To read the full report, please download PDF.

Market resilience keeps dollar moves contained

FX View:

The FX fallout this morning in response to Iran reneging on its commitment to reopen the Strait of Hormuz has been contained, with DXY advancing just 0.2%. European equities are lower in response to the worsening of the Middle East risks but hope of de-escalation remains, which has limited financial market reaction. Talks remain scheduled for Pakistan tomorrow although it is unclear at this stage whether the talks will proceed. Still, general expectations of de-escalation persist, and Brent crude oil remains below the USD 100pbl level. This week the key macro event – the Fed Chair nomination hearing of Kevin Warsh - will be a key focus and we believe will offer market participants a reminder that there are other underlying fundamental factors that are weighing on the US dollar. Fed independence uncertainties and the general unpredictability of decision-making in Washington are likely to increasingly weigh on US dollar performance.

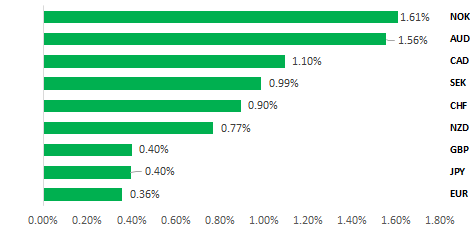

USD BROAD-BASED SELL-OFF LAST WEEK ON DE-ESCALATION HOPES

Source: Bloomberg, close on 17th April 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are maintaining a short GBP/CHF trade recommendation while our short EUR/USD trade recommendation was stopped out.

JPY Flows:

The monthly Balance of Payments data is covered this week which showed an improvement in Japan’s current account surplus led by an increased investment income surplus.

FX Correlation Analysis:

Prior to the escalation of the US–Iran conflict, FX markets operated within a clearly defined risk‑on/risk‑off framework. Since the conflict began, the jump in energy prices has reshaped FX and rates dynamics..

FX Views

USD: Are we over the worst? If yes, is the dollar headed lower?

The US dollar had already fully retraced the appreciation triggered by the Middle East conflict when Iran on Friday opened completely the Strait of Hormuz. Therefore, the FX reaction to that news at the end of last week was relatively modest. US equities advanced on Friday, and the knee-jerk FX reaction was for the US dollar to weaken by about 0.5% (DXY) but that move reversed quickly on Friday over doubts that the re-opening of the Strait of Hormuz was going to be lasting. Of course, it didn’t last and we are now awaiting news on whether the negotiation talks in Pakistan tomorrow will take place ahead of the ceasefire deadline tomorrow evening. The prospect of those talks is helping contain the risk-off reaction to the closure of the Strait of Hormuz but additionally there remains a general consensus that both sides do not want a re-escalation of intense military attacks and hence the conflict will remain contained. However, the continued lack of US dollar appreciation remains notable. The strength of US earnings has insulated US equities from the geopolitical uncertainties and that stability is limiting volatility across other markets including FX. But the lack of US dollar strength throughout the Middle East conflict does point to negative underlying fundamentals that could exert themselves with increasing force in the months ahead.

Firstly, we would certainly expect the monetary policy outlook to continue favouring non-dollar currencies however the conflict unfolds from here but certainly if the Strait of Hormuz was to reopen again and traffic increased steadily, risk conditions should remain positive and the Fed in those circumstances remain the most likely central bank to ease its monetary stance further. ECB and BoE central bankers who spoke last week were indicating there was time to assess before any decisions are made but generally the bias remains skewed to the need to tighten. We would argue that de-escalation and crude oil prices falling now will still have limits to the scale of decline (a geopolitical risk premium will remain embedded for some time) and inflation will certainly be higher than otherwise would have been the case. Is that fact well priced? The ECB is roughly priced for two rate hikes this year versus 15bps of easing prior to the conflict (a +60bp swing). The BoE is priced for one hike – a +75bp swing. The Fed is priced for 15bps of easing for a +45bps swing. The Fed is the only G10 central bank priced for any monetary easing this year. Under a re-escalation scenario the Fed would very likely be reluctant to hike in contrast to action from the ECB and BoE.

