Key Points

Bank Indonesia’s off-cycle 25bps hike and accompanying FX stabilisation measures signal a stronger policy focus on supporting the rupiah amid rising external pressures and tight dollar liquidity. Elevated US yields and building inflation risks, driven by energy prices and a closing output gap, point to further tightening, with another 25bps BI hike likely by Q3.

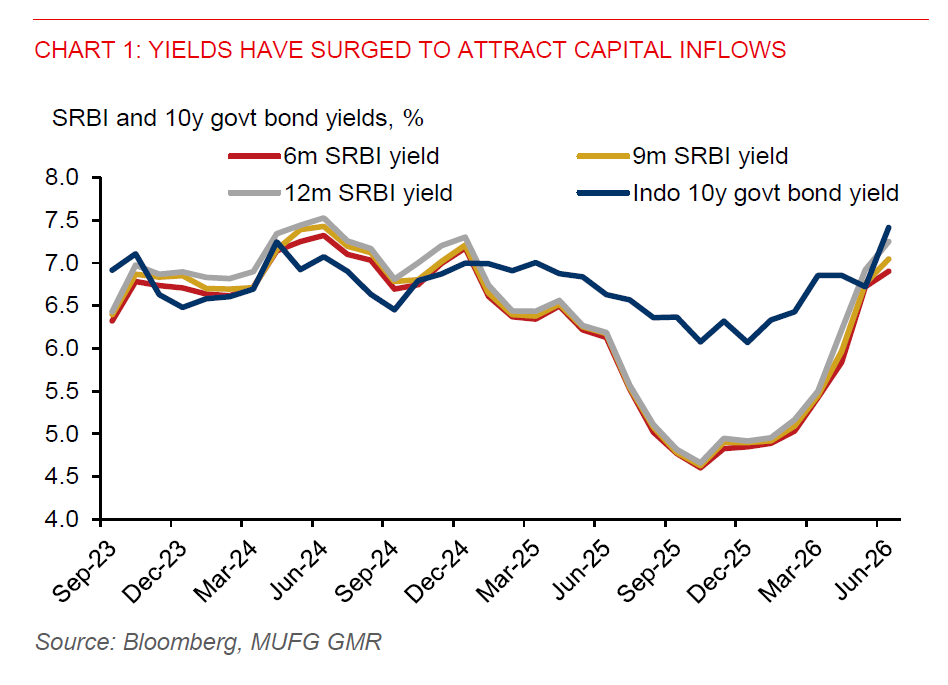

Improved nominal carry and a 10% reduction in hedging swap rates could support foreign participation in IDR assets and cushion rupiah’s weakness, particularly as IndoGB is around fair value. But persistent headwinds from ongoing Middle East conflict, elevated US yields, tight onshore USD liquidity, and weakening external buffers (narrowing trade surplus and lower FX reserves) are likely to cap any sustained rupiah recovery.

Our modelling suggests a near-term support range of 17500-17800 for USDIDR, broadly consistent with our end-Q2 forecast of 17,650, which is conditional on geopolitical de-escalation. However, with Middle East tensions flaring up again, risks are tilted to the upside. The risk is that the conflict drags into Q3, with USDIDR trending modestly higher back toward 18,200. In this environment, episodic upside spikes remain likely amid heightened global uncertainty. Near-term event risks include the 18 June FOMC meeting and the MSCI review of Indonesian equities.