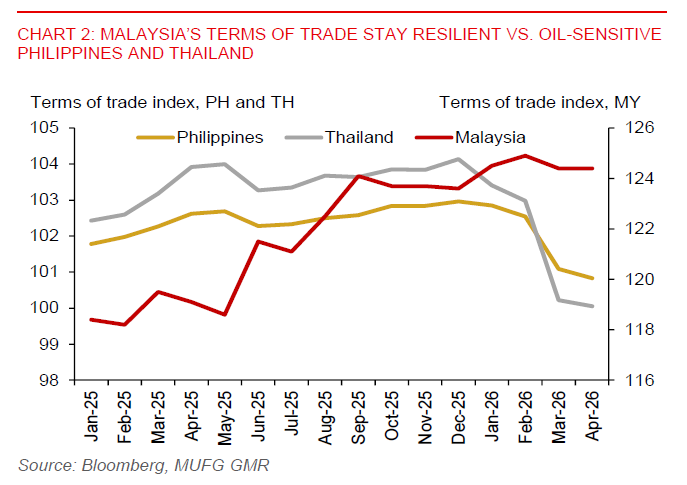

Malaysia’s status as an oil producer and net gas exporter provides the ringgit a partial natural hedge against higher energy costs. Malaysia’s terms of trade have held up far better than oil-import heavy peers such as Thailand and Philippines.

MYR volatility has been contained. The initial rise in ringgit volatility was modest versus PHP and THB, and has since fallen below pre-conflict levels, underscoring lower relative vulnerability.

Macro fundamentals and flows support MYR. We expect growth to remain at potential output of 4.8% in 2026, inflation relatively contained, BNM to stay on hold at 2.75%, and trade surplus anchored by electronics exports and steady terms of trade. Foreign bond holdings are stable, with central banks/governments now the largest foreign holder of local government bonds.

Both fiscal and inflation risks are cushioned by domestic policy buffers. Higher fuel subsidies are partly offset by stronger petroleum-linked revenues and dividends, while RON95 fuel subsidies and diesel’s low CPI weight to help contain inflation.