If we avoid re-escalation and we move gradually toward de-escalation, we would certainly expect financial market dynamics to slowly begin to shift to other drivers. One factor that was more prevalent at the start of the year was uncertainty over the independence of the Fed and that will be in focus tomorrow with Kevin Warsh’s nomination hearing to the Senate Banking Committee. There are two elements to this theme that could serve to undermine the dollar. The first relates to the how the transition from one Fed Chair to the next plays out. CNN reported last Wednesday that Thom Tillis still plans to block his nomination until the criminal investigation into Chair Powell is dropped. President Trump has stated that he will not drop the case. A probable delay to confirmation would see Fed Chair Powell extend his time. President Trump has threatened to then fire Powell. We can all see the potential for that process to go badly. The second relates to whether the markets’ confidence in Kevin Warsh being a truly independent Fed Chair will be doubted. The hearing tomorrow will be important in that regard. Trump has openly said that he wanted a Fed Chair who would cut rates. Warsh now argues that strong productivity growth will allow for easier policy without fuelling inflation. The more Warsh is seen pushing those views tomorrow, the more investors will doubt his independence. This could be one of the big negative risks for the dollar over the coming year if the Fed cuts rates and inflation remains above target, which seems likely for most of the next year.

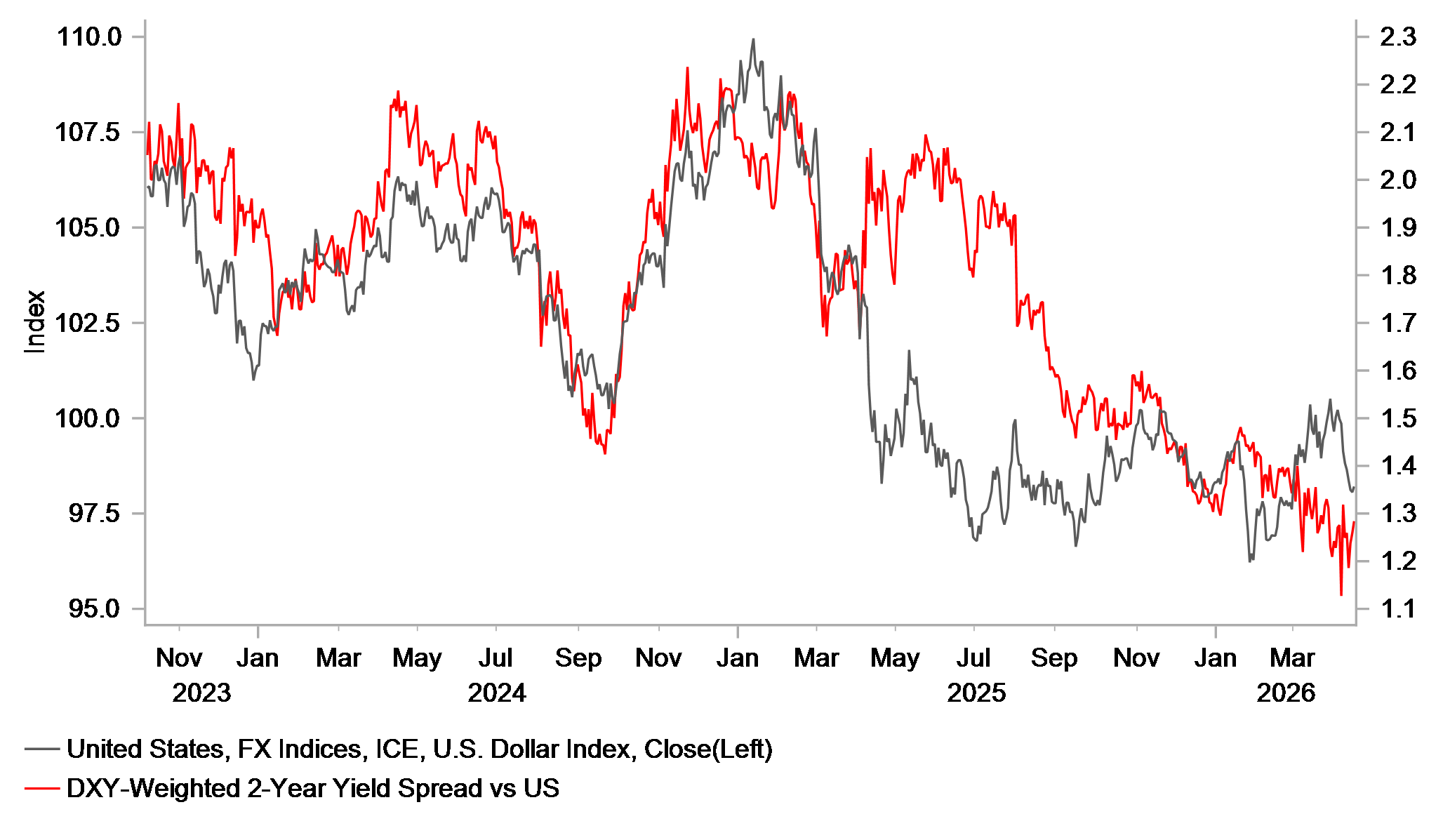

USD RETRACES BACK TOWARD YIELD SPREAD LEVELS

Source: Bloomberg, Macrobond & MUFG GMR

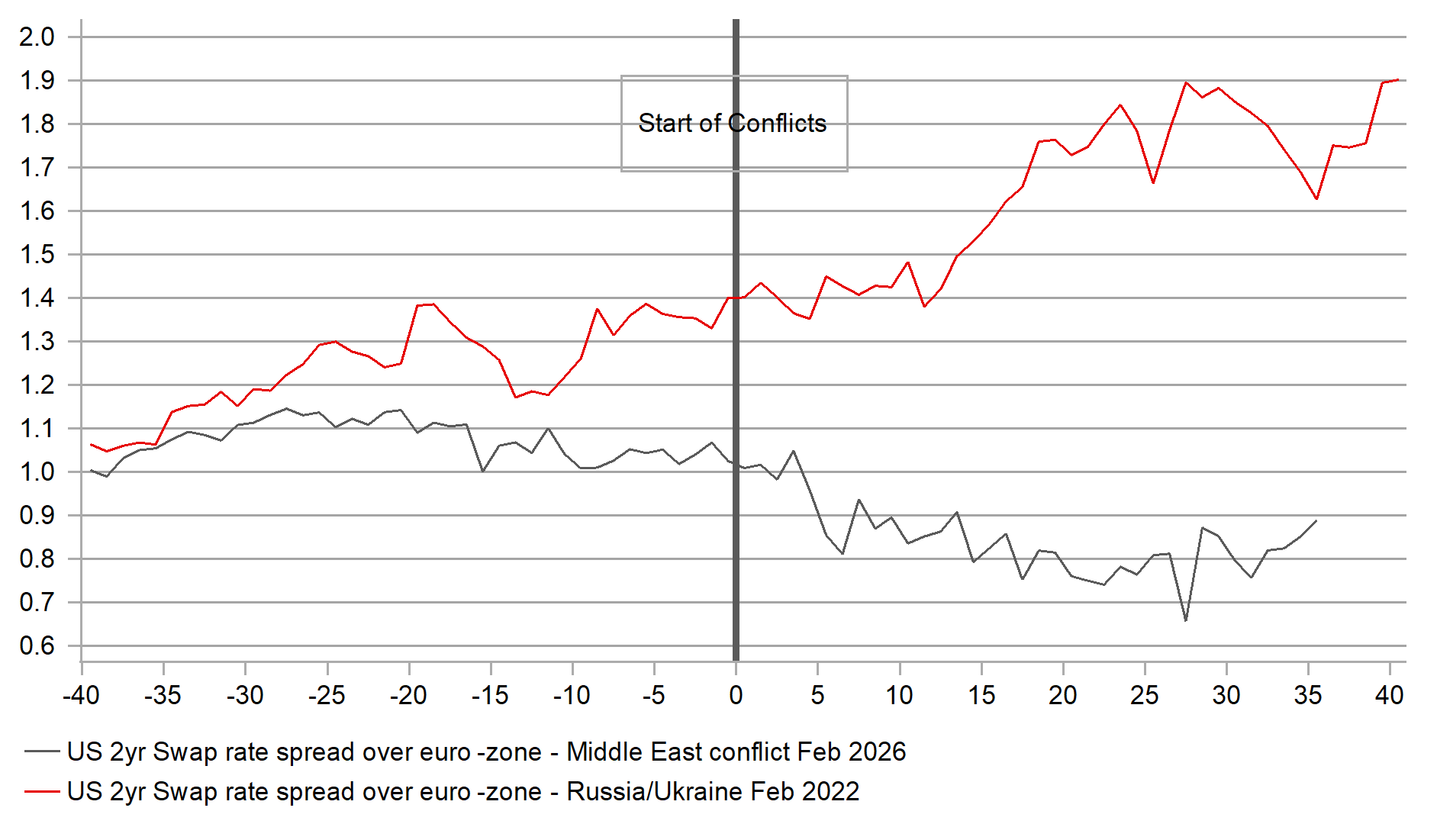

US-EZ YR SPREAD STILL LOWER VS PRE-CONFLICT

Source: Bloomberg, Macrobond & MUFG GMR

