Oil price shock continues to spill over into FX market

USD: Oil prices continues to surge higher reflecting risk conflict drags on

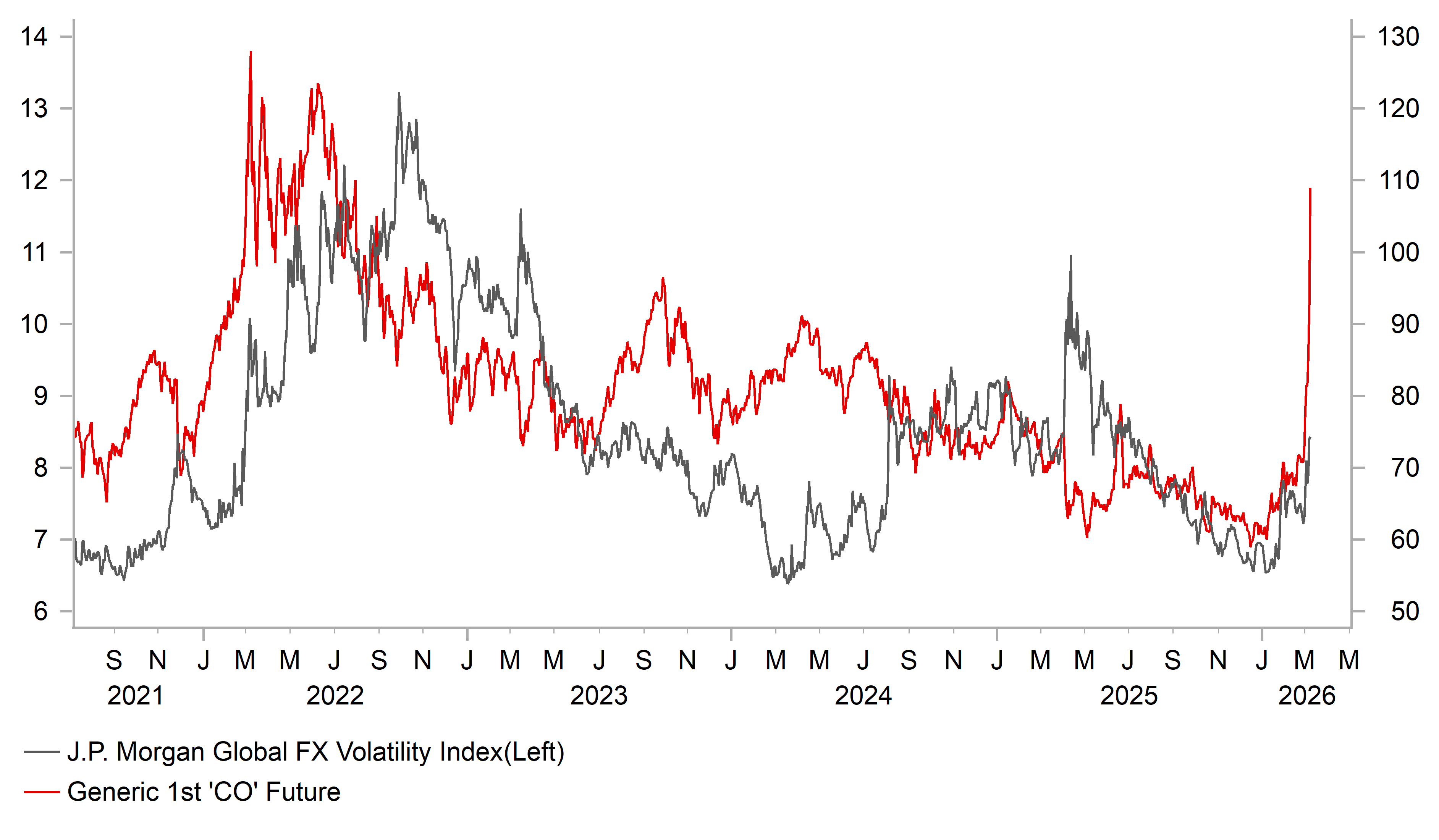

The price of oil has continued to surge higher at the start of this week driven by the ongoing conflict in the Middle East. The price of Brent has hit a fresh high overnight of USD119.50/barrel before dropping back below USD110/barrel. At the worst point it had extended its advance to almost two thirds since the conflict in the Middle East started last weekend which is the biggest jump since during the Global Financial Crisis during 2008. The surge higher for the price of oil is significantly increasing stagflation risks for the global economy and could trigger a deeper sell-off in global equity markets. The Japanese TOPIX equity index has fallen sharply overnight by around 4% extending its correction lower this month to almost 10% as it gives back most of the year to date gains. So far the spill-overs into the foreign exchange market have been relatively modest. The US dollar has continued to strengthen against other major currencies with the dollar index moving towards the top of the 96.000 to 100.00 trading range that has been in place since Q2 of last year. US dollar strength has been more evident against the high yielding emerging market currencies of the South African rand and Hungarianforint. Financial market conditions are becoming more challenging for carry trades triggering an unwind of popular positions with the FX market likely to become much more volatile the longer the conflict drags on.

