FX reserve managers move into USD in Q1 but will this be sustained?

The Composition of Foreign Exchange Reserves (COFER) data for Q1 2026 showed USD holdings increased at the expense of EUR & JPY.

The standout observation from the change in reserves was the heavy selling by reserve managers of the yen, the third largest quarter of implied selling.

We also highlight the findings from the annual OMFIF Global Public Investor Survey and assess the prospects for EUR reserves increasing.

USD holdings increased likely fuelled by the Middle East conflict

The US dollar advanced by 1.7% in Q1 and the advance, mostly following the start of the conflict in the Middle East, was an important factor helping lift the USD composition in global reserves. After dropping to 56.4% in Q4 last year, the lowest USD composition since 1995, Q1 saw an increase to 57.1%. In nominal terms, the euro holdings in global reserves fell from 20.4% to 20.0% and yen holdings fell from 5.8% to 5.4%. The pound’s holdings were unchanged at 4.4% and the ‘other currencies’ portion was also unchanged at 10.8%. The USD holdings Q/Q increase was the first since the final quarter of 2024. The US dollar did advance on a Q/Q basis in Q3 and Q4 of last year, but the gains were modest and buying of non-dollars by reserve managers were larger than the non-dollar negative valuation impact and hence USD reserve holdings declined. Looking at the Q1 2026 reserve changes after stripping out the FX valuation impact shows that for the euro, reserve managers were also outright sellers as the euro declined in value. GBP holdings were unchanged because the negative valuation impact was offset by outright buying by reserve managers. For the other currencies reported individually – CAD, AUD & CHF – again reserve managers were modest buyers. In the case of CHF and CAD this helped offset negative valuation impacts while for AUD buying by reserve managers reinforced a positive valuation impact.

