Key Points

Macro headwinds remain dominant. Higher US yields (2-year yield above 4%), elevated oil prices, and narrowing interest rate differentials (at historically low levels) continue to pressure IDR against the dollar.

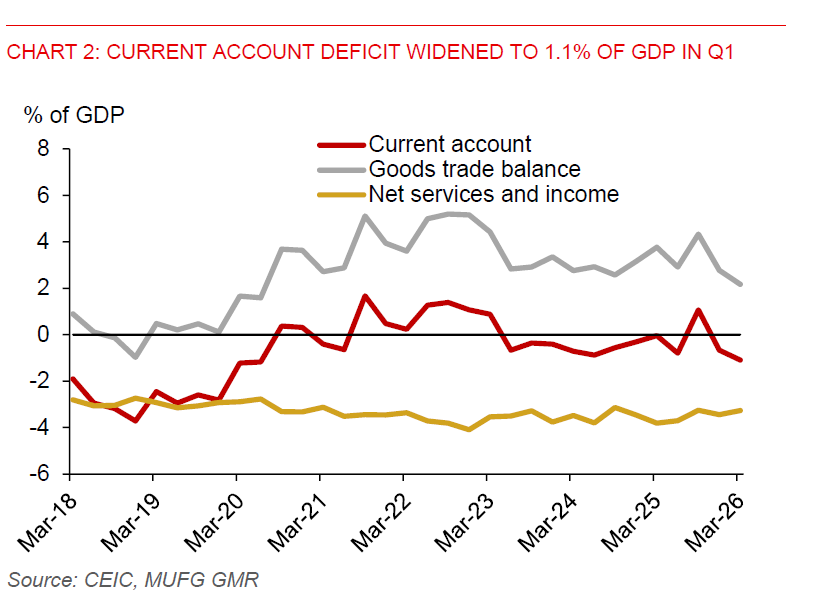

Macro pressures are increasing. Deteriorating current account (-1.1% of GDP in Q1), rising fiscal risks from energy subsidies, and softer underlying growth momentum are adding to rupiah vulnerability. Q1 growth has been driven by a strong increase in government consumption (+1.3pp to growth vs. +0.4pp in Q4 2025).

Inflation risks are skewed to the upside, driven by higher oil prices, a weaker rupiah, and a closing output gap, even as subsidies partially delay pass-through. We forecast headline inflation to average 3% in 2026 (1.9% in 2025) and GDP growth of 5.3% (5.1% in 2025).

BI tightening (50bps hike in May) and higher SRBI yields (12-month at 6.8%) provide some support for the rupiah. But concerns over government intervention in commodity exports are further weighing on investor confidence. Additional two 25bps BI rate hikes could be on the cards this year to defend the rupiah.

With positioning stretched and valuations cheap, the risk-reward may be shifting, making USDIDR increasingly vulnerable to a catalyst-driven reversal. The pair is now trading deep in overbought territory, while IDR appears to be quite cheap (near 2013 taper tantrum levels) on a real effective exchange rate basis. A potential US–Iran de-escalation could be a key trigger for reversal.