President Trump’s post yesterday on Truth Social has added to investor concerns over a more disruptive outcome from the conflict in the Middle East. He downplayed the jump in oil prices by stating “short-term oil prices, which will drop rapidly when the destruction of the Iran nuclear threat is over, is a very small price to pay for U.S.A., and World, Safety, and Peace. ONLY FOOLS WOULD THINK DIFFERENTLY!”. Furthermore, Iran’s decision to choose Mojtaba Khamenei, the hard-line son of recently deceased Ayatollah Ali Khamenei, to be the new supreme leader has signalled that Iran is not ready to back down in the conflict. He has deep ties to the Islamic Revolutionary Guard Corps. President Trump has already told Fox News that he is “not happy” with the pick, and had previously told ABC News that “if he doesn’t get approval from us, he’s not going to last long”. The new leader pick increases the risk of more prolonged conflict in the Middle East.

In an attempt to put a dampener on surging oil prices and the negative impact for the global economy, G7 finance ministers are reportedly set to discuss a possible joint release of oil reserves today. The call is set to take place at around 13.30 CET and was initiated by France who currently hold the G7 presidency. The joint action apparently has the support of the US and any action will be in coordination with the International Energy Agency (IEA). According to Bloomberg, co-ordinated drawdowns of strategic stockpiles have only been carried out on five prior occasions with the last two in response to Russia’s invasion of Ukraine. The FT reported one person as saying that some US officials believe a joint release in the range of 300 million to 400 million barrels, or around 25% to 30% of the 1.2 billion barrels held in reserve, would be appropriate. The Strait of Hormuz normally carries between 17-20 million barrels of crude and refined products. So, the SPR release would offset around 2 to 3 weeks of normal Strait of Hormuz flows if it remains effectively closed. It would be a temporary fix to help prevent an even more disruptive surge in the price of oil in the coming weeks.

With the conflict in the Middle East understandably the main driver of financial markets in the near-term, it has meant that global economic data releases have become less important as they will be viewed as even more backward looking than normal covering the period prior to the energy price shock. The release of the latest nonfarm payrolls report released on Friday did though reveal a big downside surprise for the health of the US labour market. The report revealed that employment contracted by -92k in February giving back the strong employment gains of 126k in January. The scale of employment weakness in February was driven by a number of temporary factors including the bad winter weather, a health-care workers strike, and payback weakness for strong employment growth recorded in January. Employment growth has been volatile at the start of this year but the underlying trend still appears to have remained weak similar to at the end of last year. Private employment growth has averaged 30k/month so far in 2026 which compares to an average of 26k/month in Q4 2025.

Normally, the softer NFP report would have reinforced Fed rate cut expectations and weakened the US dollar in the absence the Middle East conflict. The combination of still weak US labour market and energy price shock is putting the Fed in an even more difficult position when setting policy. The energy price shock will lift inflation in the near-term but demand destruction should ultimately prove disinflationary further down the line. So far the US rate market has moved to push back both the timing and scale of further Fed rate cuts lifting US rates and the US dollar. However, there has been a bigger hawkish repricing in Europe. The euro-zone rate market has now moved to price in almost 50bps of ECB rate hikes by year end even though the euro-zone economy will be hit by a bigger negative energy price shock.

OIL PRICE SPIKE TO TRIGGER JUMP IN FX VOLATILITY?

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EU |

09:30 |

Sentix Investor Confidence |

(Mar) |

-3.1 |

4.2 |

! |

|

EU |

10:00 |

Eurogroup Meetings |

- |

- |

- |

!! |

|

US |

15:00 |

Consumer Inflation Expectations |

(Feb) |

- |

3.1% |

! |

|

JP |

23:50 |

GDP (QoQ) |

(Q4) |

0.1% |

-0.6% |

!!! |

Source: Bloomberg & Investing.com