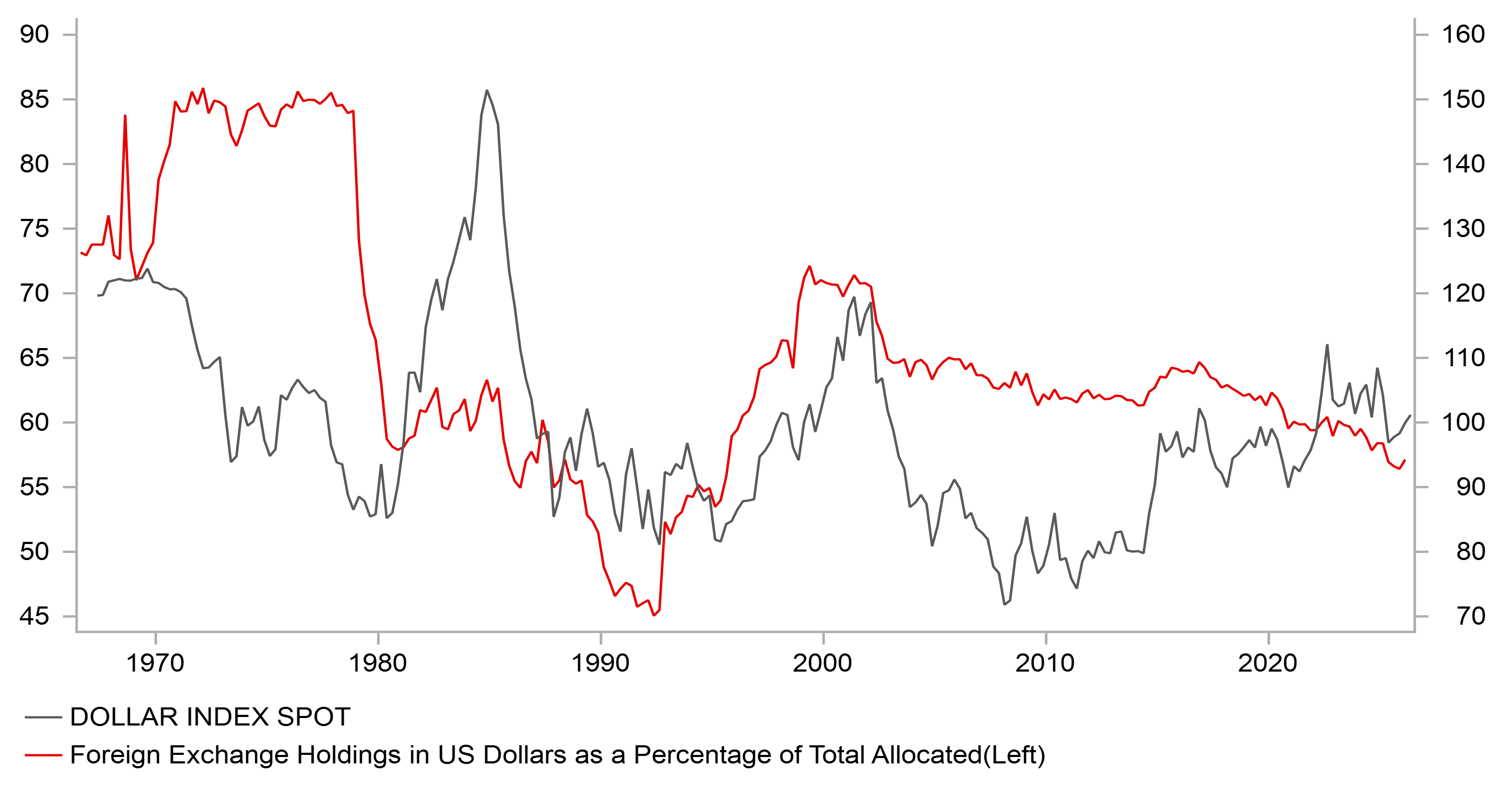

CONTINUED GRADUAL DROP IN USD RESERVES DESPITE STRONGER USD

Source: Bloomberg, IMF COFER, Macrobond & MUFG GMR

Reserve managers sell JPY – 3rd largest quarter of JPY selling ever

The most notable observation from the Q1 data was for JPY – the nominal composition drop from 5.8% to 5.4% was the lowest since Q4 2023 and was driven not just by valuation but also by some large selling. Stripping out the FX impact on total JPY holdings, there was a further USD 45bn drop in holdings in Q1, the largest quarterly drop since Q1 2018. The difference between then and Q1 2026 was that in 2018 the yen surged in value so reserve managers were selling yen into strength (USD/JPY dropped nearly 10 big figures in Q1 2018). The Q1 2026 implied JPY selling by reserve managers was the third largest in the series of the COFER data and the only one of the three largest reserve manager selling episodes in which the yen weakened during the quarter. That highlights worsening yen sentiment from global reserve managers.

CHF benefits from Middle East conflict, EUR does not

Reserve managers flows also indicate increased demand for CHF. CHF weakened modestly versus the USD in Q1, so valuation saw a drag but the total nominal CHF holding increased 6.8%, the biggest increase since Q4 2023. That was due to the largest buying since Q4 2024. However, CHF reserves remain tiny, at just 0.24% of total reserves. The hit to the euro from the energy price shock in 2022-23 due to Russia’s invasion of Ukraine was likely in the minds of reserve managers and the Middle East conflict likely encouraged outright euro selling. The outright selling in a quarter when the valuation had a negative impact on holdings was the first since the onset of the Russia/Ukraine conflict in Q1 2022.