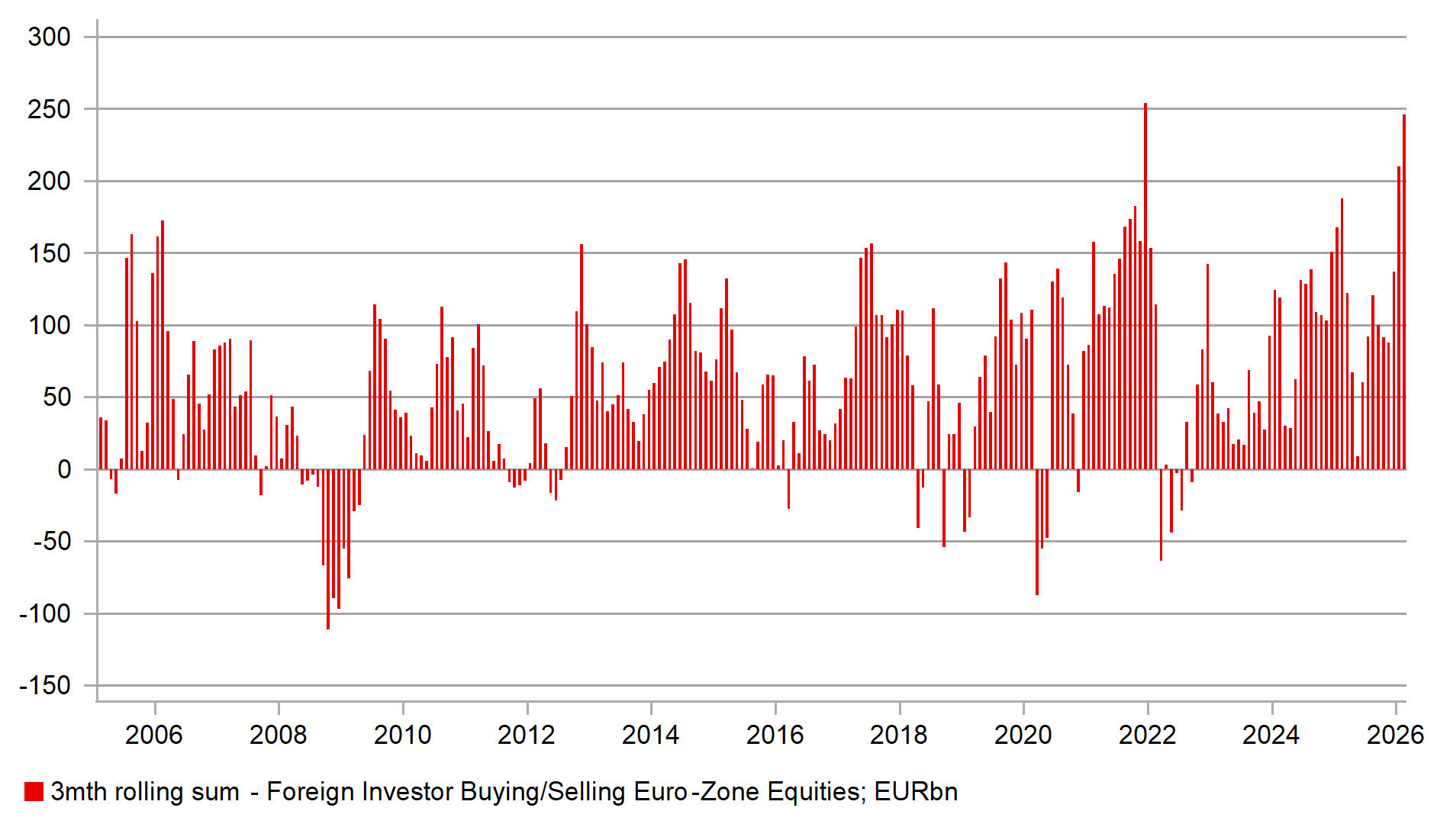

The FT reported last week that the EU is set to announce changes in M&A rules that will make it easier for large corporates to merge in order to compete better with some of the largest companies in the world. New rules will give more weight to innovation, resilience and sustainability with many now believing too much weight previously was given to consumer protection. The new rules could boost investor confidence and add to positive momentum for European equities. ECB flow data to February shows very strong demand for European equities ahead of the conflict with foreign investors buying nearly EUR 250bn worth of equities in the three-month period to February. That is just below the record for that period seen in the initial post-covid rebound in risk.

The weekend has seen Middle East risks increase again with the US seizing an Iranian ship and reports of Iranian shots fired. A lot now rests on whether negotiations take place in Pakistan and if so, how successful they can be. An extension of the ceasefire to allow further talks looks most plausible at this stage which would help maintain current market conditions, especially given US corporate earnings have been positive so far. According to Factset, with 10% of companies reported Q1 is on track for another double-digit growth in earnings. But the back and forth from de-escalation hopes to re-escalation fears should not mask the fact that the underlying fundamental backdrop for the US dollar remains poor. Risk-off will likely result in less US dollar appreciation than previously assumed while de-escalation could see those negative dynamics come to the fore more quickly. De-escalation would likely be accompanied by greater dollar downside momentum than re-escalation would be accompanied by dollar upside momentum.

