Key Points

A structural regime shift is underway. Indonesia is transitioning toward a state-controlled commodity export system under Danantara Sumberdaya Indonesia (DSI), a new subsidiary of the Danantara sovereign wealth fund. Unlike global precedents typically focused on a single commodity resource, Indonesia is attempting to apply this model across multiple key commodities such as coal, palm oil, and ferroalloys, making the scope both unique and execution intensive.

The commodity reform aims to strengthen fiscal position, FX reserves, and external stability, including ensuring full repatriation of commodity export proceeds. However, successful implementation hinges on the government’s ability to scale operational, trading, and pricing capabilities across several complex commodity value chains, alongside managing coordination across ministries and existing ecosystems.

Implementation risks are high in the near term. Uncertainty during the rollout phase could disrupt trade flows, create pricing ambiguity, and weigh on investor sentiment. Markets appear to be pricing this risk, with the rupiah underperforming regional peers amid a softening macro backdrop - including a sharply narrowing trade surplus ($89mn in April vs. $3.3bn in March), declining FX reserves (down ~USD6.3bn YoY in April), and persistent capital outflows.

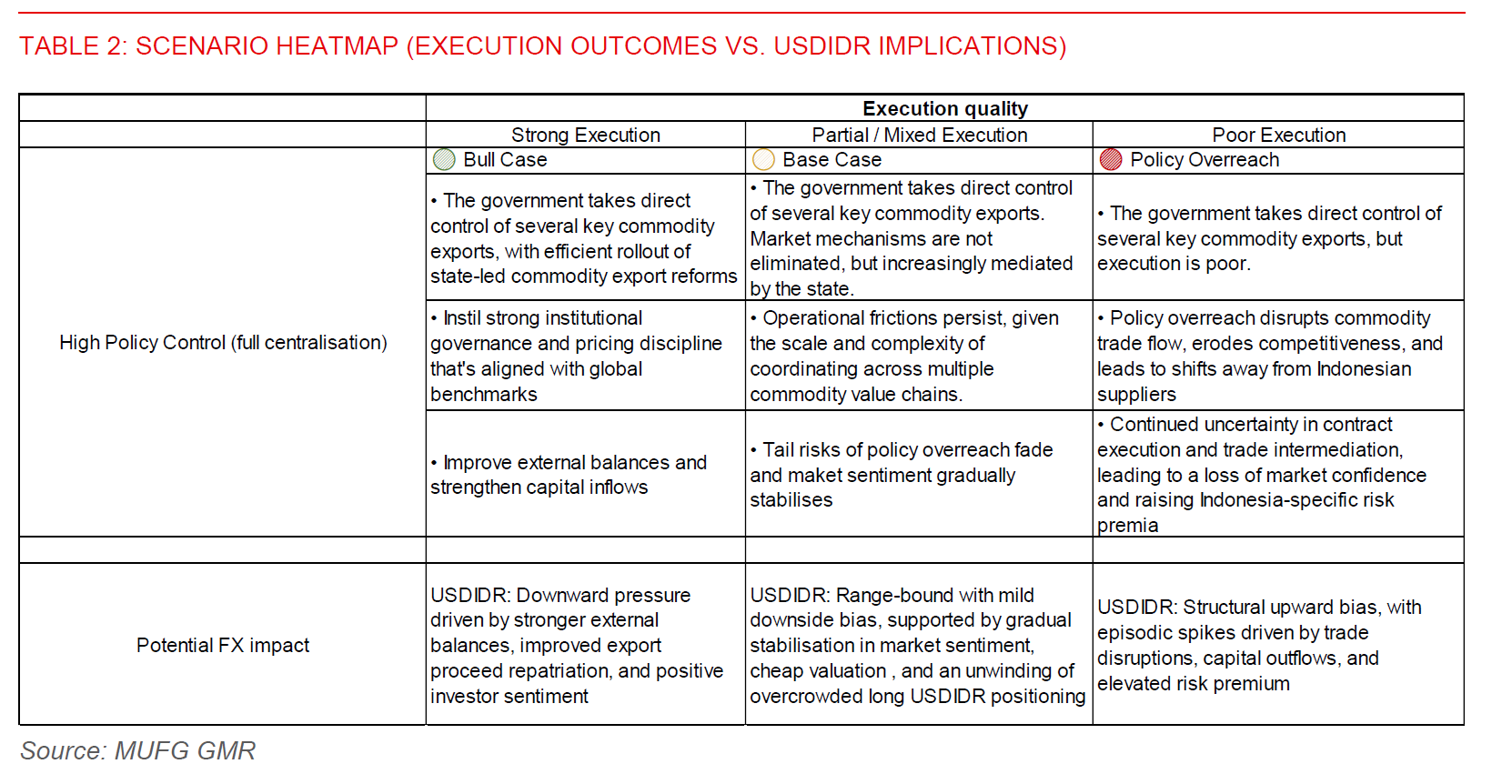

Our base case: We expect the government to take direct control of several key commodity exports. Market mechanisms are not eliminated, but increasingly mediated by the state. Prices could still reference global benchmarks, even as state influence rises. Operational challenges are likely to persist across multiple commodity value chains, given the scale and complexity of coordination. At the same time, tail risks of policy overreach gradually fade, allowing market sentiment to stabilise. USDIDR could develop a mild downside bias on an unwinding of crowded long USDIDR positioning and cheap valuations. US–Iran de-escalation could be a key trigger for reversal.

Policy outcomes are inherently binary over the medium term. Effective execution would strengthen Indonesia’s external position and underpin rupiah stability, while poor execution or policy overreach risks disrupting trade flows, eroding competitiveness, and driving prolonged currency weakness.

BI’s policy support will help to partially offset rising country risk premia. The central bank has raised policy rate by 50bps in May and enhanced FX support measures via issuing more high-yielding SRBI, helping to improve the rupiah’s front-end carry appeal.