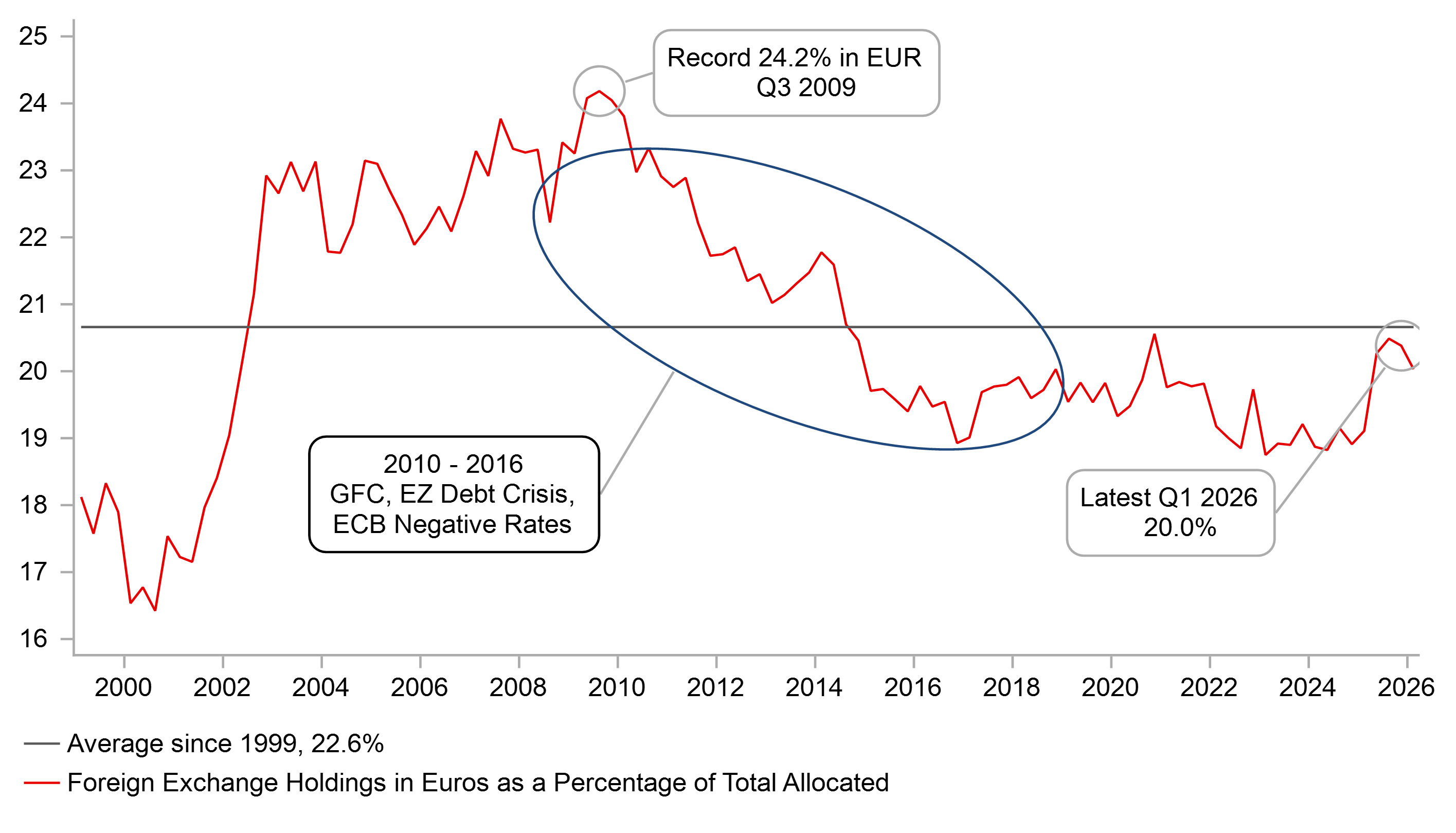

SELLING & VALUATION IMPACT LOWERS EURO’S SHARE OF RESERVES

Source: IMF COFER & Macrobond

OMFIF Global Public Investor 2026 confirms positive EUR prospects

More de-dollarisation & diversification

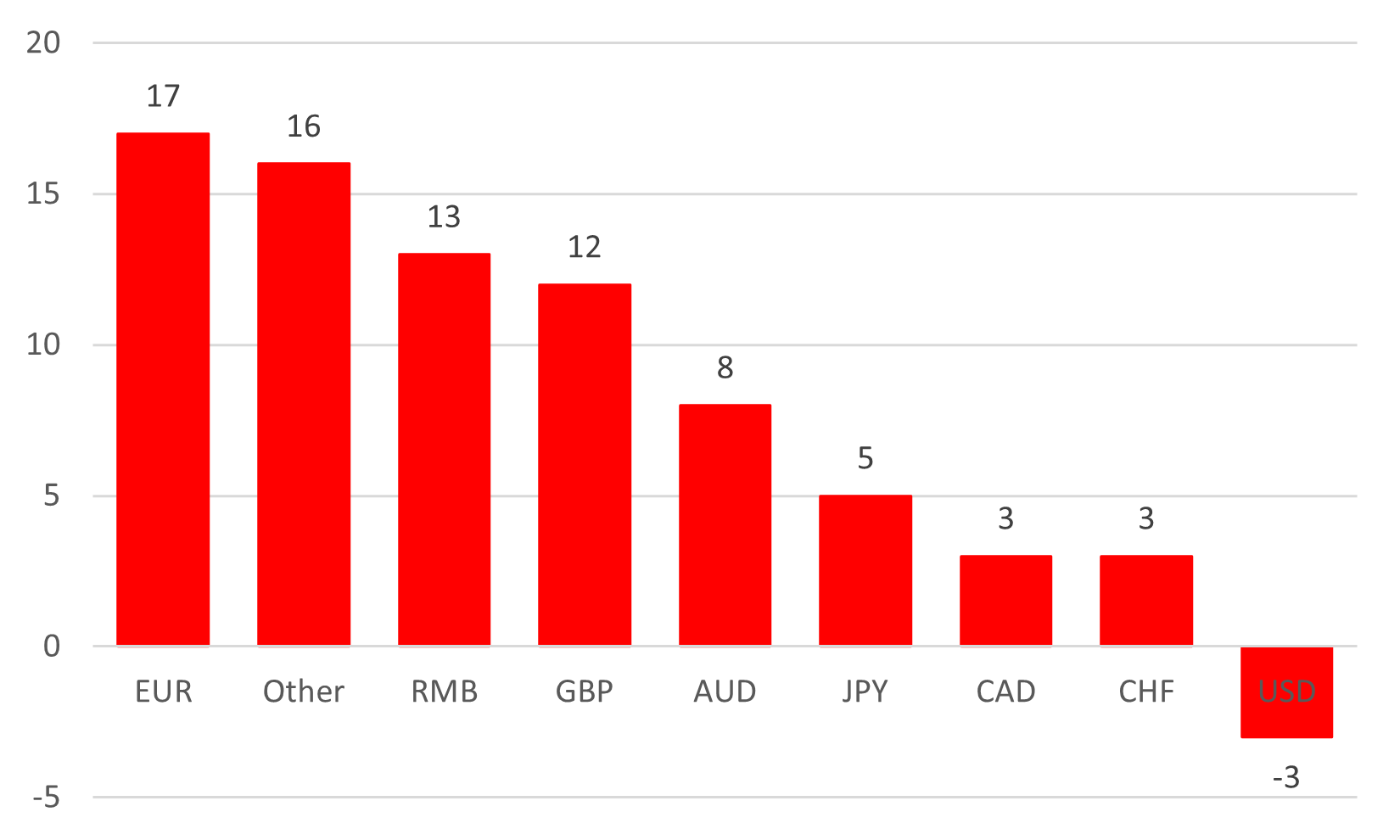

The OMFIF Global Public Investor 2026 publication was released in June and offers the most detailed overview of sentiment and investing plans amongst a large pool of global reserve managers. Global FX reserves covered in the COFER data stands at just over USD 13trn while the OMFIF GPI publication covers responses from 90 official institutions (74 central banks; 16 public pension funds & sovereign funds) with over USD 10trn in assets. One key takeaway is the indications in responses that points to the continued gradual diversification away from the US dollar. 79% of central banks see the global monetary system moving to a multi-polar currency structure. Policy rates remain the most important short-term driver of decisions on which currencies to invest (12-24mths) while geopolitics is the key factor shaping long-term strategies. 85% of respondents viewed the Middle East conflict as the top risk concern followed by unpredictable US foreign policies. The result of these developments shows continued plans to diversify away from the US dollar with a drop compared to last year from a net +5% to -3%. The biggest beneficiary of this drop was GBP which saw plans to increase holdings rise from a net +5% to +12%. JPY also declined notably from a net +9% to +5%. EUR remained top but the increase was modest from +16% to +17%. The ‘other currency’ category also increased notably from +13% to +16%. For the US dollar the 12-24mth plan has gone from a net increase of USD holdings of +18% in 2024, to +5% last year to -3% this year. President Trump and his policies are having a deeply negative impact on short-term appetite to hold the dollar.

OVER NEXT 12-24 MONTHS ARE YOU PLANNING TO INCREASE/DECREASE YOUR EXPOSURES TO THE FOLLOWING CURRENCIES?