FOREIGN BUYING EZ EQUITIES NEAR RECORD

Source: Bloomberg, Macrobond & MUFG GMR

RESILIENT EQUITY MARKETS KEEP USD WEAKER

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

|

NZD |

19/04/2026 |

23:45 |

Trade Balance NZD |

Mar |

-- |

-257m |

!! |

|

EUR |

20/04/2026 |

10:00 |

Construction Output MoM |

Feb |

-- |

-0.2% |

!! |

|

CAD |

20/04/2026 |

13:30 |

CPI YoY |

Mar |

2.5% |

1.8% |

!!! |

|

CAD |

20/04/2026 |

16:30 |

BoC Overall Business Outlook Survey |

1Q |

-- |

- 1.8 |

!! |

|

NZD |

20/04/2026 |

23:45 |

CPI YoY |

1Q |

-- |

3.1% |

!!! |

|

GBP |

21/04/2026 |

07:00 |

Average Weekly Earnings 3M/YoY |

Feb |

-- |

3.9% |

!! |

|

GBP |

21/04/2026 |

07:00 |

Employment Change 3M/3M |

Feb |

-- |

84k |

!!! |

|

EUR |

21/04/2026 |

10:00 |

Germany ZEW Survey Expectations |

Apr |

-- |

- 0.5 |

!! |

|

USD |

21/04/2026 |

Tbc |

Confirmation Hearing for Kevin Warsh |

|

|

|

!!! |

|

USD |

21/04/2026 |

13:30 |

Retail Sales Advance MoM |

Mar |

1.2% |

0.6% |

!!! |

|

USD |

21/04/2026 |

15:00 |

Pending Home Sales MoM |

Mar |

-- |

1.8% |

!! |

|

JPY |

22/04/2026 |

00:50 |

Trade Balance |

Mar |

¥1096.5b |

¥44.3b |

!! |

|

GBP |

22/04/2026 |

07:00 |

CPI YoY |

Mar |

-- |

3.0% |

!!! |

|

SEK |

22/04/2026 |

07:00 |

Unemployment Rate SA |

Mar |

-- |

8.4% |

!! |

|

EUR |

22/04/2026 |

18:30 |

ECB's Lagarde Speaks in London |

!!! |

|||

|

GBP |

23/04/2026 |

07:00 |

Public Sector Net Borrowing |

Mar |

-- |

14.3b |

!! |

|

EUR |

23/04/2026 |

09:00 |

S&P Global Eurozone Manufacturing PMI |

Apr P |

-- |

51.6 |

!!! |

|

EUR |

23/04/2026 |

09:00 |

S&P Global Eurozone Services PMI |

Apr P |

-- |

50.2 |

!!! |

|

GBP |

23/04/2026 |

09:30 |

S&P Global UK Services PMI |

Apr P |

-- |

50.5 |

!!! |

|

GBP |

23/04/2026 |

09:30 |

S&P Global UK Manufacturing PMI |

Apr P |

-- |

51.0 |

!!! |

|

USD |

23/04/2026 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

USD |

23/04/2026 |

14:45 |

S&P Global US Composite PMI |

Apr P |

-- |

50.3 |

!! |

|

JPY |

24/04/2026 |

00:30 |

Natl CPI YoY |

Mar |

1.5% |

1.3% |

!!! |

|

GBP |

24/04/2026 |

07:00 |

Retail Sales Inc Auto Fuel MoM |

Mar |

-- |

-0.4% |

!! |

|

CHF |

24/04/2026 |

09:00 |

SNB's Schlegel & Steiner Speak |

!! |

|||

|

EUR |

24/04/2026 |

09:00 |

Germany IFO Business Climate |

Apr |

-- |

86.4 |

!! |

|

CAD |

24/04/2026 |

13:30 |

Retail Sales MoM |

Feb |

0.9% |

1.1% |

!! |

|

USD |

24/04/2026 |

15:00 |

U. of Mich. Current Conditions |

Apr F |

-- |

50.1 |

!! |

Source: Bloomberg & MUFG GMR

Key Events:

- The two‑week US–Iran ceasefire is scheduled to expire on 21st April. Further talks between the US and Iran are expected to take place tomorrow, and there have been reports that the ceasefire could be extended for a further two weeks. However, developments over the weekend have cast fresh doubt on whether the talks will proceed. The IRGC fired on multiple commercial vessels in the Strait of Hormuz, while the US Navy fired upon and boarded an Iranian‑flagged cargo ship in the Gulf of Oman.

- The Senate Banking Committee has confirmed that the confirmation hearing for Kevin Warsh to become the next Fed chair will take place on 21st April. We expect Kevin Warsh to be confirmed. Market participants will listen closely for any signals on how he is likely to conduct monetary policy, particularly in light of the energy price shock currently affecting the US and global economies. The US rates market continues to expect that the Fed’s next policy move will be a rate cut later this year, once the initial inflationary impact has faded.

- Key economic data releases in the coming week include: i) March CPI reports from Canada, the UK and Japan, as well as New Zealand’s Q1 CPI report; ii) the UK labour market report for February; and iii) April PMI surveys for the euro area, the UK and the US.The March CPI data should capture the initial inflationary effects of higher energy prices triggered by the Middle East conflict, while the PMI surveys will provide early insight into the hit to business confidence and the likely impact on economic activity. Both the Bank of England and the ECB have dampened expectations of near‑term rate hikes and appear inclined to wait longer in order to better assess upside inflation risks.