Source: OMFIF Global Public Investor 2026

USD diversification over the long-term also; RMB, EUR & GBP benefit most

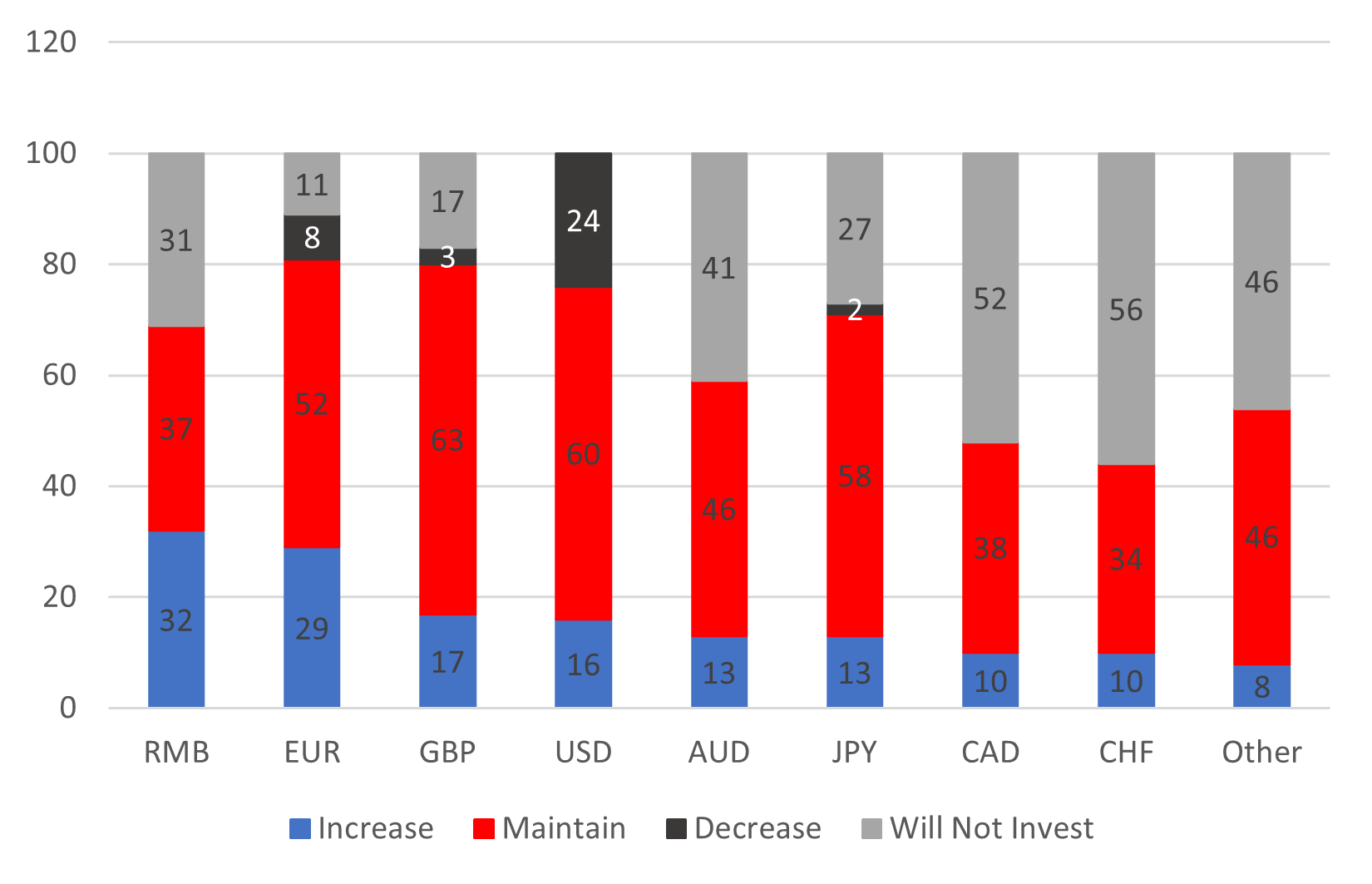

However, that indication of wanting to diversify over the short-term doesn’t change over the long-term either. Asking the same question as above but over a 10-year time horizon, there was a huge 24% that were planning to reduce USD holdings over that period. With only 16% planning an increase holdings, there was a net -8%. It was the only currency with a net negative reading. RMB was the top currency with a net +32% followed by EUR on +21% and GBP on +14%. While the ‘other currency’ category shows a strong appetite to increase holdings over the short-term, over the long-term the net increase was just 8% - only the US dollar was less. It suggests that central banks see a possible capacity issue in investing in smaller currencies over time. Structural challenges continue to constrain appetite for RMB and EUR and for holdings to increase an opening up of China’s capital account will be necessary while less fragmented capital markets in Europe is also likely required. What is telling is the high scores for GBP in both the short-term and long-term. It suggests less concerns over fiscal policy and inflation amongst global reserve managers, or put another way, that the yield offered in the UK sovereign bond markets adequately compensates investors for those sovereign and inflation risks.

LONG-TERM (10 YEARS) ARE YOU PLANNING TO INCREASE/DECREASE YOUR EXPOSURES TO THE FOLLOWING CURRENCIES?

Source: OMFIF Global Public Investor 2026

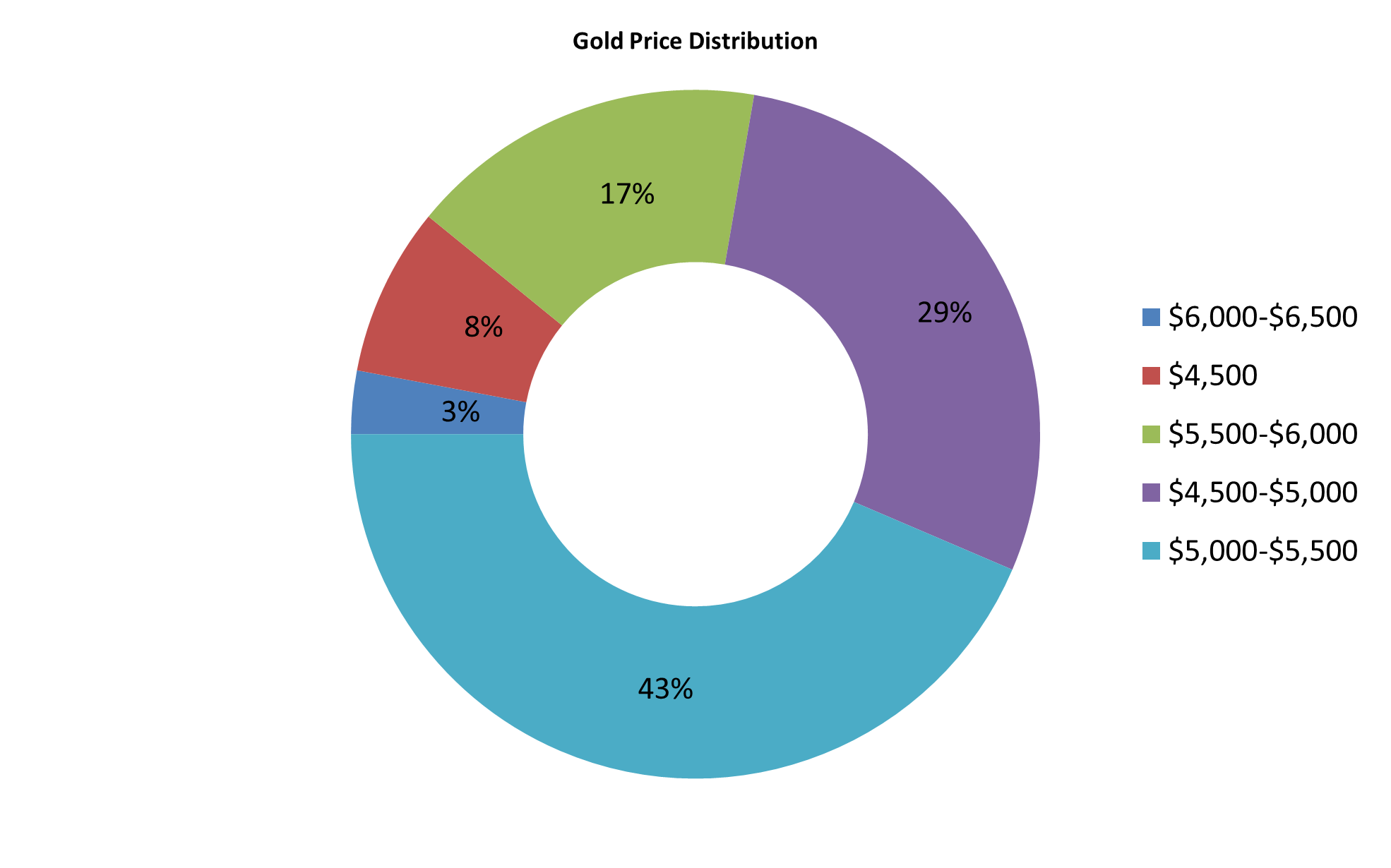

Gold most favoured asset over coming two years

With geopolitical risks elevated, reserve managers look set to continue increasing gold holdings. 82% of central banks hold gold (vs. 71% last year) with primary reasons being diversification followed by protecting against geopolitical risks and then as an inflation hedge. A little over 30% of respondents expect to increase their holdings of gold over the next 12-24 months, the largest across all assets and surpassing the next most popular asset – conventional sovereign bonds. Over a 10-year period, gold remains highly popular with a little over a net 40% planning to increase holdings. Only corporate bonds were more popular. Part of this may reflect the very bullish sentiment amongst respondents. 44% of respondents expect the price of gold to range between USD 5,000-5,500/oz by June 2027 while a further 20% expect a range between USD 5,500-6,500/oz. Only 8% expected a price of USD 4,500/oz or lower.

GLOBAL RESERVE MANAGERS ARE VERY BULLISH GOLD

Source: OMFIF Global Investor 2026

EUR opportunities

What the Global Policy Investor 2026 report has indicated once again is the opportunities that exist for the euro to be further internationalised and for its role as a reserve currency to increase. There has never been such a clear picture of global reserve managers intentions to continue moving away from the US dollar and over the short-term and long-term the euro is the most or second most popular currency for increasing holdings. 55% of global reserve managers stated that their willingness to hold the euro would increase further if there was a single euro-denominated safe asset. If the EU was therefore to become a permanent large-scale issuer of debt, then reserve managers’ demand for the euro would pick up. While there is a way to go to become a “large-scale” issuer, we believe the EU is set to increase further the issuance of EU bonds. In addition to a fragmented capital market, another impediment has been returns. Due to the historic shortage of German government bonds and the anchor that market serves for sovereign debt markets in the euro-zone, yields have generally been less than what is offered in US bond markets. But conditions are about to change. The problems of a shortage of German bunds will diminish over the coming years in line with the implementation of the EUR 1 trillion defence and infrastructure spending plan announced by Chancellor Merz last year. Gross German securities issuance this year is expected to increase from EUR 425bn last year to EUR 512bn this year, increasing total outstanding government bonds from EUR 2.84trn at the end of 2025.

EU bond market size to grow

A single entity issuer – the EU – is becoming a more important development and the EU bond market is growing. The EU is now effectively one of the largest supranational issuers globally through several different funding programs. The NextGenerationEU, some Ukraine support financing facilities, SAFE defence financing and some other EU programmes are all financed through EU issued bonds. As of now, the EU bond market has grown to EUR 827bn. Before covid and the NextGenEU financing, the EU bond market was very small. One of the key consequences of President Trump’s second term in office and Russia’s invasion of Ukraine is the drastic need for increased defence spending in the EU. The strategy of depending on the US and NATO for Europe’s security is seen as flawed and outdated and the EU is under considerable pressure to increase defence spending notably. Via SAFE or some other EU-wide financing programme, increased EU bond issuance to finance some of this defence spending need seems inevitable.

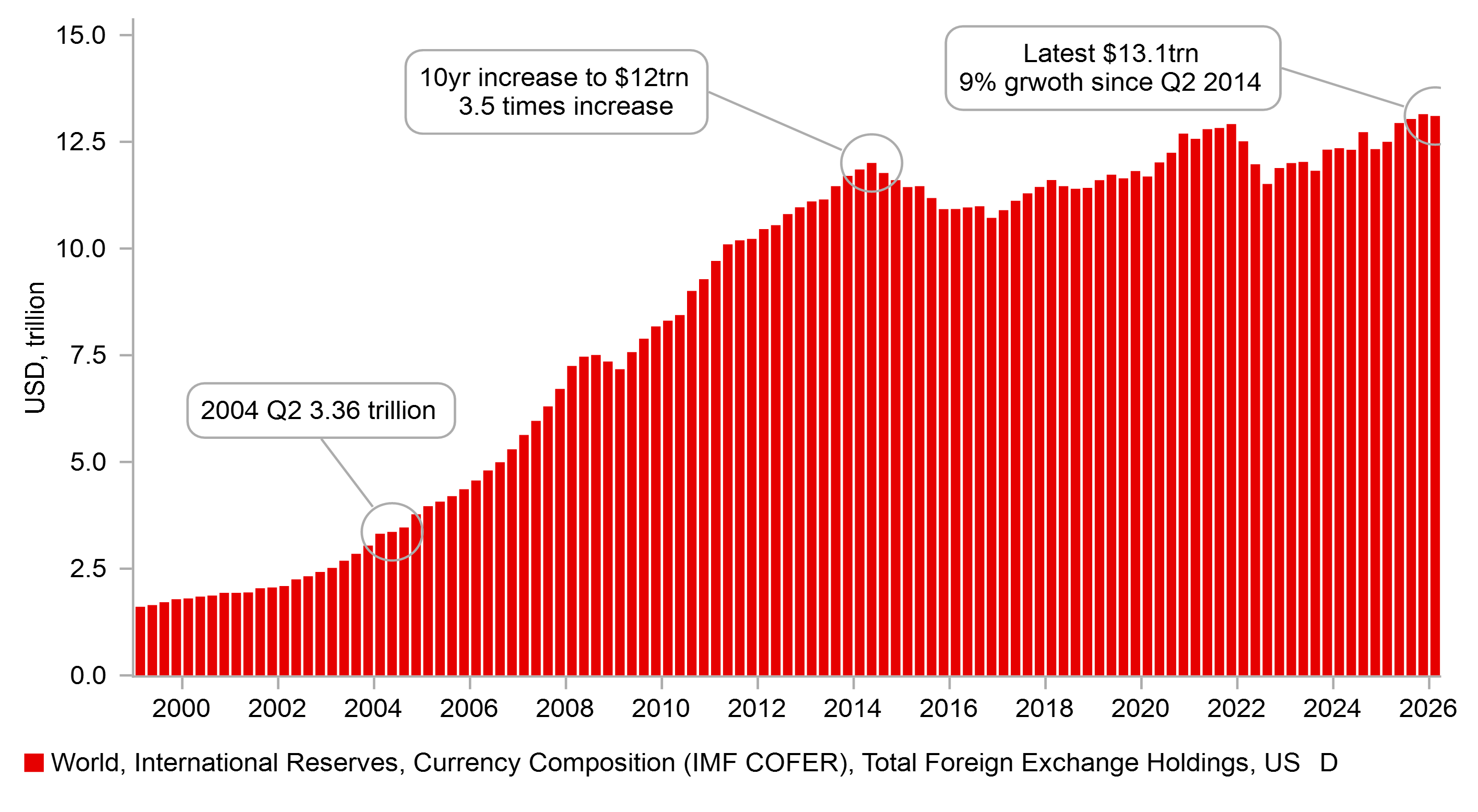

PACE OF GLOBAL FX RESERVE GROWTH HAS SLOWED SINCE 2014

Source: IMF COFER, Macrobond

EUR holdings can rise back toward previous highs over the coming years

The euro's reserve-currency challenge is no longer primarily about credibility. It is increasingly about capacity. If Germany's fiscal expansion and a permanent EU issuance framework materially increase the stock of euro safe assets, reserve managers may finally have enough depth and liquidity to raise euro allocations meaningfully over the coming decade. In 10 years’ time global reserve managers expect the USD composition to fall to 52% and EUR to rise to 23%. We see that projection as somewhat conservative and see no reason why the pace over the last 10 years is not sustained – from Q1 2016 to Q1 2026 the USD composition has fallen by close to 7ppts. A similar pace of decline would imply a drop to 50% by 2036. That could mean EUR holdings reaching 24% to 25%, to around the current record high of 24.2% in 2009. Assuming a 24.5% EUR composition by then and assuming the previous 10-year total global FX reserve growth rate is replicated through to 2036 (20%), the EUR composition would grow by over USD 1.2trn. Even assuming a stronger euro does some of the work there would still be a considerable upturn in EUR buying by global reserve managers. In the 10-year period since Q1 2016 the EUR composition has increased by USD 465bn. Valuation contributed to that increase only marginally

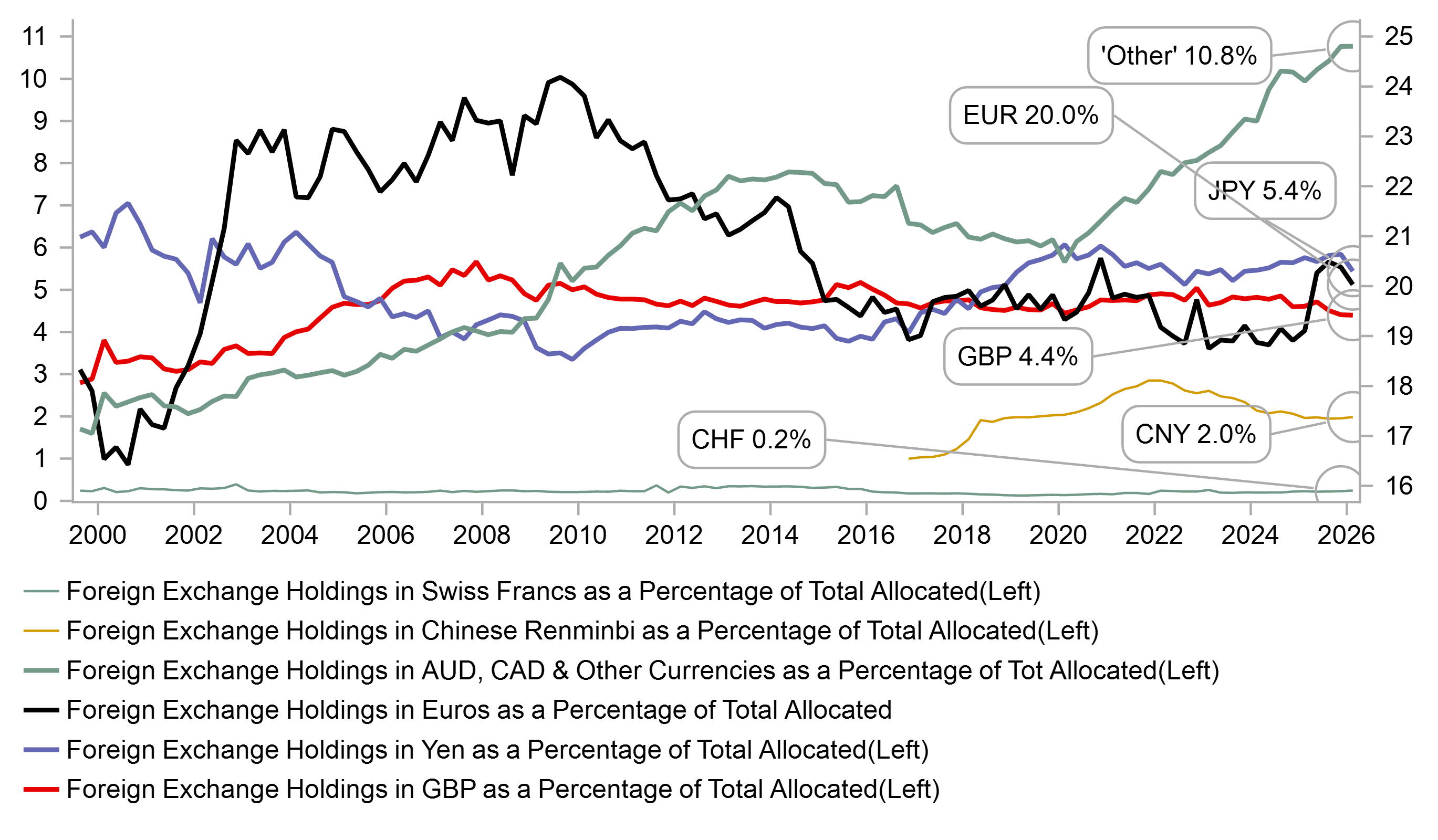

NON-DOLLAR FX RESERVE COMPOSITIONS FOR Q1 2026 – OTHER COULD RUN OUT OF CAPACITY LEAVING EUR BEST PLACED TO RISE

Source: IMF COFER, Macrobond